Costco's Q2 beat reinforces its membership-fee machine

Costco just did the most Costco thing possible. It reported another quarter of very impressive, very steady growth — and did it without breaking the “no surprises” brand promise that has turned the warehouse club into a market-cap religion. Amid all the market chaos, the warehouse club quietly keeps doing what it does best: selling a lot of stuff, moving a lot of people through its doors, and letting membership fees turn madness into margin.

For Q2 FY 2026, Costco said net sales rose 9.1% to $68.24 billion, while net income climbed to $2.04 billion, or $4.58 per diluted share. Total revenue, which adds in the part investors actually tattoo over their hearts — membership fees — came in at $69.6 billion. Membership fees themselves were $1.36 billion, up about 14% from a year ago, and operating income grew to $2.61 billion. That’s a touch better than the drumbeat heading into today, when analysts were broadly looking for $4.55 EPS on $69.3 billion in revenue, with same-store sales (excluding gas) up 5.88%.

Costco keeps selling the hot dog combo and the 40-pack of paper towels, but the model keeps behaving like a subscription business.

Comparable sales for the quarter were up 7.4% companywide, with “digitally-enabled” sales up 22.6%, a reminder that Costco’s e-commerce operation is a meaningful second register. Strip out gasoline and foreign exchange, and comps were still up 6.7% (beating the Street’s 5.88% estimate), with digitally-enabled up 21.7%. The U.S. did what the U.S. usually does for Costco: steady, mid-single-digit growth. Canada and “Other International” did what they’ve been doing lately: reminding everyone that Costco’s brand travels.

Costco also bundled in its February sales update. For the four-week period ending March 1, net sales rose 9.5% to $21.69 billion, with total company comps up 7.9% (7% adjusted). That “Other International” category was a headline-grabber at 17.9% in February — though Costco flagged that the later timing of Lunar and Chinese New Year this year (19 days later) boosted that region by about four percentage points and total company sales by about half a point.

Under the hood, the company is still doing the same math it always does: Protect the value proposition, let volume do the heavy lifting, and let membership fees fatten the margins. Over the first 24 weeks of fiscal 2026, membership fees totaled $2.68 billion, total revenue hit $136.9 billion, and operating cash flow came in at $7.68 billion. Costco also kept returning cash the Costco way, reporting $419 million in share repurchases and $1.15 billion in dividends paid over that period.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

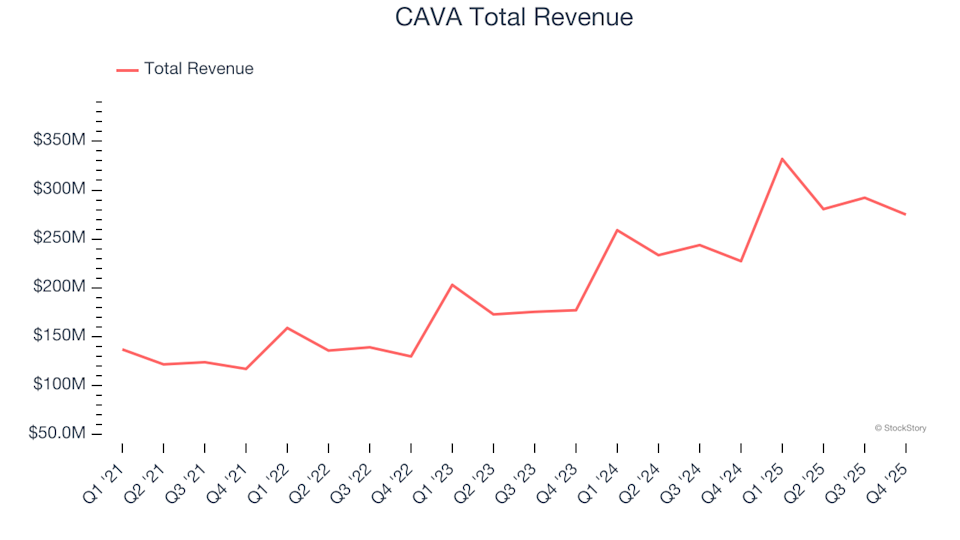

Q4 Results Overview: CAVA (NYSE:CAVA) Outperforms Contemporary Fast Food Chains

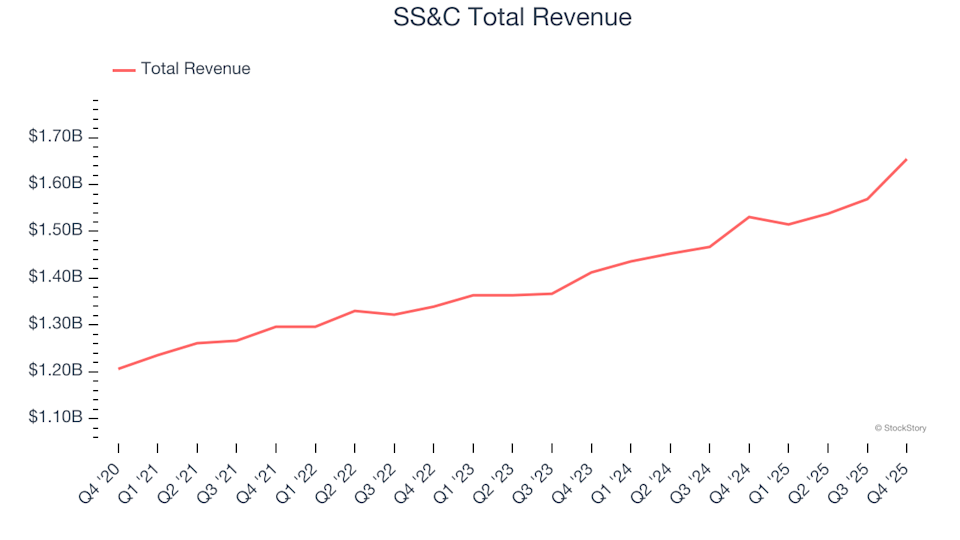

Q4 Financial Results Overview: SS&C (NASDAQ:SSNC) Compared to Other Data & Business Process Services Companies

Gold holds losses as strong dollar outweighs haven demand; set for weekly drop

Sophron's $7 Million PECO Sale: The Real Insights from Savvy Investors