Cracker Barrel's (NASDAQ:CBRL) Q4 CY2025 Sales Top Estimates, Stock Soars

Restaurant company Cracker Barrel (NASDAQ:CBRL) announced

Is now the time to buy Cracker Barrel?

Cracker Barrel (CBRL) Q4 CY2025 Highlights:

- Revenue: $874.8 million vs analyst estimates of $864.2 million (7.9% year-on-year decline, 1.2% beat)

- Adjusted EPS: $0.25 vs analyst estimates of -$0.30 (significant beat)

- Adjusted EBITDA: $38.16 million vs analyst estimates of $26.54 million (4.4% margin, 43.8% beat)

- The company slightly lifted its revenue guidance for the full year to $3.26 billion at the midpoint from $3.25 billion

- EBITDA guidance for the full year is $92.5 million at the midpoint, above analyst estimates of $91.52 million

- Operating Margin: 0.1%, down from 3.1% in the same quarter last year

- Free Cash Flow Margin: 2.8%, down from 6.3% in the same quarter last year

- Locations: 710 at quarter end, down from 726 in the same quarter last year

- Same-Store Sales fell 7.1% year on year (4.7% in the same quarter last year)

- Market Capitalization: $685.7 million

Cracker Barrel President and Chief Executive Officer Julie Masino said, "Our disciplined focus on operational excellence is driving significant improvements in several key guest metrics, many of which serve as important leading traffic indicators. We have also taken additional actions to improve financial performance and remain confident that we are well-positioned to regain prior momentum."

Company Overview

Known for its country-themed food and merchandise, Cracker Barrel (NASDAQ:CBRL) is a beloved American restaurant and retail chain that celebrates the warmth and charm of Southern hospitality.

