3 Compelling Reasons to Invest in Modine Shares Even with Their High Valuation

Modine Manufacturing: Is There Still Upside After a Strong Rally?

Modine Manufacturing (MOD) shares have experienced a significant rally this year, climbing approximately 57%. The stock is now trading at a forward 12-month P/E ratio of nearly 29.8, which is considerably higher than the industry average of 11.9. This elevated valuation has led some to wonder if the stock’s impressive run is nearing its end.

Image Source: Zacks Investment Research

Despite the premium price, Modine’s strong foothold in rapidly growing sectors, improving profit margins, and disciplined management approach indicate that the company’s growth prospects remain promising. Here are three compelling reasons why Modine could still be a smart investment, even at current levels.

1. Momentum in Climate Solutions Division

Modine has been transitioning into a specialized provider of climate solutions, expanding this segment through strategic acquisitions that enhance its expertise and customer base.

In recent years, Modine has bolstered its Climate Solutions portfolio by acquiring several businesses. In fiscal 2024, the company purchased Scott Springfield Manufacturing and key assets from Napps Technology. The expansion continued in fiscal 2026 with the addition of AbsolutAire, L.B. White, and Climate by Design International. These moves have strengthened Modine’s position in HVAC, specialty heating, and advanced air-handling markets.

To streamline operations, Modine is also restructuring its business. The company plans to merge its Performance Technologies segment with Gentherm (THRM) via a Reverse Morris Trust transaction, expected to finalize in the fourth quarter of 2026. This will leave Modine as a dedicated, diversified climate solutions company.

The Climate Solutions segment is showing operational improvements as well. Margins increased sequentially in the third quarter of fiscal 2026, and management anticipates margins between 20% and 21% in the fourth quarter. Modine aims to finish fiscal 2026 with record-high quarterly margins and is targeting 20%–23% margins for fiscal 2027, reflecting the success of its strategic shift.

2. Surging Demand for Data Center Cooling Driven by AI

One of Modine’s major growth engines is the booming demand for data center cooling, fueled by the rapid expansion of artificial intelligence. As AI accelerates the construction of data centers worldwide, efficient cooling has become a top priority for operators.

Advanced cooling solutions are now essential for data center infrastructure, often dictating how quickly large-scale facilities can grow. This trend is driving robust demand for innovative cooling technologies.

Modine is well-positioned to capitalize on this opportunity, alongside peers such as Vertiv Holdings (VRT) and Johnson Controls International (JCI), as data center operators increase investments in cooling and efficiency solutions.

In the third quarter of fiscal 2026, Modine’s data center-related sales jumped 31% sequentially. Management expects further growth in the fourth quarter, with segment revenues projected to surpass $400 million.

Modine’s order backlog is at record levels, split between chillers and other data center products, providing nearly five years of revenue visibility.

The company anticipates its data center business will grow at a compound annual rate of 50%–70% over the next two years. To support this trajectory, Modine is expanding capacity, with new chiller production lines scheduled for fiscal 2028. The current capital investment plan could support up to $3 billion in data center revenue over time, and long-term agreements with customers further enhance revenue predictability.

3. Operational Excellence Boosts Profitability

In addition to pursuing growth, Modine is focused on enhancing profitability through disciplined operational practices, notably the adoption of the 80/20 operating model.

This approach—prioritizing the most profitable products, customers, and markets—enables Modine to allocate resources efficiently and reduce complexity. By concentrating on high-return areas, the company aims to streamline its operations and drive sustainable growth.

The benefits of this strategy are already evident. In fiscal 2025, Modine increased gross margins despite lower overall sales, thanks to these operational improvements. The company also closed a technical service center in Germany, made targeted workforce adjustments, and shifted product lines to optimize global capacity and improve supply chain efficiency.

Looking ahead, management expects these initiatives to continue supporting profitability. For fiscal 2026, Modine forecasts revenue growth of 20%–25%, reaching between $3.10 billion and $3.23 billion. Adjusted EBITDA is projected to rise 16%–21%, to a range of $455 million–$475 million.

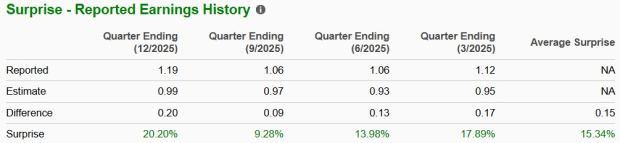

Consistent Earnings Surprises and Upward Estimate Revisions

Modine has exceeded earnings expectations in each of the last four quarters.

Image Source: Zacks Investment Research

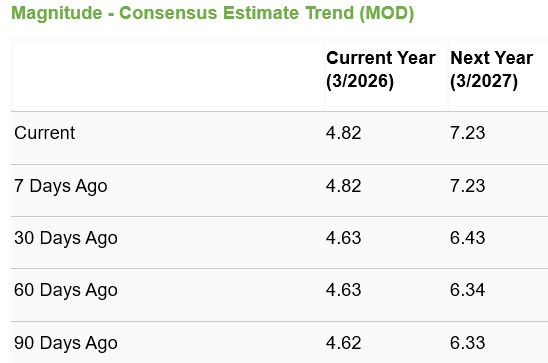

Analyst consensus for fiscal 2026 points to sales and earnings per share growth of 21% and 19%, respectively. For fiscal 2027, consensus estimates suggest further increases of 21% in sales and a 50% jump in earnings per share compared to 2026 projections.

Notably, these estimates have been revised upward in the past month, reflecting growing analyst confidence in Modine’s earnings outlook.

Image Source: Zacks Investment Research

Currently, MOD holds a Zacks Rank #1 (Strong Buy).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Mercury Systems (MRCY) Shares Rise 15.6% Following Recent Earnings: Will the Momentum Last?

Why Has Cabot (CBT) Dropped 4.9% Following Its Most Recent Earnings Announcement?

Why Has Amdocs (DOX) Dropped 5.9% Following Its Most Recent Earnings Announcement?

Coherent Surges 325% in a Year: How Should Investors Play the Stock?