AMAT Surges 33.4% Over Past 3 Months: Should You Buy, Sell, or Keep the Shares?

Applied Materials Outpaces Sector Peers With Strong Three-Month Gains

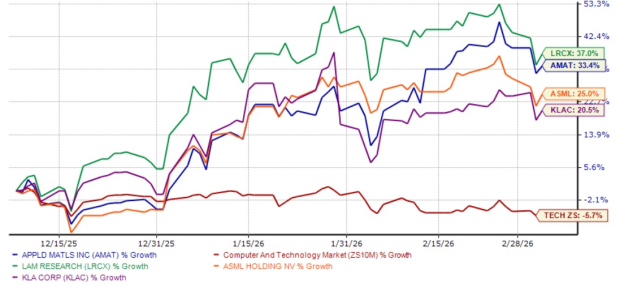

Over the past quarter, shares of Applied Materials (AMAT) have surged by 33.4%, significantly outperforming the Zacks Computer and Technology sector, which saw a 5.7% decline during the same period. Compared to its competitors, AMAT outshined both ASML Holding and KLA Corporation, though it trailed behind Lam Research in terms of stock performance.

AMAT’s Recent Stock Performance

Source: Zacks Investment Research

In the last three months, ASML Holding, KLA Corporation, and Lam Research have posted gains of 25%, 20.5%, and 37%, respectively. With AMAT’s notable rise and its standing among other wafer fabrication equipment (WFE) companies, investors are considering whether now is the right time to buy, sell, or hold AMAT shares.

AMAT’s Comprehensive WFE Portfolio Sets It Apart

The wafer fabrication equipment industry involves several critical manufacturing steps. Applied Materials stands out by offering the most extensive and diversified range of solutions, covering areas such as deposition, materials engineering, etching, metrology, and packaging. In contrast, many of its rivals focus on just one or two segments.

For example, both Applied Materials and KLA Corporation provide advanced systems for wafer inspection, yield improvement, and process control. Lam Research, meanwhile, produces atomic layer deposition tools similar to those from AMAT. ASML and AMAT both target advanced semiconductor nodes, but ASML specializes in lithography systems like EXE and NXE, while AMAT’s etching lineup includes products such as Sym3 Magnum Etch and Centura Xtera.

AMAT’s offerings in CVD deposition (Producer GT and SE), atomic layer deposition (Olympia ALD), and physical vapor deposition (Endura PVD) compete directly with Lam Research. Its metrology and inspection platforms, including PROVision eBeam and SEMVision, rival those from KLA Corporation.

This wide-ranging product suite allows AMAT to integrate its equipment across various manufacturing processes, reducing dependence on any single technology cycle and supporting stronger margins. Analyst estimates for AMAT’s fiscal 2026 earnings now project a 16.5% increase, with forecasts trending higher over the past month.

Source: Zacks Investment Research

Growth Drivers: Logic, DRAM, and Advanced Packaging

Applied Materials anticipates that its leading-edge foundry, logic, DRAM, and high-bandwidth memory (HBM) segments will be the fastest-growing areas in 2026. The company’s logic business is benefiting from the industry’s transition from FinFET to Gate-All-Around (GAA) transistors and the adoption of backside power delivery.

AMAT is at the forefront of technologies such as GAA transistors at 2nm and below, HBM stacking, hybrid bonding, and 3D device metrology—key components for next-generation semiconductor manufacturing. Recent product launches like Xtera epi, Kinex hybrid bonding, and PROVision 10 eBeam are expected to fuel further growth through 2026 and beyond.

Demand for AMAT’s DRAM solutions is rising as customers invest in advanced 6F² nodes and high-bandwidth memory, driven by the expansion of AI applications. In its first-quarter 2026 earnings report, AMAT highlighted record results in both logic and DRAM, reflecting major industry shifts.

The company’s HBM chips are becoming more complex and larger, requiring three to four times more wafer starts per bit compared to standard DRAM, which increases equipment demand—a positive trend for AMAT as the HBM market grows. AMAT aims to reach $3 billion in HBM-related revenue in the coming years.

Future HBM generations are expected to utilize hybrid bonding, an area where AMAT is a leading innovator. The company’s advancements in advanced packaging, especially 3D chiplet stacking, position it well as AI chips become increasingly heterogeneous. New product introductions and progress in cold field emission e-beam technology further enhance AMAT’s competitive edge.

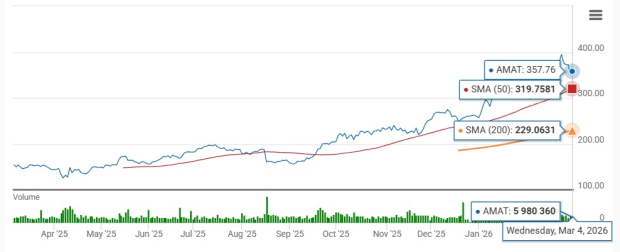

Technical Indicators Point to Continued Strength

AMAT’s stock is currently trading above both its 200-day and 50-day simple moving averages, signaling ongoing bullish momentum.

AMAT’s Moving Average Chart

Source: Zacks Investment Research

Should You Buy AMAT Stock Now?

With its extensive WFE product lineup spanning deposition, materials engineering, etching, metrology, and packaging—and strong momentum in foundry, logic, DRAM, and high-bandwidth memory—Applied Materials is well-positioned within the semiconductor supply chain. Given these strengths, investors may want to consider adding this Zacks Rank #2 (Buy) stock to their portfolios.

Quantum Computing: The Next Big Opportunity

Artificial intelligence has already transformed investing, and its intersection with quantum computing could unlock unprecedented opportunities for wealth creation.

Now is your chance to position your investments at the forefront of this technological shift. Our special report, Beyond AI: The Quantum Leap in Computing Power, reveals lesser-known stocks that could lead the quantum computing revolution and deliver significant returns to early investors.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

BlackBerry's Profitability Disconnect: A Behavioral Finance Analysis

Dollar-cost averaging Bitcoin is safest strategy for long-term gains: Data

Walmart Stock Is Taking A Dive: What's Happening?

Solana Eyes $90.6 Trigger Point as $83 Support Holds and Liquidation Pressure Builds