Grid Dynamics (NASDAQ:GDYN) Posts Q4 CY2025 Sales In Line With Estimates

Digital transformation consultancy Grid Dynamics (NASDAQ:GDYN)

Is now the time to buy Grid Dynamics?

Grid Dynamics (GDYN) Q4 CY2025 Highlights:

- Revenue: $106.2 million vs analyst estimates of $105.9 million (5.9% year-on-year growth, in line)

- Adjusted EPS: $0.10 vs analyst estimates of $0.09 (in line)

- Adjusted EBITDA: $13.74 million vs analyst estimates of $13.24 million (12.9% margin, 3.8% beat)

- Revenue Guidance for Q1 CY2026 is $103.5 million at the midpoint, below analyst estimates of $106.6 million

- EBITDA guidance for Q1 CY2026 is $12.5 million at the midpoint, below analyst estimates of $13.68 million

- Operating Margin: 0.5%, in line with the same quarter last year

- Market Capitalization: $610.6 million

Company Overview

With engineering centers across the Americas, Europe, and India serving Fortune 1000 companies, Grid Dynamics (NASDAQ:GDYN) provides technology consulting, engineering, and analytics services to help large enterprises modernize their technology systems and business processes.

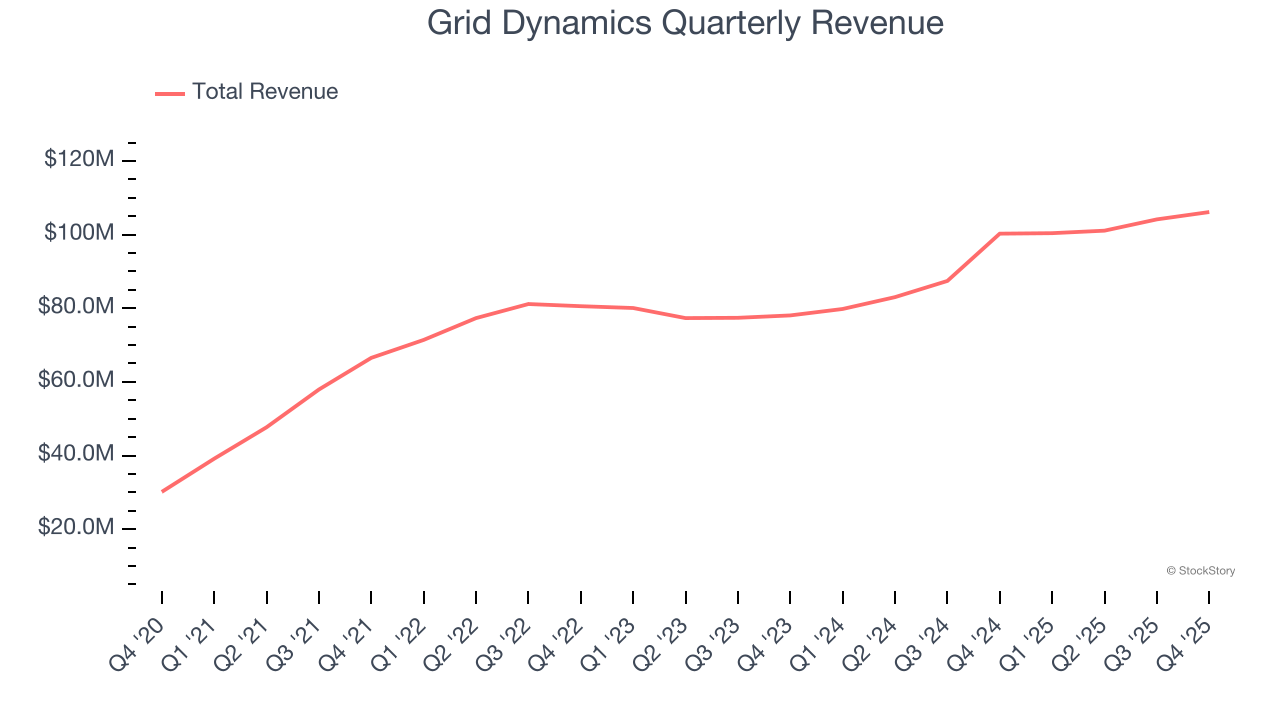

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $411.8 million in revenue over the past 12 months, Grid Dynamics is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

