Verizon Shares Rise 19.4% in a Year: Should You Invest Now?

Verizon Communications Inc. VZ has gained 19.4% in the past year against the Wireless National industry’s decline of 2.1%. The stock has underperformed the Zacks Computer & Technology sector during this time period.

Image Source: Zacks Investment Research

The company has outperformed its peers like AT&T Inc. T and T-Mobile US, Inc. TMUS. Shares of AT&T have gained 10.6%, while T-Mobile has declined 16.4% during this period.

Verizon Rides on Subscriber Gain, AI Telematics Adoption

Verizon is benefiting from solid traction in the Consumer segment. Strong postpaid phone subscriber momentum is the major growth driver. As of the fourth quarter of 2025, the company’s wireless retail connections were 115.9 million, with wireless retail postpaid connections being 95.7 million, up from prior year reported figures of 115.3 million and 95.2 million, respectively. Consumer postpaid phone net adds were 551,000, the highest in five years.

Verizon’s convergence strategy, which is actually selling wireless and broadband as a bundled solution at a reasonable price, is driving customer additions. When customers get dependent on multiple services from a single vendor, it becomes difficult for them to change service providers. This higher switching friction lowers churn rate and boosts customer retention.

Management is relying on competitive offers to bring customers more value rather than just price hikes. Revenue growth is, for the most part, supported by subscriber expansion rather than ARPU inflation. A retail postpaid phone churn of 0.95% indicates healthy customer retention. The company’s wireless retail postpaid ARPA was $147.36 at the end of the fourth quarter, up 1.2% year over year.

Fixed wireless access (FWA) broadband remains a major growth engine in this segment. Q4 fixed wireless net adds were 319,000. Total broadband net adds were 372,000, highlighting strengths in both FWA and fiber. Owing to these factors, revenues from the Consumer segment rose to $28.44 billion, up 3.2% year over year.

The company has been taking several initiatives to diversify its product offerings amid growing competition in the U.S. wireless market. It is developing its AI native telematics solutions to expand into fleet management, logistics sector. Verizon Connect solution suite consists of software, hardware and connectivity solutions that help companies track vehicles, monitor drivers and optimize fleet operations. Per a report from Mordor Intelligence, the fleet management solutions market is projected to witness a 15.32% compound annual growth rate from 2025 to 2030. Verizon is set to gain from this market trend.

VZ Affected by Stiff Competition and High Debt Burden

The U.S. wireless market is highly competitive and saturated. Intensifying competition with a relatively fixed pool of customers is putting pressure on pricing. It could limit the company’s ability to attract and retain customers and may adversely affect its operating and financial results. During the fourth quarter of 2025, Verizon registered 53,000 Fios Video net losses, reflecting the ongoing shift from traditional linear video to over-the-top offerings.

Companies like AT&T and T-Mobile are doubling down on 5G network expansion. Following the acquisition and deployment of the EchoStar spectrum, AT&T’s 5G capacity has improved significantly. The buyout of Lumen’s fiber business has also expanded its fiber broadband footprint, enabling AT&T to expand its bundled product offerings. This could pose a threat to Verizon’s customer acquisition strategy through its convergence strategy. TMUS is also enhancing its 5G portfolio.

As of Dec. 31, 2025, the company had $19.05 billion in cash and cash equivalents with $139.53 billion of long-term debt compared with respective tallies of $4.19 billion and $121.38 billion in the year-ago period. As of 2025, Verizon’s current ratio is 0.91, while its cash ratio is 0.31. A current ratio lower than 1 suggests that the company may find it difficult to fulfill its short-term debt obligations.

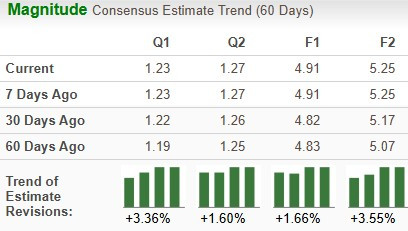

Estimate Revision Trend of VZ

VZ’s earnings estimates for 2026 and 2027 have increased over the past 60 days.

Image Source: Zacks Investment Research

Key Valuation Metric of VZ

From a valuation standpoint, VZ appears to be trading relatively cheaper compared to the industry but trading above its mean. Going by the price/earnings ratio, the company’s shares currently trade at 10.3, down from 13.31 for the industry.

Image Source: Zacks Investment Research

End Note

Verizon is gaining from solid subscriber momentum with a lower churn rate. Its convergence strategy is boosting brand loyalty, improving churn and driving customer retention. Focus on portfolio diversification and expansion into the emerging market of AI-enabled telematics for fleet management will likely bring long-term benefits. However, despite its effort to achieve portfolio diversification, stiff competition in its core domains, which are 5G and fiber broadband markets, continues to weigh on margins. High debt burden remains a major concern. With a Zacks Rank #3 (Hold), VZ appears to be treading in the middle of the road, and new investors could be better off if they trade with caution.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Benzinga’s Financial Flow: 25 Million Users, 50% Productivity, and the API Revenue Engine

Benzinga's Crypto Traffic Engine: Monetization Flow vs. Financial Reality

Is Figma, Inc. (FIG) A Good Stock To Buy?

México endurecerá reglas sobre minería del carbón tras accidente mortal