The Key to Cryptocurrency Mainstream Adoption: Custody and Licensing, Not Price

The crypto industry is replicating the modernization of Wall Street.

Author: Prathik Desai

Translated by: Block unicorn

Preface

In the late 1960s, Wall Street faced a rather unremarkable problem. As securities trading became increasingly popular, trading activities surged, but the infrastructure supporting these trades remained outdated. Brokers were still settling trades by physically exchanging stock certificates. Couriers dashed around Manhattan, delivering envelopes. Back-office offices were piled high with various forms. The increased trading activity became so severe that the U.S. markets had to close every Wednesday for six consecutive months to allow firms to catch up on the backlog of paperwork.

This ultimately evolved into the notorious "paperwork crisis."

Better couriers or more paperwork couldn’t solve the problem. So, in 1973, they replaced all liquid assets with the Depository Trust Company (DTC). This firm immobilized securities and transformed changes in ownership into ledger updates rather than the exchange of physical stock certificates. The modern American securities markets we know today have resulted from this decision, followed by several iterations and evolutions.

Today, the DTC holds over 1.4 million securities valued at $87.1 trillion, including those issued in the U.S. and more than 130 other countries and regions.

We see a similar narrative throughout financial history. When an asset class is big and popular enough, its growth isn’t just about record-keeping strategies—the deeper driving force is always trust. After DTC was introduced, ordinary investors no longer needed to worry about ownership because trust in a central institution’s record-keeping replaced the need for physical certificates.

The same issue has emerged in the crypto world. Over the past two years, with the rise of exchange-traded funds (ETFs) and other investment vehicles like digital asset treasury bonds, crypto has gained growing mainstream appeal in the U.S.

This development prompted the back office to move quickly, just as the paperwork crisis of the 1960s led to the DTC.

The "paper" in crypto refers to private keys, which operate much like bearer instruments—whoever controls the private key controls the asset. This brings with it a slew of familiar issues for financial institutions: operational control, asset segregation, auditability, bankruptcy, governance, and the fact that losing a private key means permanent loss of assets.

Now, a new trust mechanism is being built around these challenges: the trust bank charter. In today’s article, I’ll explain why so many companies are racing to apply for cryptocurrency custody bank licenses.

