BJ's (NYSE:BJ) Reports Q4 CY2025 Revenue Matching Expectations

BJ’s Wholesale Club Q4 2025 Earnings Recap

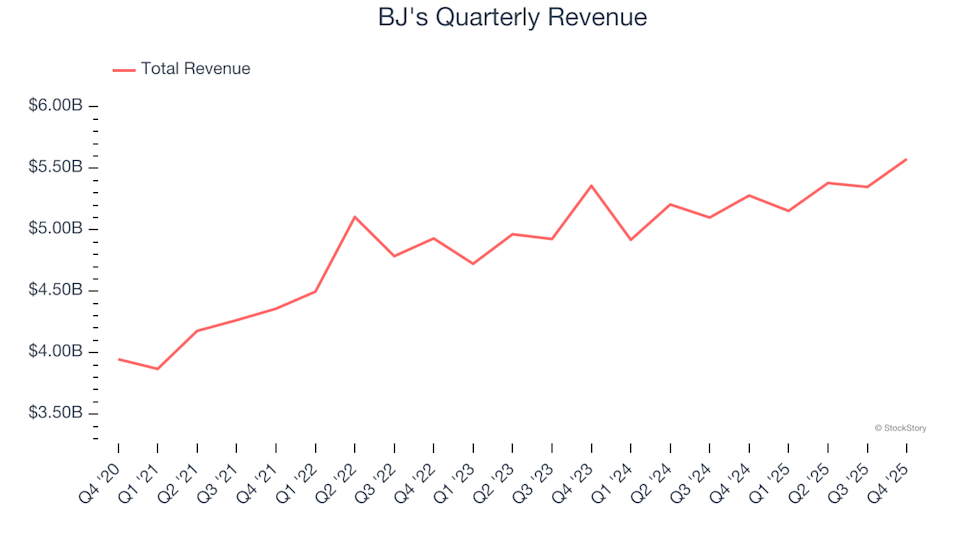

BJ’s Wholesale Club (NYSE:BJ), a retailer offering exclusive membership discounts, reported its fourth-quarter 2025 results with revenue reaching $5.58 billion—a 5.6% increase compared to the same period last year, matching market expectations. Adjusted earnings per share came in at $0.96, surpassing analyst forecasts by 3.3%.

Highlights from BJ’s Q4 2025 Report

- Total Revenue: $5.58 billion, slightly above the $5.55 billion consensus (5.6% annual growth)

- Adjusted EPS: $0.96, beating estimates of $0.93 by 3.3%

- 2026 Adjusted EPS Guidance: Midpoint at $4.50, which is 3.4% below analyst projections

- Operating Margin: 3.2%, consistent with the prior year’s quarter

- Free Cash Flow Margin: 3.4%, up from 2.1% a year ago

- Store Count: 263 at quarter’s end, up from 250 the previous year

- Same-Store Sales: Increased 1.6% year over year (compared to 4% growth last year)

- Market Cap: $13.08 billion

About BJ’s Wholesale Club

BJ’s Wholesale Club is a membership-based chain catering to value-focused shoppers, offering a wide selection of groceries, home goods, electronics, and appliances—often in bulk quantities.

Revenue Trends and Growth

Examining long-term sales trends can reveal much about a company’s strength. While any business can have a strong quarter, sustained growth is a sign of quality. Over the past year, BJ’s generated $21.46 billion in sales, making it a major player in the retail sector. Its established brand helps drive consumer decisions, but its large size can make it challenging to find new growth opportunities. To accelerate revenue, BJ’s may need to adjust pricing strategies or expand internationally.

Over the last three years, BJ’s has posted a modest 3.6% compound annual growth rate in sales, with limited gains at existing stores.

In the most recent quarter, revenue climbed 5.6% year over year, aligning with analyst expectations at $5.58 billion.

Looking forward, analysts anticipate BJ’s revenue will grow by 6.1% over the next year, a faster pace than recent years. This suggests that new product offerings could help drive stronger sales growth.

Bonus Insight: 3 Emerging Platforms Outpacing Amazon, Google, and PayPal

Major tech giants like Amazon and Google achieved dominance by targeting overlooked markets and building strong competitive advantages. Today, three new platforms are following a similar path and growing even faster.

Store Expansion and Performance

Store Count

At the end of the latest quarter, BJ’s operated 263 stores. The company has been expanding rapidly, averaging 3.7% annual growth in store count over the past two years—outpacing much of the retail sector.

Opening new locations typically signals that a retailer is investing in growth to meet rising demand, especially in underserved areas.

Same-Store Sales Analysis

While expanding the number of stores is important, evaluating same-store sales gives a clearer picture of organic growth. This metric tracks sales at locations open for at least a year, helping to assess underlying demand.

Over the past two years, BJ’s has seen steady but modest same-store sales growth, averaging 1.8% annually—slower than many competitors. This suggests the company may need to focus on increasing customer traffic and operational efficiency before further expansion.

In the latest quarter, same-store sales rose 1.6% year over year, consistent with recent trends.

Summary and Outlook

BJ’s slightly exceeded gross margin expectations and met revenue forecasts this quarter. However, its full-year earnings guidance fell short, and EBITDA was a bit below analyst estimates, making for a somewhat disappointing quarter. Following the report, shares dropped 3.1% to $96.90.

While the latest results were mixed, investors may want to consider whether this presents a buying opportunity. Factors such as valuation, business fundamentals, and recent performance should all be weighed.

