3 Stocks We Believe Are Overhyped and Carry Significant Risk

Stocks Near Their 52-Week Highs: A Closer Look

Several stocks have recently approached their highest prices in the past year. While this can indicate robust company performance, favorable industry trends, or positive investor sentiment, it’s important to remember that momentum alone doesn’t guarantee lasting success. Below, we highlight three stocks that may be overextended and suggest alternatives worth your attention.

Restaurant Brands International (QSR)

One-Month Performance: +2.5%

Restaurant Brands International (NYSE:QSR) was created through a merger and now operates major fast-food names including Burger King, Tim Hortons, and Popeyes.

Reasons for Caution with QSR

- Projected sales growth of 4.3% over the next year suggests a slowdown compared to its six-year average.

- Operating costs have increased faster than revenue, leading to a 5.4 percentage point drop in operating margin over the past year.

- Despite revenue gains, earnings per share have only grown by 5.1% annually over six years, indicating less profitable incremental sales.

Currently, QSR trades at $72.10 per share, with a forward price-to-earnings ratio of 17.8.

Assurant (AIZ)

One-Month Performance: -4.4%

Assurant (NYSE:AIZ), established in 1892, specializes in insurance solutions for significant consumer purchases such as electronics, vehicles, homes, and appliances.

Why We’re Hesitant About AIZ

- Net premiums have grown at just 4.8% annually over the past five years, lagging behind industry peers due to the company’s scale.

- Earnings per share increased by only 13.1% annually over the last two years, underperforming the sector average.

- Book value per share has risen by just 2.8% annually over five years, which is below expectations for insurance companies of this size.

Assurant is priced at $231.89 per share, with a forward price-to-book ratio of 1.8.

Atmus Filtration Technologies (ATMU)

One-Month Performance: +5.2%

After separating from Cummins in 2023, Atmus Filtration Technologies (NYSE:ATMU) now produces filtration systems for trucks, construction, and agricultural equipment, focusing on reducing emissions and engine protection.

Concerns About ATMU

- Sales have grown by just 4.1% annually over the past two years, which is below the industrial sector average.

- High production costs have resulted in a relatively low gross margin of 26.3%, requiring increased sales volume to compensate.

- Free cash flow margin has declined by 3.4 percentage points over five years, reflecting higher investments to maintain market share.

Atmus trades at $63.74 per share, equating to a forward P/E of 21.3.

Stocks We Prefer

Don’t Miss: Top 5 Momentum Stocks

The optimal time to invest in outstanding companies is when the market starts to recognize their potential. These businesses not only have strong fundamentals, but are also experiencing positive momentum right now.

Discover which stocks our AI system is highlighting this week.

Past picks from our list include well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, and lesser-known companies such as Tecnoglass, which delivered a 1,754% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

