Should You Consider Investing in Barrick Mining Shares Following a 61% Surge Over the Past Six Months?

Barrick Mining Corporation Surges on Gold Price Rally

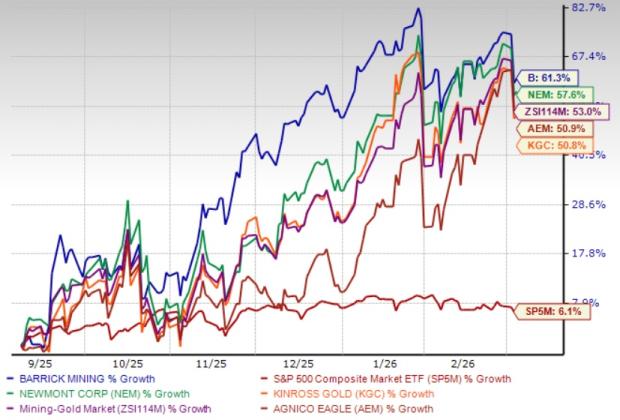

Over the past half year, Barrick Mining Corporation's stock has soared by 61.3%, fueled by unprecedented gold price highs amid global geopolitical instability, economic uncertainty, and trade tensions. The company's robust earnings, driven by higher realized gold prices, have also contributed to this impressive performance.

Barrick has outpaced both the Zacks Mining – Gold industry, which rose 53%, and the S&P 500, which gained 6.1% during the same period. Other leading gold miners, including Newmont Corporation, Kinross Gold Corporation, and Agnico Eagle Mines Limited, saw their shares climb 57.6%, 50.8%, and 50.9%, respectively.

Six-Month Price Movement

Source: Zacks Investment Research

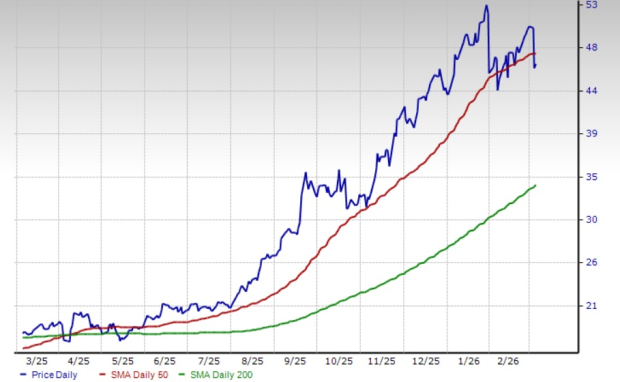

On March 3, 2026, Barrick's stock dipped below its 50-day simple moving average (SMA) but remains above the 200-day SMA, indicating a continued long-term upward trend. Since the golden crossover on April 9, 2025, the 50-day SMA has consistently stayed above the 200-day SMA, signaling ongoing bullish momentum.

Trading Below the 50-Day SMA

Source: Zacks Investment Research

To better understand Barrick's outlook, let's examine the company's core fundamentals.

Major Projects Set to Drive Barrick’s Growth

Barrick is advancing several significant gold and copper projects that are expected to boost its production in the coming years. Key initiatives include the Goldrush mine, Pueblo Viejo plant expansion and mine life extension, Fourmile, Lumwana Super Pit, and the Reko Diq project. All are progressing on schedule and within budget, setting the stage for future growth.

- Goldrush: Targeting 400,000 ounces of annual production by 2028.

- Fourmile: 100% owned by Barrick, this project is delivering grades twice as high as Goldrush and is on track to become a Tier One mine, with a prefeasibility study underway.

- Reko Diq: Located in Pakistan, this copper-gold project aims for annual output of 460,000 tons of copper and 520,000 ounces of gold in its second phase, with first production expected by late 2028.

- Lumwana Super Pit: The $2 billion expansion is transforming the mine into a Tier One copper asset, expected to yield 240,000 tons of copper per year.

Barrick notes that the Lumwana expansion marks a dramatic turnaround, making it a cornerstone of both the company’s copper portfolio and Zambia’s economic strategy.

Strong Liquidity and Cash Flow Support Barrick’s Ambitions

Barrick’s financial health is robust, providing flexibility for new investments, exploration, and acquisitions, while also supporting shareholder returns and debt reduction. At the close of 2025, the company held approximately $6.7 billion in cash and equivalents. Operating cash flow for the fourth quarter reached $2.7 billion, a 13% increase year-over-year, while free cash flow grew 9% to $1.6 billion. For the full year, operating cash flow surged 71% to $7.7 billion, and free cash flow jumped 194% to $3.9 billion.