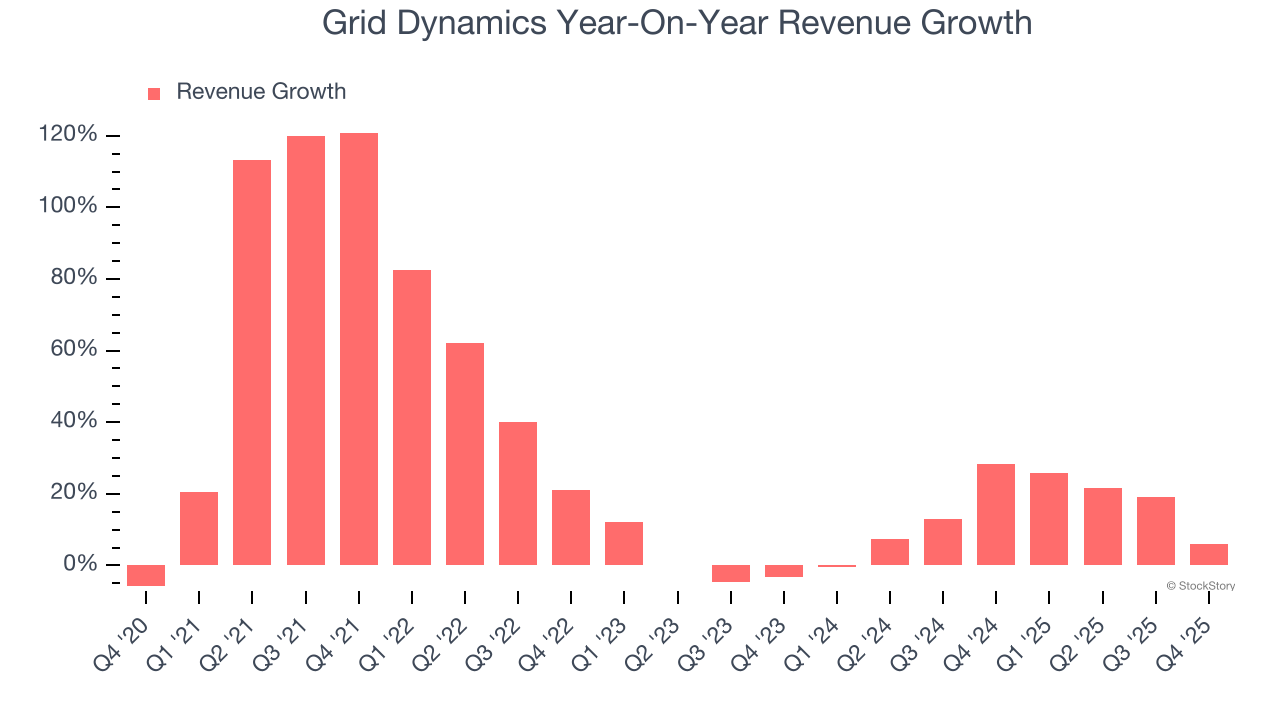

As you can see below, Grid Dynamics’s sales grew at an incredible 29.9% compounded annual growth rate over the last five years. This is an encouraging starting point for our analysis because it shows Grid Dynamics’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Grid Dynamics’s annualized revenue growth of 14.7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Grid Dynamics grew its revenue by 5.9% year on year, and its $106.2 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 3.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.1% over the next 12 months, a deceleration versus the last two years. Still, this projection is noteworthy and indicates the market is baking in success for its products and services.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar.

