Rumble (NASDAQ:RUM) Reports Q4 CY2025 In Line With Expectations

Video sharing platform Rumble (NASDAQGM:RUM)

Is now the time to buy Rumble?

Rumble (RUM) Q4 CY2025 Highlights:

- Revenue: $27.07 million vs analyst estimates of $27.09 million (10.5% year-on-year decline, in line)

- EPS (GAAP): -$0.13 vs analyst expectations of -$0.10 (36.8% miss)

- Adjusted EBITDA: -$16.03 million (-59.2% margin, 19.8% year-on-year decline)

- Operating Margin: -131%, down from -80.1% in the same quarter last year

- Free Cash Flow was -$31.72 million compared to -$12.38 million in the same quarter last year

- Market Capitalization: $1.88 billion

Rumble's Chairman and CEO, Chris Pavlovski, commented, "Rumble has reached an inflection point. The investments we made throughout 2025, in platform stability, creator monetization, short-form video, and our sales infrastructure, are beginning to bear fruit. Rumble Shorts alone surpassed one million daily unique video views just weeks after launch, and Rumble Wallet gives creators a first-of-its-kind way to earn through Bitcoin, USA ₮, USD ₮, and Tether Gold. Our advertising business is anchored by a $100 million Tether commitment, and our pending acquisition of Northern Data will open an entirely new frontier in Cloud and GPU infrastructure. We are competing, winning on multiple fronts, and we are just getting started.”

Company Overview

Founded in 2013 as a champion for content creator rights and free expression, Rumble (NASDAQ:RUM) is a video sharing platform that positions itself as a free speech alternative to mainstream platforms, offering creators more favorable revenue-sharing opportunities.

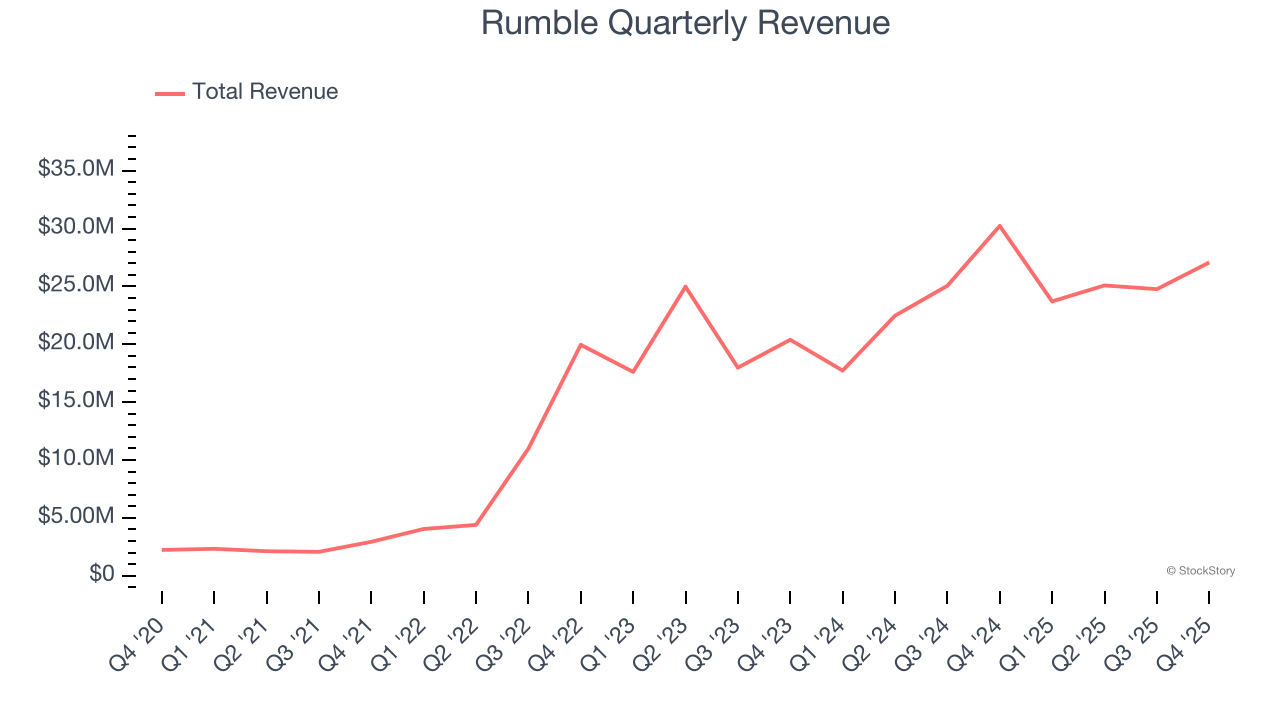

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $100.6 million in revenue over the past 12 months, Rumble is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