In 2025, Barrick returned $2.4 billion to shareholders through dividends and buybacks, including $1.5 billion in share repurchases and a fourth-quarter dividend of $0.42 per share—a 140% increase from the prior quarter. The company also introduced a new dividend policy targeting a payout of 50% of attributable free cash flow annually.

At current prices, Barrick offers a 3.6% dividend yield with a payout ratio of 29%, indicating sustainability. The five-year annualized dividend growth rate stands at roughly 5.9%.

High Gold Prices Bolster Margins and Cash Flow

The surge in gold prices has significantly enhanced Barrick’s profit margins and cash generation. In 2025, gold reached record levels, driven by aggressive trade policies, including sweeping tariffs under President Donald Trump, which heightened global trade tensions and spurred central banks to increase gold reserves.

Although gold prices have retreated from their January 2026 peak, they remain elevated. Ongoing geopolitical conflicts, a weaker U.S. dollar, new tariff threats, and concerns about Federal Reserve independence pushed gold to nearly $5,600 per ounce in late January. After a brief correction below $4,900, bargain buying lifted prices back above $5,000. Most recently, gold surged past $5,400 per ounce following joint U.S.-Israel strikes on Iran, which escalated tensions and disrupted oil markets. While prices have since moderated due to a stronger dollar and tempered expectations for Fed rate cuts, they remain above $5,100 per ounce, supported by persistent geopolitical risks and central bank demand.

Continued safe-haven buying, especially amid Middle East conflicts and broader economic uncertainty, is expected to keep gold prices strong.

Rising Production Costs Present a Challenge

Barrick is facing increased costs, which could pressure its margins. In the fourth quarter, total cash costs per ounce of gold and all-in-sustaining costs (AISC)—a key industry metric—rose by about 15% and 9% year-over-year, respectively. The AISC reached $1,581, up from the previous year, and climbed 10% to $1,637 for 2025.

Production declines, partly due to the suspension of the Loulo-Gounkoto mine, contributed to higher unit costs. Barrick’s consolidated gold output dropped 19% year-over-year to 871,000 ounces in the fourth quarter and fell 17% for the full year.

For 2026, Barrick anticipates AISC between $1,760 and $1,950 per ounce, a notable increase from the prior year. Cash costs are projected at $1,330–$1,470 per ounce, up from $1,199 in 2025. The rise is attributed to lower ore grades, higher input costs, and increased gold price assumptions, as well as a higher cost base at Loulo-Gounkoto as operations ramp up following the restoration of control in December 2025.

Upward Earnings Revisions Reflect Optimism

Analysts have raised their earnings forecasts for Barrick over the past two months. The Zacks Consensus Estimate for 2026 and 2027 earnings has been revised upward, now pointing to a 49.6% and 19.1% year-over-year increase, respectively.

Source: Zacks Investment Research

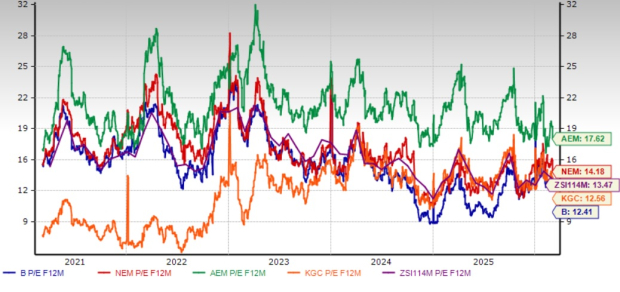

Barrick’s Valuation Remains Attractive

Barrick’s stock currently trades at a forward price-to-earnings ratio of 12.41, about 7.9% below the industry average of 13.47. The stock is also valued at a discount compared to Agnico Eagle, Newmont, and Kinross Gold. Barrick, Newmont, and Kinross all hold a Value Score of B, while Agnico Eagle’s Value Score is D.

Price/Earnings Comparison: Barrick vs. Peers

Source: Zacks Investment Research

Investor Takeaway: How to Approach Barrick Stock

Barrick’s ongoing production initiatives, strong balance sheet, positive earnings outlook, compelling valuation, and reliable dividend yield create a favorable investment profile. Elevated gold prices should continue to support profitability and cash flow, though rising production costs warrant careful monitoring.

For current shareholders, maintaining a position in this Zacks Rank #3 (Hold) stock appears to be a prudent choice.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Gold Holds Above $5,100 as Geopolitical Tensions Bolster Safe-Haven Demand

BlackBerry's Profitability Disconnect: A Behavioral Finance Analysis

Dollar-cost averaging Bitcoin is safest strategy for long-term gains: Data