3 Reasons to Steer Clear of SNX and 1 Alternative Stock Worth Buying

TD SYNNEX: Recent Performance Overview

Over the last half-year, TD SYNNEX's stock price has remained relatively unchanged, delivering a modest gain of 4.7% and currently sitting at $156.16 per share.

Should investors consider adding TD SYNNEX to their portfolios now, or is caution warranted?

Why We’re Not Enthusiastic About TD SYNNEX

Our outlook on TD SYNNEX is reserved. Below are three key reasons why we find SNX less compelling, along with an alternative stock we prefer.

1. Sluggish Revenue Expansion

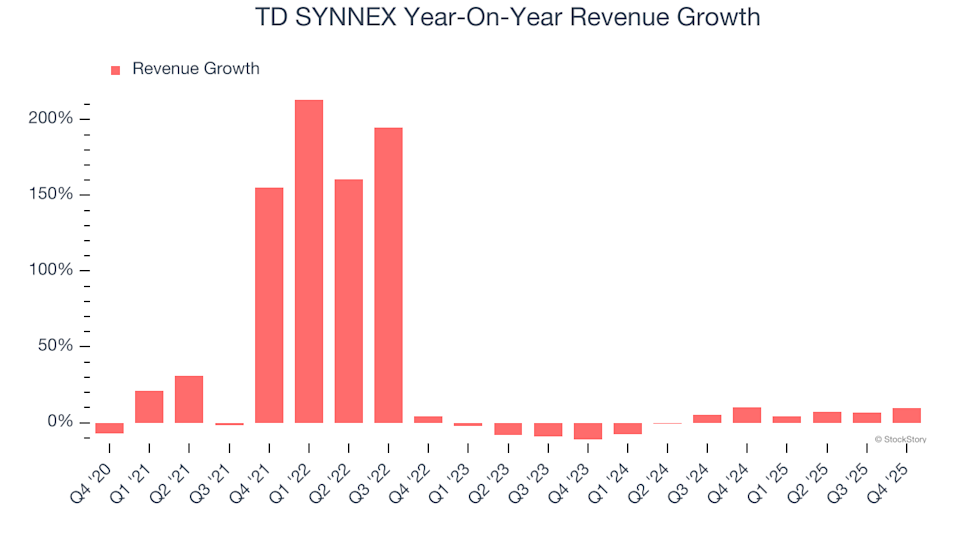

At StockStory, we prioritize sustainable long-term growth. However, in the business services sector, focusing solely on historical trends can overlook recent shifts and innovation. TD SYNNEX has experienced a noticeable slowdown, with annualized revenue growth of just 4.2% over the past two years—significantly trailing its five-year average.

TD SYNNEX Year-On-Year Revenue Growth

2. Stagnant Earnings Per Share

We closely monitor changes in earnings per share (EPS) as a measure of profitable growth. Over the last five years, TD SYNNEX's EPS has remained flat, despite a 25.6% annualized increase in revenue. This indicates that as the company grew, its profitability per share did not keep pace.

TD SYNNEX Trailing 12-Month EPS (Non-GAAP)

3. Weak Free Cash Flow Margins

Free cash flow is a critical metric for us, as it reflects a company's ability to generate real cash rather than just accounting profits. TD SYNNEX has underperformed its industry peers in this area, with an average free cash flow margin of only 1.6% over the past five years. This limited cash generation restricts its capacity to reward shareholders or reinvest in growth.

TD SYNNEX Trailing 12-Month Free Cash Flow Margin

Our Verdict

Ultimately, TD SYNNEX does not meet our criteria for high-quality businesses. While its current forward P/E ratio of 10.7 (equivalent to $156.16 per share) may seem attractive, the company's underlying fundamentals introduce considerable risk. We believe there are more promising opportunities available. Consider exploring one of our top picks in software and edge computing instead.

Alternative Stocks Worth Considering

Don’t Miss: This Week’s Top 6 Stock Picks — The current market environment is quickly distinguishing strong performers from overpriced stocks, with AI-driven shifts impacting entire sectors. In such a dynamic landscape, having a curated list of high-quality companies is essential.

Our AI-powered system previously identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rally, and Nvidia prior to its 1,178% climb. Every week, it highlights six new stocks that meet our rigorous standards.

Our recommendations have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) as well as lesser-known success stories such as Tecnoglass, which delivered a 1,754% return over five years. Discover your next potential winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

SEC submits framework to White House on applying securities laws to crypto assets

Alibaba CEO confirms departure of Qwen AI division head

NZD/USD holds onto gains near 0.5950 as US Dollar’s rally hits pause

First Bullish MACD Cross Since 2020: 5 Altcoins Positioned for a Potential 50x Expansion Move