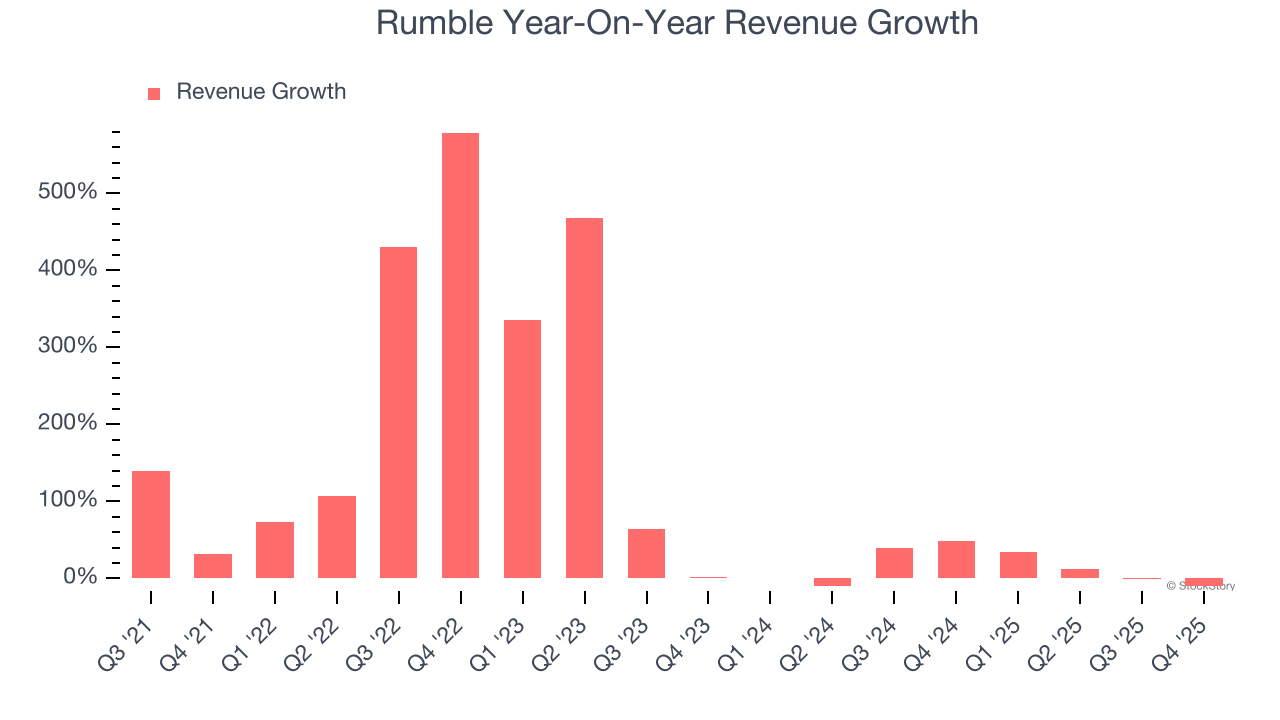

As you can see below, Rumble’s 75.6% annualized revenue growth over the last five years was incredible. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Rumble’s annualized revenue growth of 11.5% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Rumble reported a rather uninspiring 10.5% year-on-year revenue decline to $27.07 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 349% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will spur better top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar.