The Rush for Charters

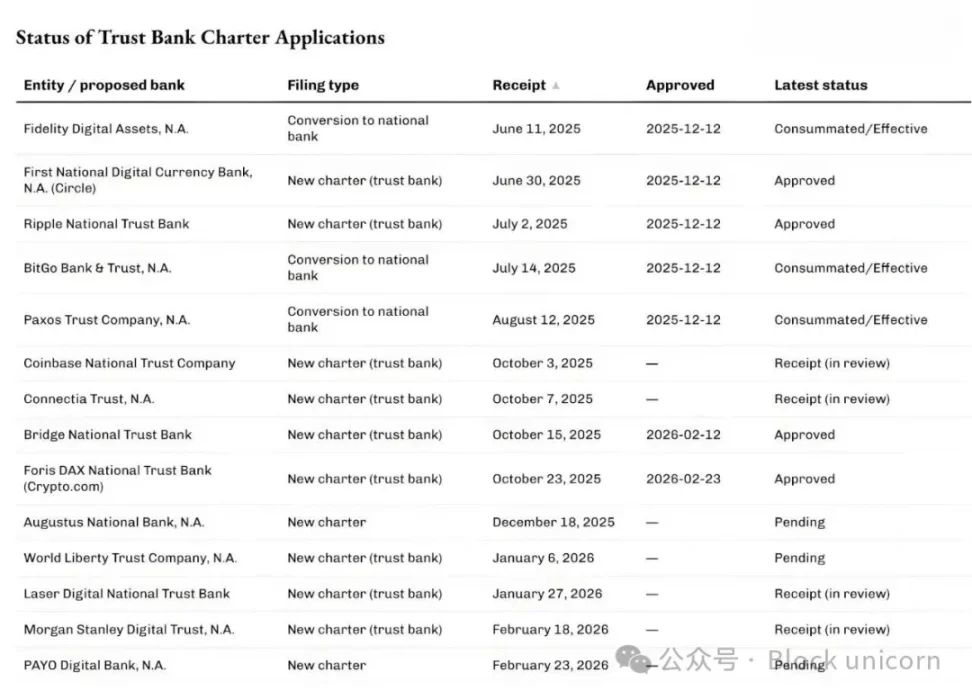

In recent months, the U.S. Office of the Comptroller of the Currency (OCC) has been approving and reviewing an increasing number of applications, with companies aiming to become national trust banks specializing in digital asset custody and stablecoin infrastructure.

On December 12, 2025, the OCC conditionally approved five such applications, including Circle’s First National Digital Currency Bank, Ripple National Trust Bank, as well as conversion applications from BitGo, Fidelity Digital Assets, and Paxos. Subsequently, Stripe’s crypto division Bridge and Crypto.com received preliminary OCC approvals in February 2026.

The queue isn’t limited to crypto-native companies.

Last week, the world’s largest wealth management company, Morgan Stanley, applied to establish a trust bank named Morgan Stanley Digital Trust National Association.

Do you know what all these applications have in common? They are not applying to become traditional banks that handle deposits and loans. Unlike regular banks, these national trust banks cannot accept deposits, make loans, or be insured by the Federal Deposit Insurance Corporation (FDIC). All they offer are custody, safekeeping, and trust management services. You can think of them as specialized record-keeping services for crypto assets.

I believe this is one of the most obvious signs that crypto is changing how traditional financial institutions operate, while the rest of the world remains preoccupied with crypto price volatility.

Bank charters may sound dull, but like many other financial infrastructure innovations, they bring our attention back to the lessons learned from the paperwork crisis. It also underscores that the core of crypto going mainstream is about custody and control.

Why Now?

The rush to apply for charters is closely tied to recent clarifications from the OCC regarding national banks’ authority to conduct crypto-related custody activities. In May 2025, the OCC confirmed that national banks and federal savings associations can buy and sell custodial assets according to client instructions.

In December 2025, the agency further confirmed that banks can function as intermediaries for "riskless principal" crypto trades without holding inventory.

Last week, on February 27, 2026, the OCC clarified that from April 1, 2026, national trust banks can conduct non-fiduciary activities beyond their narrow scope of trust responsibilities.

Why is this important? If you are a company engaged in custody, settlement, reserve management, and related services, this is crucial.

We’ve seen similar scenarios before in finance.

In the early 2010s, a wave of fintech companies launched applications built on partner banks. Although these apps made banking more convenient, they came with problems. While fintech apps controlled the user interface, the partner banks still managed the deposits, core infrastructure, and regulatory authority. When issues arose, responsibility was often diffused among multiple entities, leading to confusion.

The response back then is similar to what we see with crypto now: asserting control over risk and reward.

In 2016, the OCC began to explore specialized national bank charters for fintech companies. Two years later, the OCC began accepting applications from non-depository fintechs engaging in core banking activities.

Although courts rejected the possibility of granting bank charters to non-depository institutions, fintechs continued to reduce their reliance on partner banks. A few eventually became full-service banks through more traditional, and sometimes acquisition-driven, routes.

Varo started as a fintech and, in 2020, received a full-service national bank charter. Jiko became a bank through the acquisition of a small national bank. SoFi, in 2022, received conditional approval to become a full-service national bank through an acquisition.

The current rush for national trust bank charters follows a similar pattern—except this time, Washington is also drafting new safeguards for digital assets.

The legislative backdrop to all these developments makes it even clearer why companies pursuing national trust bank charters are interested in more than just custody services for digital assets.

In July 2025, President Donald Trump signed the GENIUS Act, establishing a federal framework for payment stablecoins. Several companies seeking the trust bank structure have explicitly stated their intent to operate stablecoin and related reserve businesses under that federal regulatory regime.

Both Bridge and Circle referenced this in their respective announcements.