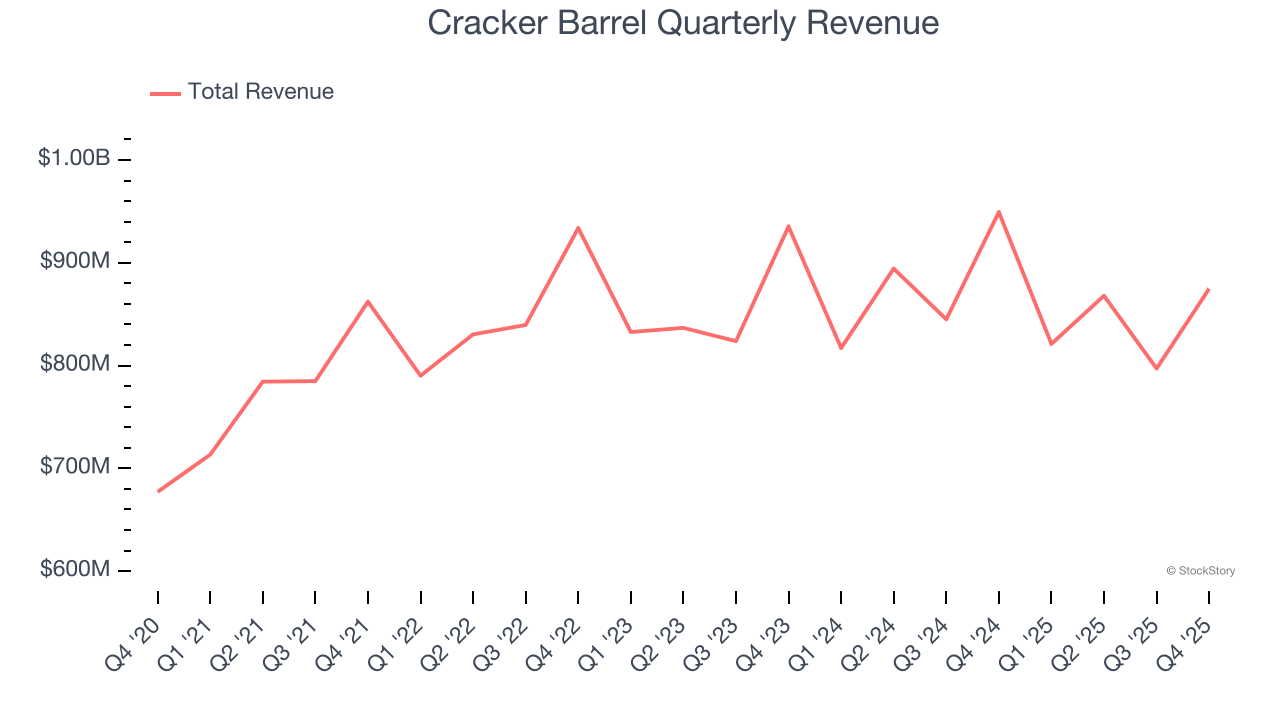

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $3.36 billion in revenue over the past 12 months, Cracker Barrel is one of the larger restaurant chains in the industry and benefits from a well-known brand that influences consumer purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing restaurant banners have penetrated most of the market. For Cracker Barrel to boost its sales, it likely needs to adjust its prices, launch new chains, or lean into foreign markets.

As you can see below, Cracker Barrel’s 1.2% annualized revenue growth over the last six years was weak as it didn’t open many new restaurants.

This quarter, Cracker Barrel’s revenue fell by 7.9% year on year to $874.8 million but beat Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to decline by 1.8% over the next 12 months, a deceleration versus the last six years. This projection doesn't excite us and indicates its menu offerings will face some demand challenges.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar.

Restaurant Performance

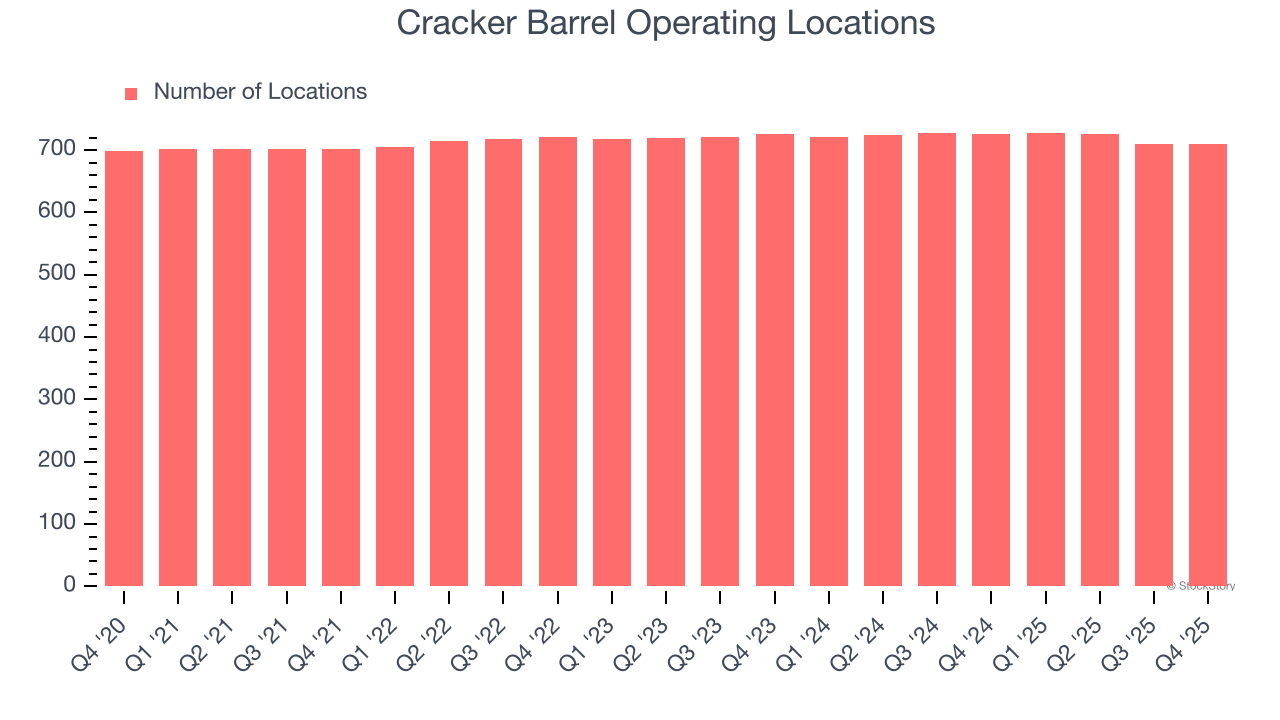

Number of Restaurants

The number of dining locations a restaurant chain operates is a critical driver of how quickly company-level sales can grow.

