Dollar Weakens Amid Stock Market Rebound

Dollar Index Slides Amid Stock Market Rally

The dollar index (DXY00) has declined by 0.13% today, pressured by a surge in equities following a New York Times report suggesting Iranian officials are open to negotiating an end to the conflict. However, the dollar managed to rebound from its lowest point after the February ADP employment data revealed that U.S. companies hired more workers than anticipated, and the ISM services index for February posted its strongest growth in three and a half years—both developments that could influence the Federal Reserve toward a more hawkish stance.

Key Economic Updates

- ADP Employment: U.S. private sector jobs increased by 63,000 in February, surpassing forecasts of a 50,000 gain.

- ISM Services Index: The February reading jumped by 2.3 points to 56.1, defying expectations of a drop to 53.5 and marking the fastest expansion since mid-2020. Conversely, the prices paid sub-index fell by 3.6 points to 63.0, an 11-month low, which was weaker than the expected rise to 68.3.

- Fed Outlook: Cleveland Fed President Beth Hammack emphasized the importance of returning inflation to target levels, noting that monetary policy may remain unchanged for an extended period.

- Rate Cut Odds: Swaps markets currently assign just a 2% probability to a 25 basis point rate cut at the upcoming March 17-18 policy meeting.

- Long-Term Rate Expectations: The FOMC is projected to reduce rates by about 37 basis points in 2026, while the Bank of Japan is expected to raise rates by 25 basis points, and the European Central Bank is anticipated to keep rates steady.

Currency Market Movements

EUR/USD has risen by 0.16% today, buoyed by dollar weakness and robust Eurozone economic data. The Eurozone’s January Producer Price Index (PPI) climbed 0.7% month-over-month and fell 2.1% year-over-year, both outperforming expectations. Additionally, the region’s unemployment rate dropped to a record low of 6.1%, indicating a stronger labor market than the anticipated 6.2%. These factors are seen as supportive for the euro and suggest a more hawkish stance from the ECB. Swaps indicate no expectation of a rate cut at the ECB’s next meeting on March 19.

USD/JPY has declined by 0.30% as the yen strengthens. Japan’s February consumer confidence index surged to a 6.75-year high, and comments from Finance Minister Satsuki Katayama signaled the government’s readiness to intervene in currency markets if needed. A sharp 3% drop in the Nikkei Stock Index to a 3.5-week low has also increased demand for the yen as a safe haven.

Additional Market Headlines from Barchart

International Economic Highlights

- Japan: The February consumer confidence index climbed by 2.1 points to 40.0, the highest since mid-2017, beating expectations of 38.2. Markets are pricing in a 5% chance of a Bank of Japan rate hike at the March 19 meeting.

- Eurozone: January’s PPI increased by 0.7% month-over-month and decreased by 2.1% year-over-year, both better than forecasts. The unemployment rate fell by 0.2 percentage points to a historic low of 6.1%.

Precious Metals and Safe-Haven Demand

April COMEX gold rose by $26.80 (0.52%), and May COMEX silver gained $0.342 (0.41%) today. Both metals are rebounding after Tuesday’s sharp declines, supported by a weaker dollar. Heightened geopolitical tensions, particularly concerns about the Iran conflict spreading across the Middle East, have increased safe-haven buying of gold. Recent Iranian drone and missile attacks on several countries, including Qatar, Saudi Arabia, Bahrain, and Oman, have contributed to this demand. Additionally, the closure of Qatar’s Ras Laffan natural gas plant and the Strait of Hormuz has led to reduced crude production by Iraq and Saudi Arabia, fueling fears of rising energy costs and inflation, which in turn is boosting interest in precious metals as an inflation hedge.

However, gold and silver retreated from their highs following hawkish remarks from Cleveland Fed President Beth Hammack and stronger-than-expected U.S. economic data, which pushed Treasury yields higher and weighed on precious metals.

Safe-haven interest in precious metals also persists due to ongoing conflicts in Iran, Ukraine, the Middle East, and Venezuela. Uncertainty surrounding U.S. tariffs, political instability, large deficits, and unpredictable government policies is prompting investors to reduce dollar holdings in favor of gold and silver.

Central banks continue to support gold prices, with China’s central bank increasing its gold reserves for the fifteenth consecutive month in January, adding 40,000 ounces to reach a total of 74.19 million troy ounces.

Liquidity injections by the Federal Reserve, including a $40 billion monthly boost announced in December, are also driving demand for precious metals as a store of value. Fund interest remains robust, with gold ETF holdings reaching a 3.5-year high last Friday. Silver ETF holdings also hit a multi-year high in December, though they have since retreated to a three-and-a-half-month low.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Circle's Rally: An Oil, Interest Rates, and Reserves Trade Fueled by Market Momentum

Micron: Why the Recent Pullback is an Opportunity

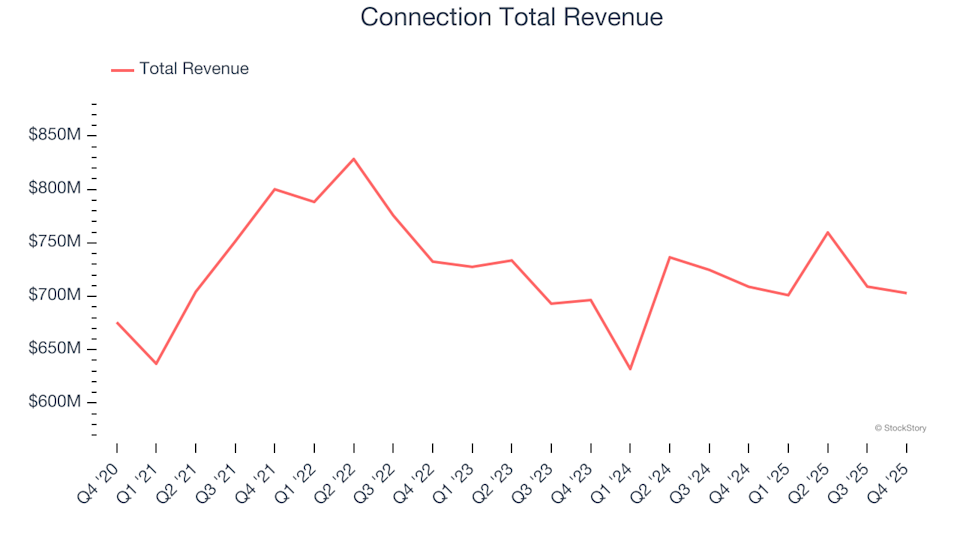

Winners And Losers In Q4: How Connection (NASDAQ:CNXN) Compares To Other IT Distribution & Solutions Stocks

NLight Stock Surges After Baird's $95 Price Target