This answers the first aspect of "why now." Clearer regulatory policies are opening new value chains for established firms—both traditional and crypto-native—to expand their businesses.

The second aspect concerns market structure.

Institutional crypto investment has shifted towards vehicles that resemble traditional financial products, such as ETFs, funds, and managed accounts. These structures require custodians that can meet legal and operational requirements.

If you think there’s no demand for centralized crypto investment, you are completely mistaken. The ongoing construction of crypto ETF infrastructure is proof enough.

In April 2025, BlackRock, the world’s largest asset and crypto fund manager, added Anchorage Digital Bank as a bitcoin custodian for its iShares Bitcoin Trust, in addition to its existing partner Coinbase. BlackRock cited this as part of "ongoing risk management" to meet growing retail and institutional demand.

What value do financial giants like Morgan Stanley, with a market cap of $9 trillion, see in these charters?

One recent sign appeared less than two weeks ago during a fireside chat at the "Enterprise Bitcoin" conference. Phong Le, CEO of Strategy (formerly MicroStrategy), said, "If anyone can help the world 'take the orange pill,' it would be Morgan Stanley." Amy Oldenburg, head of Digital Asset Strategy at Morgan Stanley, replied, "That may be accurate."

What’s Changing?

Once you piece these developments together, the charter boom looks less like a crypto-specific story and more like the kind of evolution we saw with the DTC.

As crypto grows into a financial asset, both retail and institutional investors need a place to store private keys—and it must be an institution acceptable to lawyers, auditors, and regulators. The national trust bank charter is a way to solve this problem at scale.

Next comes the business economics of this line. Custody might seem like a low-fee business. Beginning in Q1 2025, Coinbase no longer discloses custody fee income as a standalone line item and instead includes it under "Other subscription and services revenue." However, the complexity of custody goes far beyond what is apparent on the surface.

Whoever controls custody, controls the collateral—and that collateral sets the financing capacity for these institutions. Financing determines leverage, and leverage, in turn, determines trading volume. Ultimately, trading volume translates into revenue.

In 2025, global securities lending revenue is expected to reach $15.3 billion, with loan balances exceeding $4 trillion. State Street, a custody giant, reported total revenue of $13.94 billion in 2025. Of this, services revenue—comprising custody, accounting and fund administration, record-keeping, and client reporting—accounted for about 40% ($5.32 billion).

So, although custody alone may not generate substantial revenue, the ancillary services built around custody can serve as repeatable sources of income.

The reason DTC became indispensable is that it enabled markets to scale without being overwhelmed by paperwork. Today, the DTC has evolved into a fully functional system; it’s far more than a depository. It offers settlement, handles corporate actions, and supports underwriting. It has become a comprehensive ecosystem centered on updating ownership records.

Obtaining a crypto custody license could bring similar benefits to these applicants. In addition to acting as a vault, they can provide authorized ledger interfaces.

The license allows these firms to offer credibility to clients in recording, segregating, transferring, and auditing digital asset ownership. They don’t have to be deposit-taking banks to do this—they can achieve it through a leaner balance sheet and a more focused approach.

But there are plenty of critics of the trust charter as well.

Traditional banking advocates argue that these charters could serve as a "back door" into the banking system, without taking deposits or facing the same broad public obligations. Banks are fiercely debating where to draw that line.

Even as the debate continues, regulatory changes are underway. The OCC’s conditional approvals may not be final, but they send an important message: As much as crypto touts self-custody, the industry is now massive enough that back-office operations cannot be overlooked.

I believe if the industry treats the trust bank charter boom as just a crypto phenomenon, they’re mistaken. It’s better seen as a natural evolution, where participants seek to create value by addressing inefficiencies in their industry.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Berkshire’s Abel Commits Entire Salary to Purchasing Company Shares

ITV maintains that the Sky sale remains in progress despite a decline in advertising income

AREC's ReElement Increases Advanced Rare Earth Lab Capabilities

Q4 Overview: Comparing Radian Group (NYSE:RDN) with Other Property & Casualty Insurance Equities