Cracker Barrel operated 710 locations in the latest quarter, and over the last two years, has kept its restaurant count flat while other restaurant businesses have opted for growth.

When a chain doesn’t open many new restaurants, it usually means there’s stable demand for its meals and it’s focused on improving operational efficiency to increase profitability.

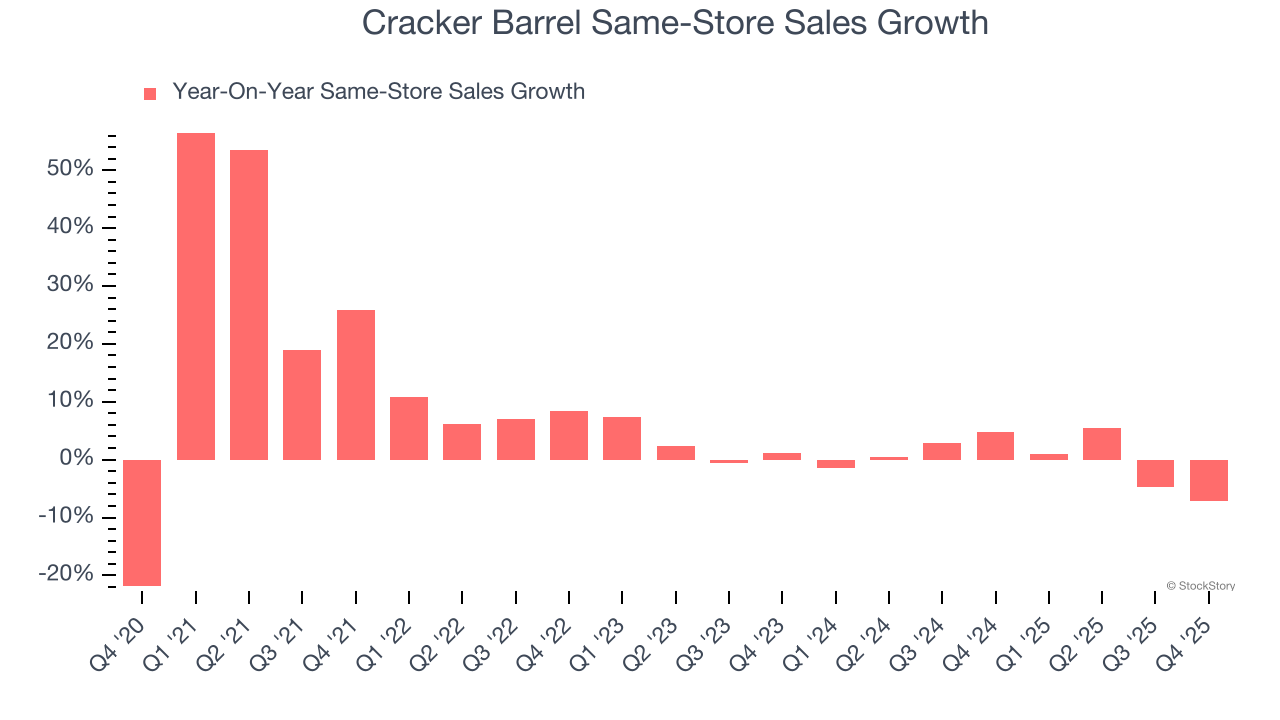

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth at restaurants open for at least a year.

Cracker Barrel’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if Cracker Barrel starts opening new restaurants to artificially boost revenue growth.

In the latest quarter, Cracker Barrel’s same-store sales fell by 7.1% year on year. This decline was a reversal from its historical levels.

Key Takeaways from Cracker Barrel’s Q4 Results

It was good to see Cracker Barrel beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 9.4% to $33.49 immediately after reporting.

Indeed, Cracker Barrel had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Echostar Stock Plunges 2.46 as $460M Volume Ranks 270th Amid Sector-Wide Selloff

NXP Semiconductors Gains 0.52% as Trading Volume Plummets 24.84% to $510 Million Ranking 238th in Daily Activity

Pulmonx Corporation (LUNG) Posts Fourth Quarter Loss, Surpasses Revenue Projections

Historical Trends Cast Doubt on Bitcoin’s March Performance