DE Gains 33% in a Year: What's the Right Strategy for Investors Now?

Deere & Company DE shares have gained 33.1% in a year, outperforming the Zacks Manufacturing - Farm Equipment industry’s 30.5% growth. In comparison, the broader Zacks Industrial Products sector has returned 31.1% and the S&P 500 has rallied 20.8%.

With this outperformance, investors may rush to add the stock to their portfolios. However, before doing so, it would be prudent to evaluate the stock’s growth prospects and associated risks to arrive at a well-informed investment choice.

Low Crop Prices Remain Challenging for DE

The U.S. Department of Agriculture forecasts a 0.7% year-over-year dip in net farm income to $153.4 billion in 2026. Total crop receipts are expected to inch up 1.2%, driven by higher corn and hay receipts. In inflation-adjusted terms, total crop receipts are predicted to fall 0.7%. Total production expenses are expected to increase 1%, with livestock/poultry purchases, feed and labor to be the three major expense categories.

Pesticide, fuel and oil expenses are likely to decline, while property taxes, fees and electricity costs are expected to rise. Direct government farm payments are anticipated to offer some relief, rising by $13.8 billion from that reported in 2025 to $44.3 billion in 2026. With the overall farm income expected to decline, this will weigh on the near-term demand for Deere’s equipment as well as other farm equipment manufacturers like AGCO Corporation AGCO and CNH Industrial CNH.

Tariffs Ail Deere’s Q1 Results Amid Higher Shipment Volumes

Deere returned to positive revenue growth in the fourth quarter of fiscal 2025, with the metric rising 11% on higher volumes after eight consecutive quarters of declines. This positive streak continued in the first quarter of 2026, with revenues increasing 17.5% from the prior-year quarter.

The Production & Precision Agriculture segment’s sales grew 3% from the prior-year quarter to $3.16 billion due to favorable foreign currency translation. The Small Agriculture & Turf segment’s sales were up 24% year over year at $2.17 billion, and Construction & Forestry sales were $2.67 billion in the first fiscal quarter, up 34% year over year.

However, earnings fell year-over-year as increased production costs and tariff-related pressures offset higher shipment volume gains. The company reported nine consecutive quarters of year-over-year decreases in net income.

Even though Deere increased its net income guidance for fiscal 2026 to $4.5-$5 billion, the range indicates a 6% year-over-year decrease at the midpoint. Net sales for Production & Precision Agriculture are expected to decrease 5-10% year over year. Sales of Small Agriculture & Turf are expected to rise 15%. Sales of Construction & Forestry are projected to increase 15%. The Financial Services segment’s net income is expected to be $840 million.

DE’s Long-term Growth Remains Solid

Despite near-term weakness, agricultural equipment demand will be supported by increased global demand for food, stemming from population growth. Also, the need to replace aging equipment will support DE’s top line. Peers AGCO Corp and CNH Industrial will also gain from these.

Over the long term, Deere is well-positioned for growth, underpinned by consistent investments in innovation and geographic expansion. Its focus on launching products with advanced technologies and features provides it with a competitive edge. The company remains focused on revolutionizing agriculture with technology in an effort to make farming automated, easy to use and more precise across the production process.

The company recently announced that it acquired the intellectual property and related assets for tree planting equipment from a Finland-based equipment manufacturing company, Risutec Oy. This deal will boost Deere’s silviculture strategy, along with providing customers involved in reforestation with solutions for sustainable forestry.

Deere also acquired a construction technology company, Tenna, in February 2026. Deere will scale and grow the business using Tenna's customer-focused mixed-fleet model. Deere will focus on scaling the business, leveraging Tenna's customer-focused mixed-fleet model.

Deere’s Recent Upward Estimate Revision

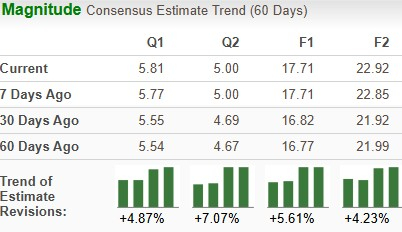

The consensus estimate for fiscal 2026 earnings suggests a year-over-year decline of 4.3%. However, the same for fiscal 2027 indicates year-over-year growth of 29.4%. The Zacks Consensus Estimate for 2026 sales implies 4.6% year-over-year growth. The same for fiscal 2027 suggests growth of 8.9%.

EPS estimates for 2026 and 2027 have moved north over the past 60 days.

DE Stock Trades at a Premium

Deere is currently trading at a forward 12-month price/earnings of 31.45X, a premium compared with the industry’s 29.99X. It is also higher than DE’s five-year median of 24.17X.

The DE stock also seems relatively more expensive than AGCO Corp and CNH Industrial, which are trading lower at 21.83X and 25.99X, respectively.

Final Take on Deere Stock

DE’s market leadership position, technologically advanced products and strong dealer network provide it with a competitive advantage to leverage the long-term demand prospects for both agricultural and construction equipment. However, the company has been facing challenges due to weak farmer spending amid low commodity prices.

Those who already own this Zacks Rank #3 (Hold) stock should stay invested to benefit from the long-term demand prospects for agricultural and construction equipment. However, new investors should wait for a more favorable time to accumulate the stock, considering expectations of low commodity prices, the impacts of tariffs and expensive valuation.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why the Integrity Viking Funds Deal Is a Win for Fidelity National

ETF Path To 401(k) Millionaire: How Index ETFs Can Power Retirement Wealth During Volatility

1 Healthcare Stock to Watch Closely This Week and 2 Encountering Obstacles

MSCI Acquires Compass Financial to Expand Multi-Asset Indexes