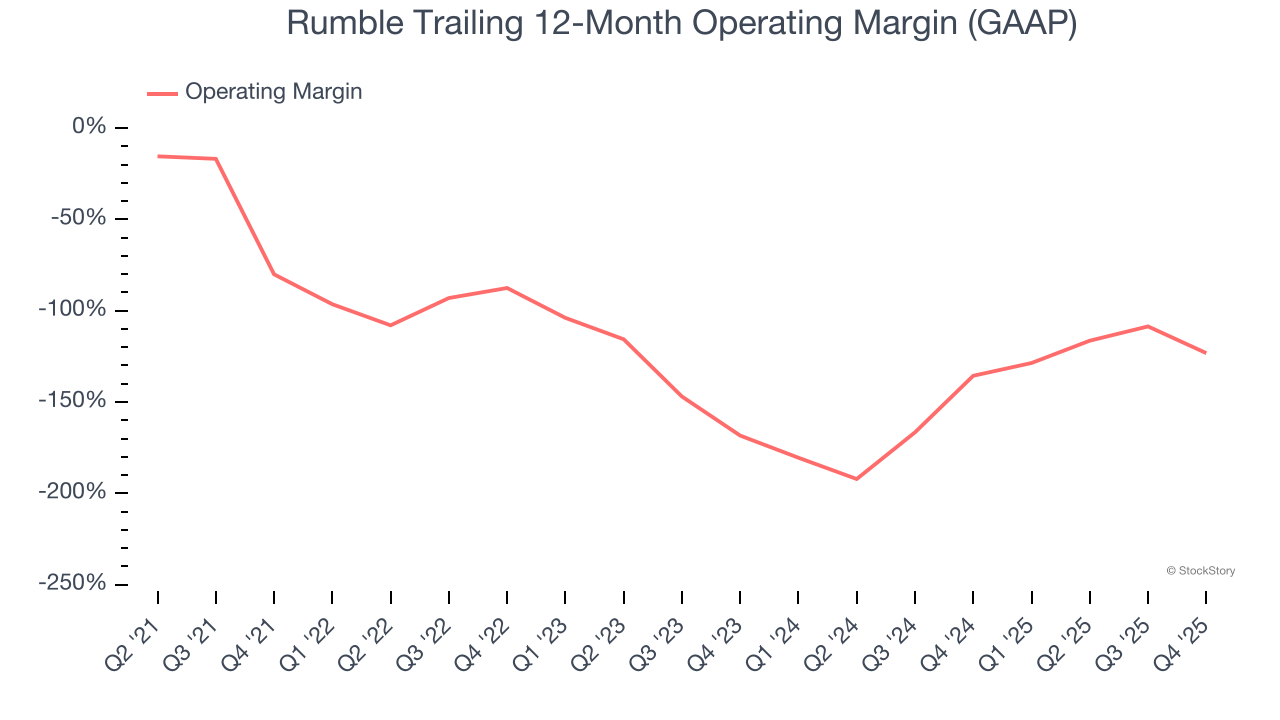

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Rumble’s high expenses have contributed to an average operating margin of negative 133% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out.

Analyzing the trend in its profitability, Rumble’s operating margin decreased by 43.1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Rumble’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

Rumble’s operating margin was negative 131% this quarter.

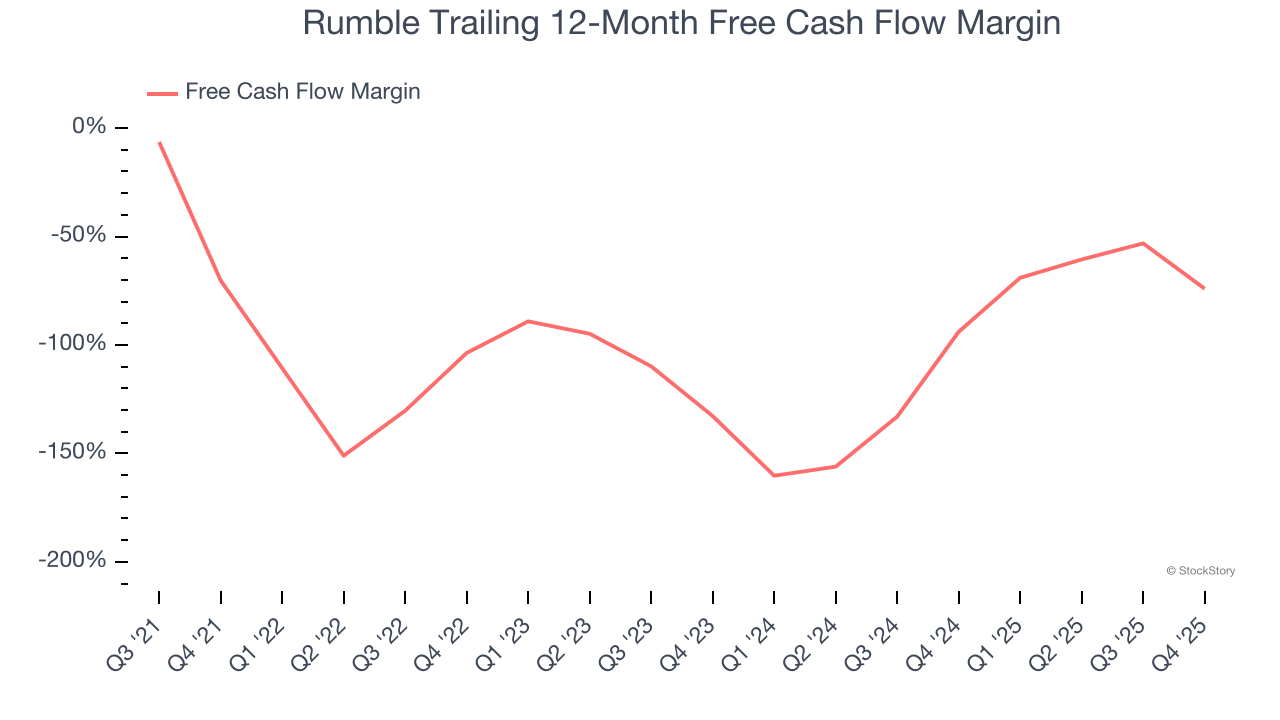

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Rumble’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 97.9%, meaning it lit $97.92 of cash on fire for every $100 in revenue.

Taking a step back, we can see that Rumble’s margin dropped by 3.8 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal it’s in the middle of an investment cycle.

Rumble burned through $31.72 million of cash in Q4, equivalent to a negative 117% margin. The company’s cash burn was similar to its $12.38 million of lost cash in the same quarter last year.

Key Takeaways from Rumble’s Q4 Results

We struggled to find many positives in these results. Overall, this was a softer quarter. The stock traded down 2.9% to $5.46 immediately after reporting.

Rumble didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

HIVE's Two-Pronged Approach: Constructing the Foundation for AI Infrastructure

Q4 Earnings Leaders: ScanSource (NASDAQ:SCSC) And Other IT Distribution & Solutions Shares

AEON Joins Zano to Expand $ZANO Utility for 50M+ Merchants in Markets

Thinkific Labs: A Strong Long-Term Investment Opportunity in the Learning Commerce Sector