Why the Suspension of LNG in Qatar Is Unlikely to Cause a Prolonged Surge in Global Prices

Global Gas Market Faces Temporary Turbulence Amid Middle East Tensions

Natural gas prices have experienced significant volatility following QatarEnergy’s suspension of LNG production and the closure of the Strait of Hormuz due to intensifying unrest in the Middle East. Although Europe’s Title Transfer Facility (TTF) saw prices soar by over 52% on March 2, Rystad Energy anticipates that this supply disruption will have only a short-lived effect on the broader global gas and LNG markets.

This assessment is grounded in the belief that the interruption will be brief and that the affected volumes can be managed effectively.

“The halt in Qatari LNG output and the closure of the Strait of Hormuz have already led to a noticeable tightening in global LNG supply, as recent price trends indicate.

The actual loss in supply will depend on the extent of any infrastructure damage—still under evaluation—and how long the Strait remains inaccessible to shipping.

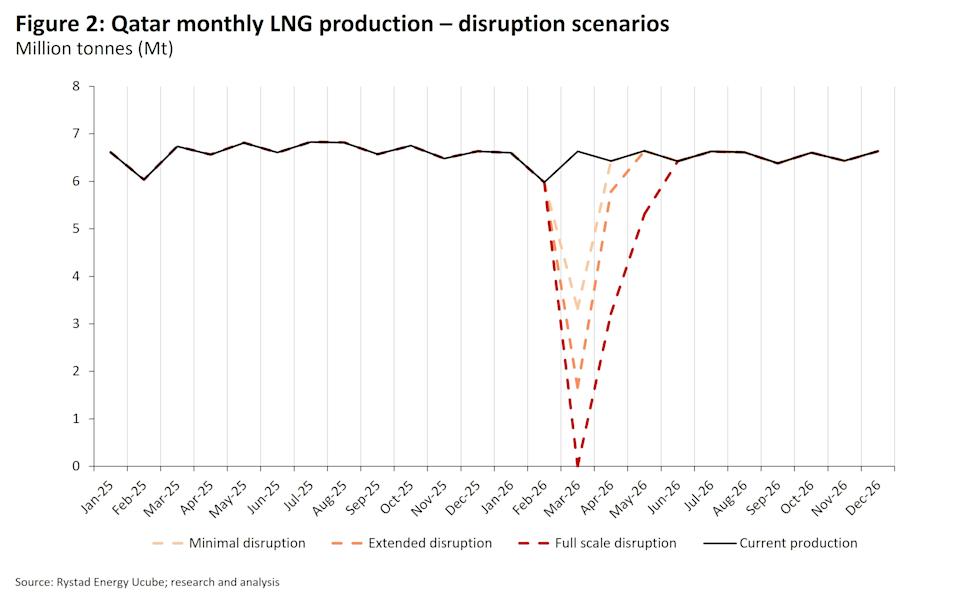

If the disruption is minimal and hostilities ease quickly, resulting in a 15-day production pause, output for 2026 could decrease by about 4.3%, or roughly 3.3 million tonnes (Mt).

Should the situation persist, the supply shortfall could reach 5.6 Mt, and a complete shutdown lasting four to five weeks could mean a loss of around 11.2 Mt for the entire year 2026.

Given the importance of LNG exports to Qatar’s economy and the global market, we expect operations to resume within a matter of weeks rather than months.”

In a worst-case scenario, other producers could step in to supply up to 15 Mt of additional LNG, while the return of Russian LNG could add another 18 Mt to the market.

The countries most impacted by these developments are primarily developing economies that are highly sensitive to price changes. These nations are more likely to switch to alternative fuels, such as thermal coal, rather than engage in aggressive bidding for LNG cargoes.

QatarEnergy Suspends LNG Production

Following a drone attack on its Ras Laffan gas facilities on March 2, QatarEnergy halted all LNG production, coinciding with the suspension of maritime traffic through the Strait of Hormuz. This indefinite pause affects Qatar’s entire liquefaction capacity of 77 million tonnes per year. While these events cast uncertainty over Qatar’s medium-term prospects, the country is still on track to nearly double its LNG capacity to 142 Mtpa within the next decade. This expansion will be achieved through three major projects: North Field East (32 Mtpa), North Field South (16 Mtpa), and North Field West (16 Mtpa). The first phase of North Field East is expected to come online in the third quarter of 2026, provided there are no further infrastructure setbacks or shipping issues. North Field South aims to start production in late 2028 or early 2029, and North Field West recently reached a final investment decision.

Potential for Russian LNG to Re-enter the Market

At the start of the year, the LNG market was poised for growth. Before the conflict, Rystad Energy projected that existing facilities would add 13.9 Mt and new or restarted plants, such as Darwin LNG, would contribute an additional 7.6 Mt compared to 2025. Higher-than-expected prices could prompt increased output from West Africa and the US, though Egypt’s exports are constrained by the halt of Israeli pipeline gas.

If Qatar’s infrastructure suffers further damage or if Iran blocks commercial shipping through the Strait, the global LNG supply could face even greater deficits in 2026. In such a scenario, discussions about reintroducing Russian LNG may arise. Lifting sanctions could allow up to 5.3 Mt from existing Russian sources and another 12.8 Mt from Arctic LNG 2 to re-enter the market. However, this would require the complete removal of sanctions and a willingness from European buyers to purchase Russian LNG, which would complicate US LNG expansion plans and is therefore considered highly unlikely.

Why a Price Surge Is Unlikely

The ongoing US-Israel operations in the Middle East are expected to tighten global gas supplies in 2026. However, these events are unfolding in a market with relatively balanced supply and growing trade flows. The disruption mainly affects a different set of countries, leading to unique demand responses.

The greatest impact will likely be felt by price-sensitive buyers in South Asia, such as Bangladesh and Pakistan, rather than by premium markets that might otherwise compete for cargoes. While reducing demand may seem like the most straightforward solution, natural gas remains a crucial part of these countries’ energy mix. As a result, a combination of demand reduction and, where possible, switching to other fuels is expected. Nevertheless, higher prices for crude oil and related products could limit the extent of this fuel switching.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Simon Property's $5B Credit Refinance Can't Stop 1.02% Decline Despite $300M Volume Surge to 465th Rank

Corteva Shares Tumble 1.81% as Earnings Misses and Execution Risks Sink 479th Ranked Stock

Wabtec (WAB): Should You Buy, Sell, or Hold After Q4 Results?