These three platforms are following the same winning strategy as Amazon’s early days. Early investors in these companies could see significant returns.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Nasdaq 100 Stocks We’re Keeping an Eye On

Nasdaq Texas Launches with Inaugural Dual Listings

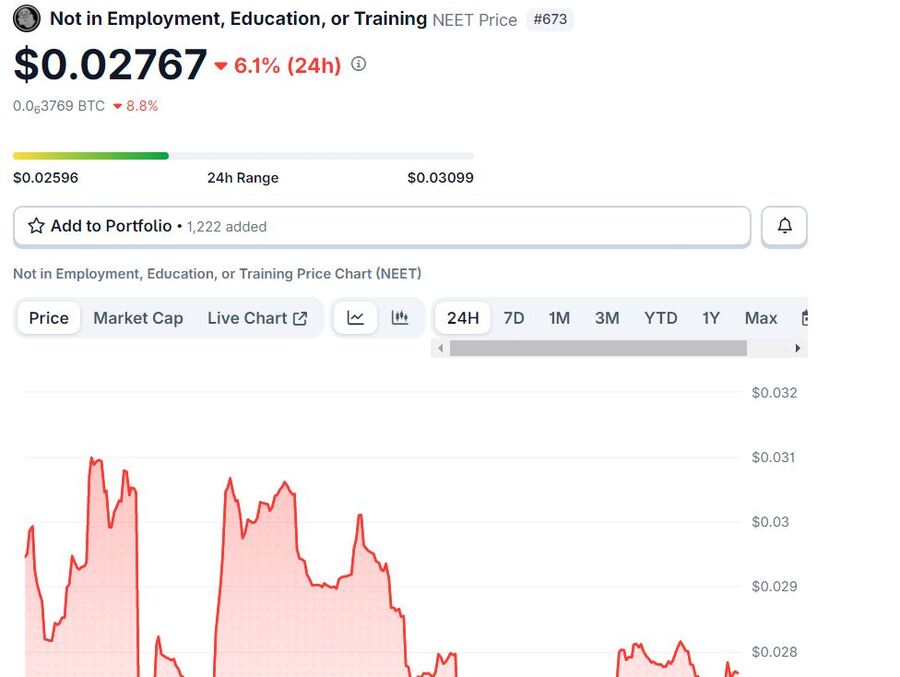

NEET’s 290.1% Price Surge On Spotlight As Analyst Eyes Huge Upside

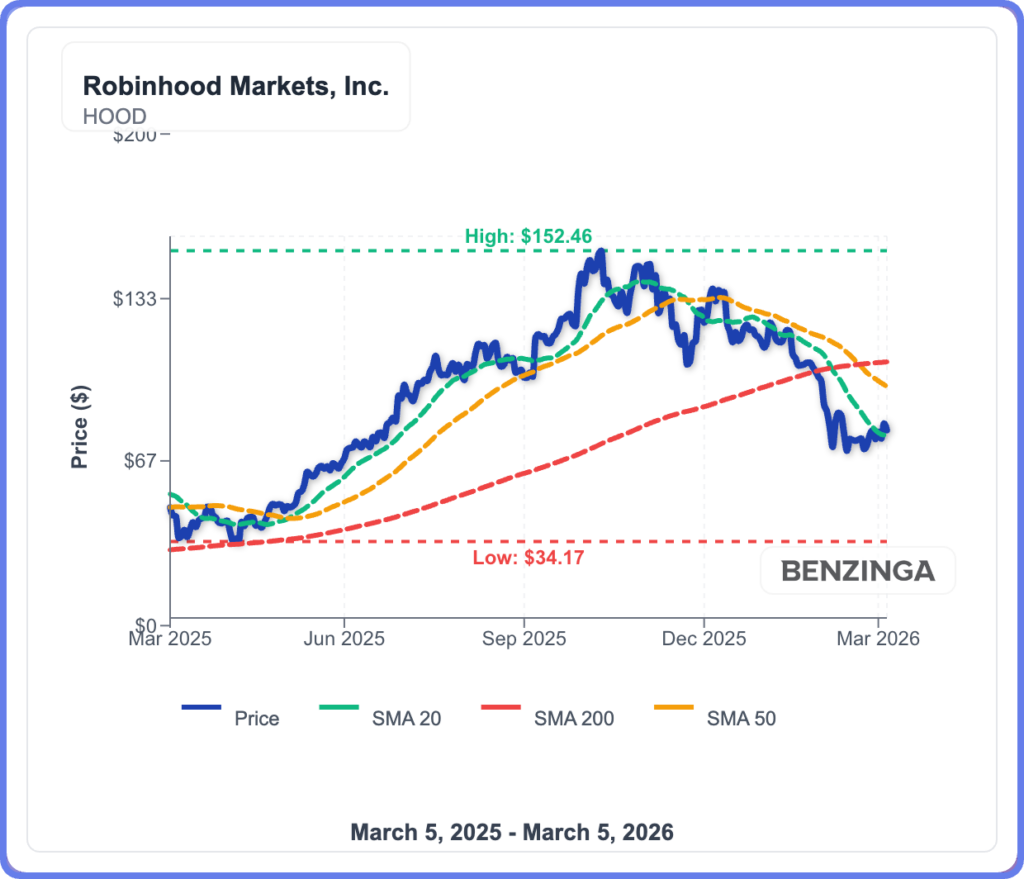

Robinhood Launches Platinum Card, Family Accounts - HOOD Falls 4% Anyway