ChargePoint (NYSE:CHPT) Reports Q4 CY2025 Revenue Surpassing Expectations, Yet Shares Decline

ChargePoint Q4 CY2025 Earnings Overview

ChargePoint Holdings (NYSE:CHPT), a leader in EV charging solutions, surpassed Wall Street’s revenue projections for the fourth quarter of calendar year 2025, posting $109.3 million in sales—a 7.3% increase compared to the previous year. However, the company’s forecast for next quarter’s revenue stands at $95 million, which is 8.5% below analyst expectations. The GAAP loss per share was $1.85, performing better than consensus estimates by 6.8%.

Is this the right moment to invest in ChargePoint?

Highlights from ChargePoint’s Q4 CY2025

- Revenue: $109.3 million, exceeding analyst estimates of $104.7 million (7.3% year-over-year growth, 4.4% above expectations)

- EPS (GAAP): -$1.85, beating analyst estimates of -$1.98 (6.8% better than expected)

- Adjusted EBITDA: -$18.39 million (margin of -16.8%, representing a 6.2% decline year-over-year)

- Q1 CY2026 Revenue Guidance: $95 million at the midpoint, below analyst projections of $103.8 million

- Adjusted EBITDA Margin: -16.8%, consistent with the same quarter last year

- Free Cash Flow: -$1.97 million, improved from -$4.62 million in the prior year’s quarter

- Market Capitalization: $153 million

About ChargePoint

ChargePoint (NYSE:CHPT) emerged as a prominent EV charging provider during the COVID-era market surge, delivering electric vehicle charging technology across North America and Europe.

Revenue Trends

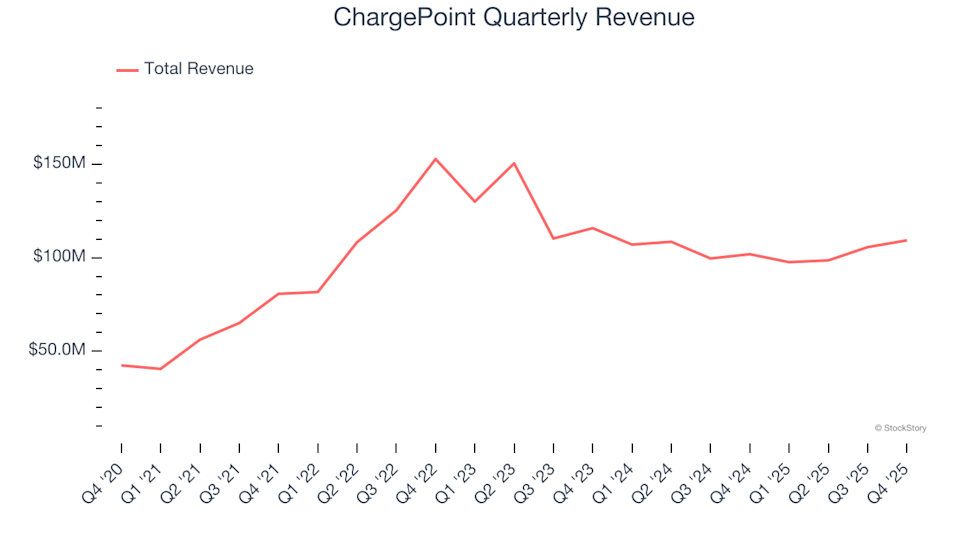

Evaluating a company’s performance over time helps gauge its quality. While short-term gains are possible for any business, sustained growth is a hallmark of industry leaders. Over the past five years, ChargePoint achieved an impressive compounded annual sales growth rate of 22.9%, outpacing typical industrial sector companies and indicating strong market demand for its products.

ChargePoint Quarterly Revenue

Although long-term growth is crucial, a five-year view may overlook recent shifts in the industrial sector. ChargePoint’s revenue trajectory has reversed in the past two years, with annualized declines of 9.9%.

ChargePoint Year-On-Year Revenue Growth

Examining ChargePoint’s main revenue streams—Networked Charging Systems (hardware) and Subscriptions (software)—reveals that these segments account for 52.7% and 38.8% of total revenue, respectively. Over the last two years, hardware sales declined by an average of 10.8% annually, while software subscriptions grew by 12.9% per year.

ChargePoint Quarterly Revenue by Segment

This quarter, ChargePoint saw a 7.3% year-over-year increase in revenue, reaching $109.3 million and beating Wall Street’s forecast by 4.4%. Management expects sales to decrease by 2.7% year-over-year in the upcoming quarter.

Looking ahead, analysts anticipate ChargePoint’s revenue will grow by 5.9% over the next year. While this suggests new offerings may drive improved results, the projected growth remains below the industry average.

Profitability and Operating Margin

Operating margin is a key indicator of profitability, reflecting the company’s ability to generate earnings after covering production, marketing, and R&D costs. ChargePoint’s substantial expenses have resulted in an average operating margin of -74.4% over the past five years. Unprofitable industrial companies warrant caution, as they may struggle during economic downturns.

On a positive note, ChargePoint’s operating margin improved by 58.8 percentage points over five years, thanks to sales growth and increased operating leverage. Nevertheless, achieving sustained profitability remains a challenge.

ChargePoint Trailing 12-Month Operating Margin (GAAP)

For the most recent quarter, ChargePoint’s operating margin was -48.5%.

Earnings Per Share (EPS)

Tracking EPS over time helps determine whether a company’s growth translates into profits. While ChargePoint’s annual earnings remain negative, it has reduced losses and improved EPS by 51.8% annually over the past five years. The upcoming quarters will be pivotal in assessing whether the company can achieve lasting profitability.

ChargePoint Trailing 12-Month EPS (GAAP)

Shorter-term EPS analysis can reveal recent business shifts. ChargePoint’s two-year annual EPS growth rate of 38.4% is lower than its five-year average, but still reflects progress. In Q4, the company reported an EPS of -$1.85, an improvement from -$2.89 a year earlier, beating analyst estimates by 6.8%. Wall Street expects ChargePoint’s full-year EPS to improve from -$9.30 to -$6.65 over the next 12 months.

Summary of ChargePoint’s Q4 Performance

ChargePoint’s revenue and EPS both outperformed analyst expectations this quarter. However, guidance for next quarter’s revenue fell short, and EBITDA missed projections, making this a weaker overall quarter. Following the report, shares dropped 5.1% to $6.20.

Despite a challenging quarter, investors should weigh ChargePoint’s valuation, business fundamentals, and recent earnings before making decisions.

Additional Insight: AI Stock Opportunity

Don’t Miss: The $21 AI Application Stock Wall Street Overlooked. While many focus on AI development, one company is already leveraging AI to generate significant profits—and it’s flying under the radar.

AI chip stocks are trading at high valuations, but this company processes a trillion consumer signals monthly using AI and is valued at just a third of the price. This discrepancy won’t last; institutional investors will soon take notice.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Roblox Stock Rises 0.64% Despite Shrinking $460M Volume Ranking 269th Growth vs Profit Dilemma Lingers

Agnico Eagle Mines' Trading Volume Plummets 46% to 271st in Activity Amid Mixed Analyst Outlooks

What Aristeia’s significant investment in IAC reveals about the strategies of savvy investors