Palantir Stock Slides 0.34 Amid Mixed Analysts and Earnings Surge as 11th-Ranked Volume Sparks Volatility

Market Snapshot

On March 5, 2026, PalantirPLTR-- (PLTR) closed with a 0.34% decline, trading at a volume of $7.67 billion, which ranked it 11th in market activity. Despite the modest drop, the stock remains within its 52-week range of $66.12 to $207.52, with the 50-day and 200-day moving averages at $156.94 and $169.14, respectively. The decline followed mixed analyst activity and broader market dynamics, though the stock had previously surged 2.94% in after-hours trading following strong Q4 2025 earnings results.

Key Drivers

Palantir’s recent earnings report underscored robust financial performance, with Q4 2025 revenue reaching $1.407 billion, a 70% year-over-year increase, and EPS of $0.25, surpassing estimates by 8.7%. The U.S. commercial segment drove much of this growth, expanding 137% YoY, while total contract value bookings hit $4.3 billion and net dollar retention reached 139%. These figures highlight the company’s ability to scale organically, a key differentiator emphasized by management. However, the stock’s slight decline suggests investors may be recalibrating expectations amid broader market volatility or profit-taking after the post-earnings rally.

Analyst sentiment has been polarized, reflecting both optimism and caution. UBS Group upgraded Palantir to “buy” with a reduced price target of $150, while Freedom Capital elevated it to “strong-buy” from “strong-sell.” Conversely, Weiss Ratings cut its rating to “hold” and Deutsche Bank maintained a “hold” with a $200 price target. The mixed guidance complicates investor sentiment, as upgrades highlight confidence in Palantir’s AI-driven enterprise software platform but downgrades and stagnant ratings signal lingering skepticism about valuation sustainability.

Management’s forward-looking guidance further contextualizes the stock’s trajectory. Palantir projects 2026 revenue between $7.182–$7.198 billion, reflecting 61% growth, with U.S. commercial revenue expected to exceed $3.144 billion. This aggressive target aligns with the company’s strategic focus on AI integration, which executives position as a core competitive advantage. The emphasis on organic growth, rather than acquisitions, reinforces long-term confidence but may test market patience if short-term execution falters.

The stock’s technical indicators and earnings momentum suggest a resilient but cautious outlook. While the 52-week high of $207.52 remains a psychological barrier, the current price near the 50-day moving average ($156.94) indicates support. The company’s 36.31% net margin and 23.81% return on equity, coupled with consistent revenue outperformance, underscore operational efficiency. Yet, the recent 0.34% drop reflects the broader tech sector’s sensitivity to interest rate uncertainty and macroeconomic risks, despite Palantir’s standalone fundamentals.

In summary, Palantir’s performance is driven by a blend of strong earnings, strategic differentiation in AI, and divergent analyst opinions. While the company’s financials and growth projections are compelling, market participants remain divided on valuation and risk-adjusted returns. Investors will likely monitor upcoming analyst upgrades, execution on 2026 guidance, and broader sector trends to determine the stock’s next directional move.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bond dealers analyze employment figures to assess the Federal Reserve’s direction as oil prices surge

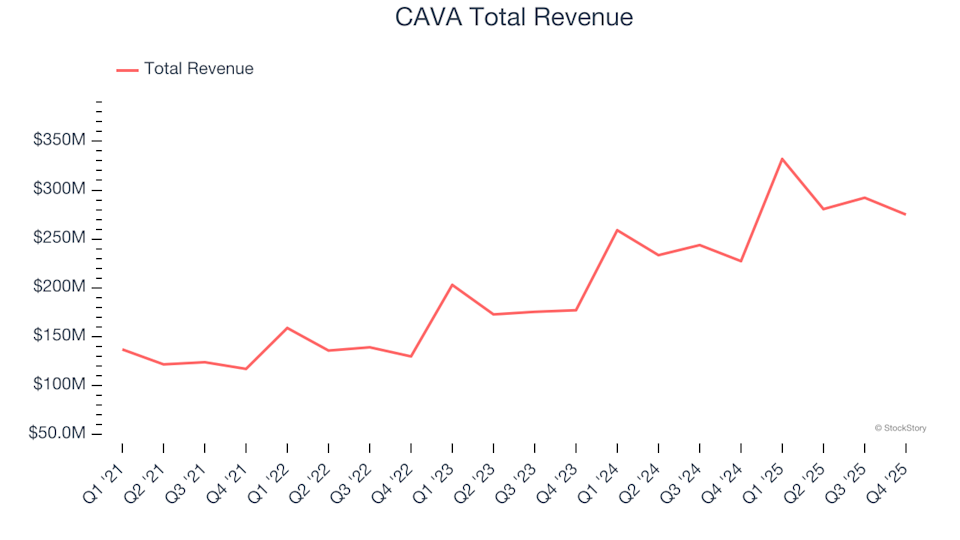

Q4 Results Overview: CAVA (NYSE:CAVA) Outperforms Contemporary Fast Food Chains

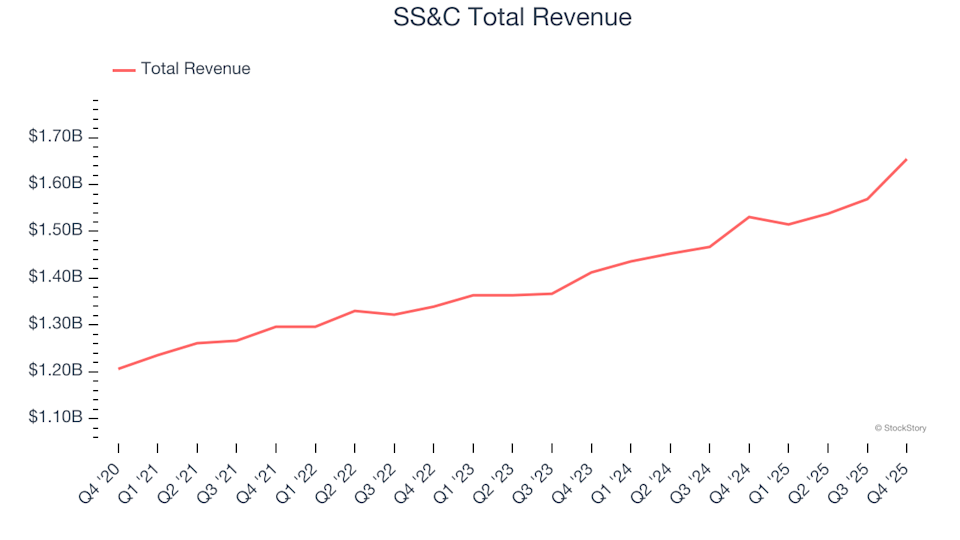

Q4 Financial Results Overview: SS&C (NASDAQ:SSNC) Compared to Other Data & Business Process Services Companies