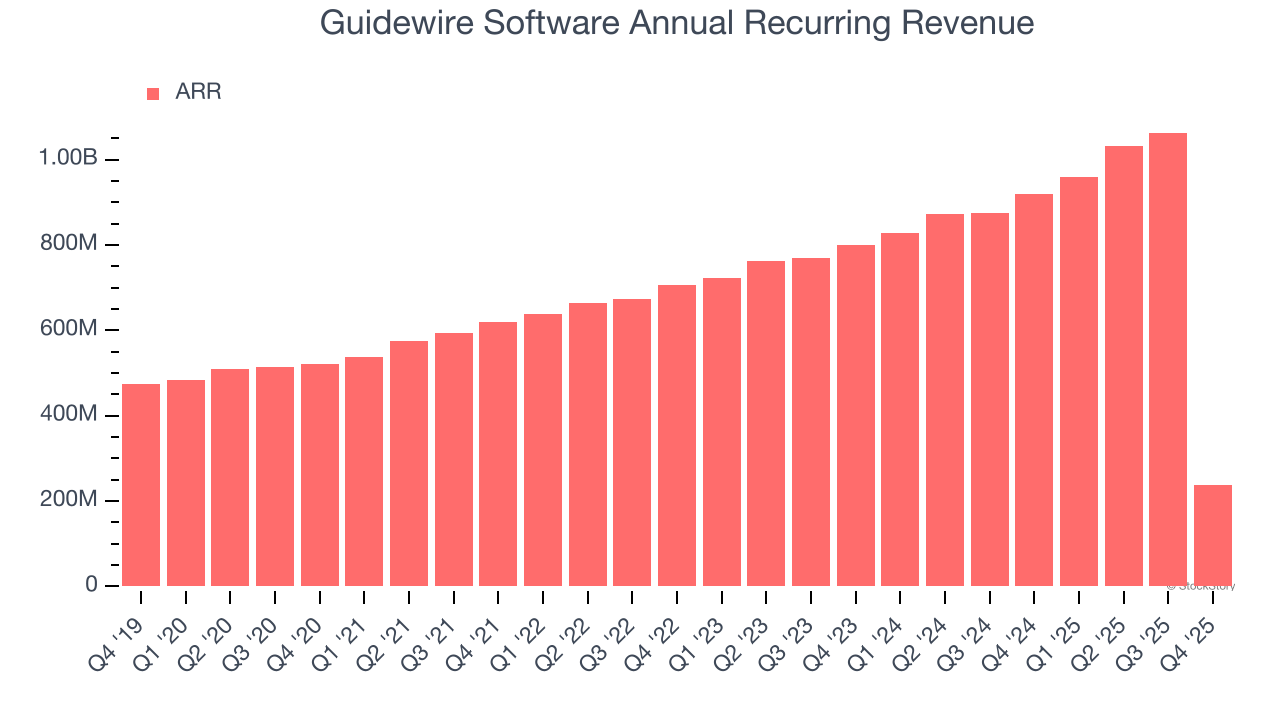

Guidewire Software's (NYSE:GWRE) Q4 CY2025 Sales Top Estimates

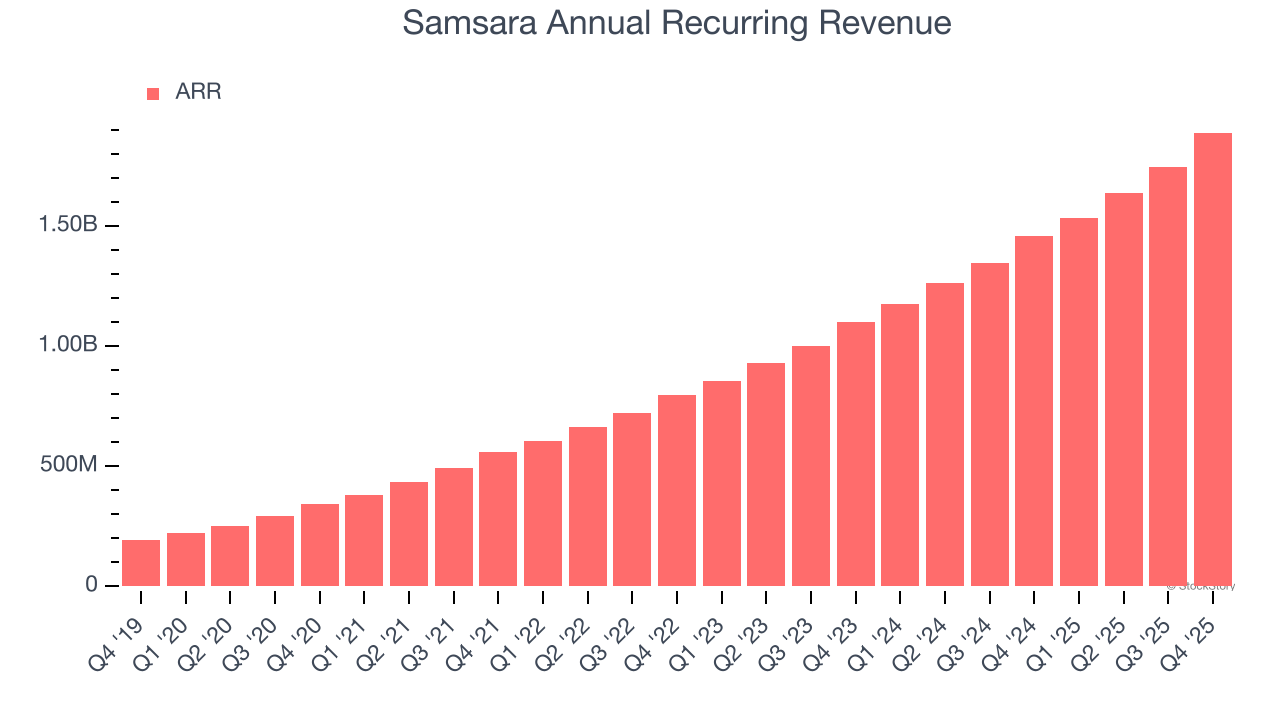

Samsara's (NYSE:IOT) Q4 CY2025: Beats On Revenue, Stock Jumps 14.2%

Crypto Market Crash: Top Analyst Reveals What’s Next For Bitcoin, Ethereum and XRP

MannKind Announces Settlement of Convertible Senior Notes