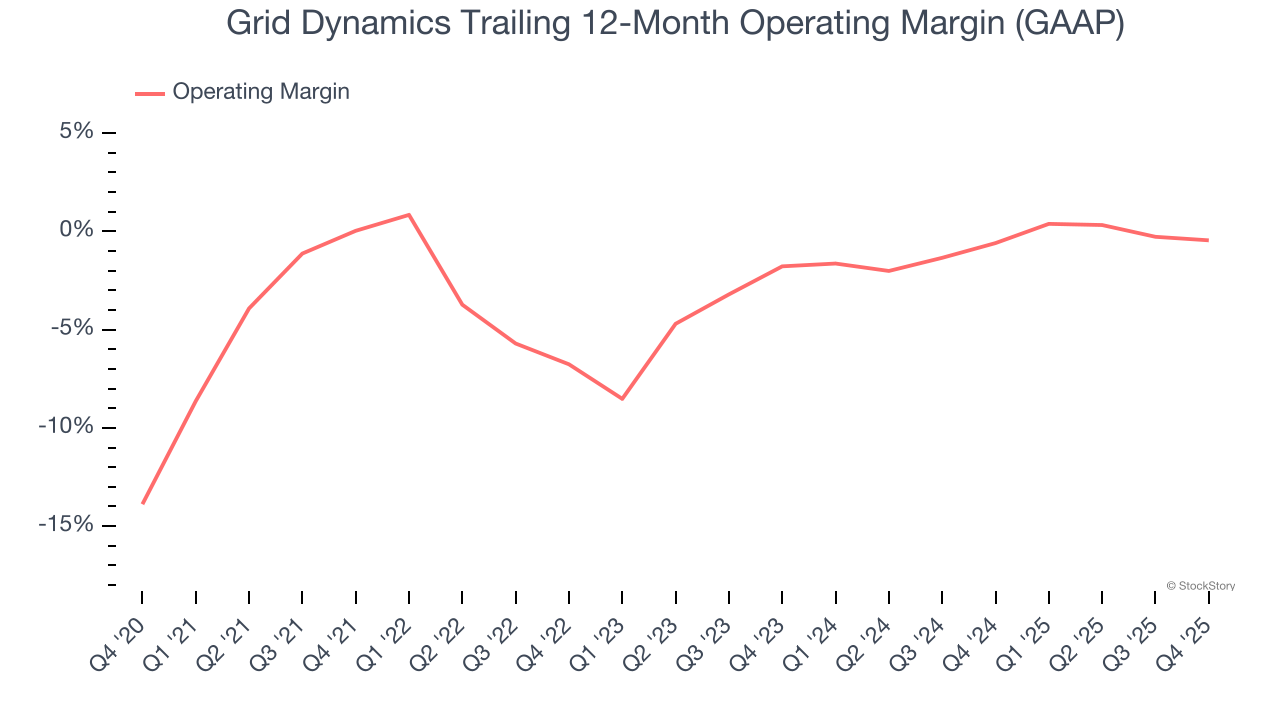

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Grid Dynamics’s operating margin has more or less stayed the same over the last 12 months , averaging negative 1.9% over the last five years. Unprofitable, high-growth companies warrant extra attention, especially if their profitability doesn’t improve. In Grid Dynamics’s case, it seems it’s deferring current profits by investing heavily to win market share.

Looking at the trend in its profitability, Grid Dynamics’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Grid Dynamics’s breakeven margin was 0.5%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

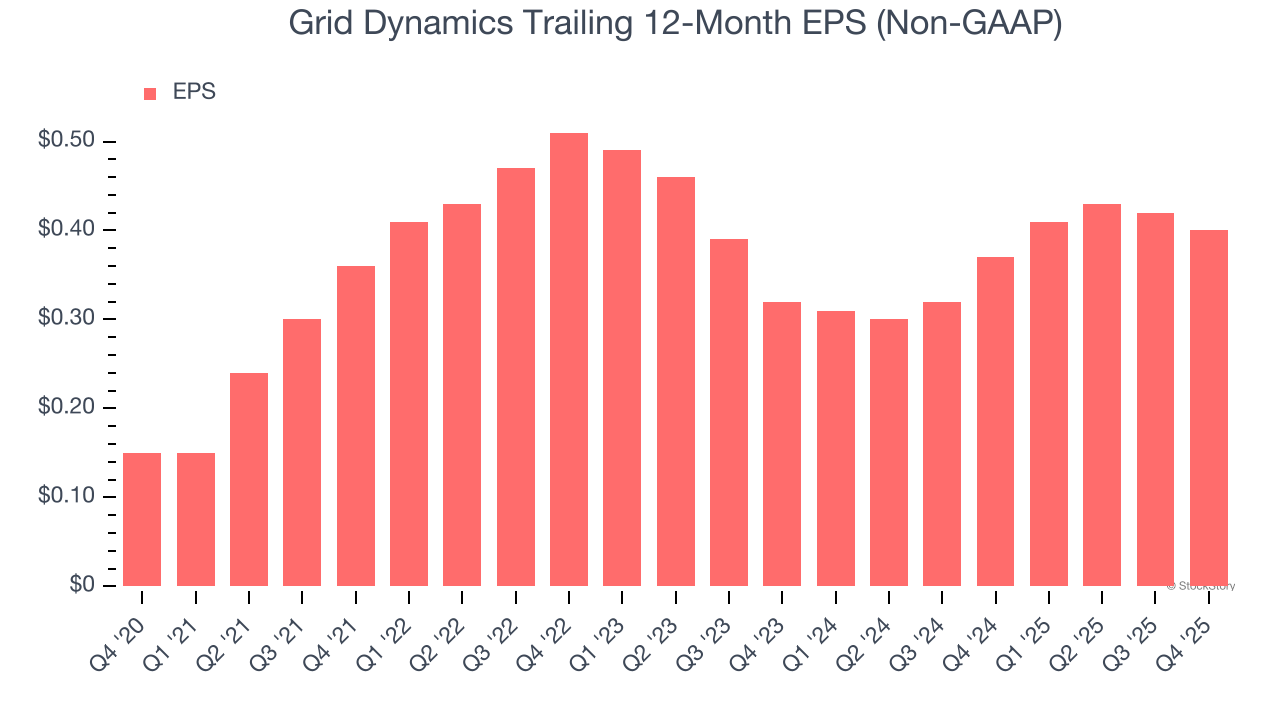

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Grid Dynamics’s EPS grew at an astounding 21.7% compounded annual growth rate over the last five years. Despite its operating margin improvement during that time, this performance was lower than its 29.9% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Grid Dynamics, its two-year annual EPS growth of 11.8% was lower than its five-year trend. This wasn’t great, but at least the company was successful in other measures of financial health.

In Q4, Grid Dynamics reported adjusted EPS of $0.10, down from $0.12 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 9.4%. Over the next 12 months, Wall Street expects Grid Dynamics’s full-year EPS of $0.40 to grow 17.5%.

Key Takeaways from Grid Dynamics’s Q4 Results

It was encouraging to see Grid Dynamics meet analysts’ EPS expectations this quarter. On the other hand, its revenue guidance for next quarter missed and its full-year revenue guidance was in line with Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.6% to $6.96 immediately after reporting.

Grid Dynamics’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The world’s biggest sovereign gold buyer might start selling to double defense budget

Top Analyst Reports for Exxon Mobil, Palantir & AstraZeneca