Cloudflare Stock Rises 3.45% on $730M Trading Volume Surge Ranking 199th in Daily Trading Activity

Market Snapshot

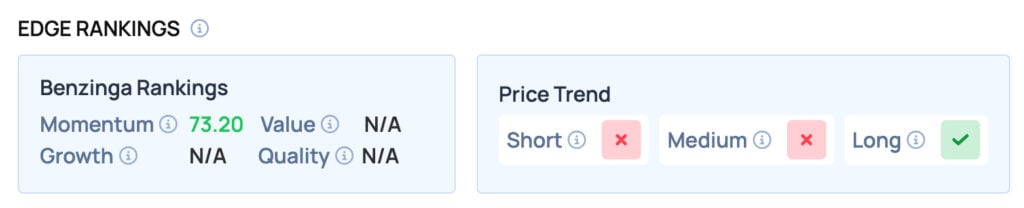

On March 5, 2026, CloudflareNET+3.45% (NET) saw a 3.45% increase in its stock price, driven by a 44.11% surge in trading volume to $0.73 billion, ranking it 199th in daily trading activity. This marked a significant rebound in liquidity compared to the prior day’s performance. The stock’s positive momentum aligns with broader market attention on its recent earnings results and strategic positioning in the AI infrastructure sector.

Key Drivers

Cloudflare’s recent earnings report revealed a critical inflection point in its financial trajectory. For the quarter ending March 2025, the company reported a net income of -$1.29 million but achieved a positive EBITDA of $4.108 million, reflecting a 113.89% year-over-year growth. This marked a reversal from consecutive quarters of negative EBITDA, including a -$29.583 million loss in June 2025. The EBITDA margin improved to 0.73%, up from -5.77% in the prior quarter, signaling improved operational efficiency. Analysts attributed this turnaround to disciplined cost management and higher gross margins, which rose to 73.97% in the March 2025 quarter, driven by strong revenue growth of 9.7% year-over-year.

A second key factor was the company’s robust revenue performance and customer expansion. Cloudflare’s quarterly revenue reached $562.027 million, with a 34% year-over-year increase in Q4 2025 revenue to $614.5 million. The company also reported a 23% rise in high-value customers (those spending over $100,000 annually), now totaling 4,298. This growth underscores Cloudflare’s expanding market share in cloud infrastructure and its ability to capitalize on the AI-driven demand for scalable internet services. CEO Matthew Prince emphasized the company’s role as a platform for AI agents, positioning Cloudflare as a critical enabler of next-generation internet infrastructure.

Third, analyst sentiment played a pivotal role in shaping investor expectations. Recent reports included mixed but largely optimistic price targets, with Wells Fargo raising its target to $270 and Royal Bank of Canada to $240, both with “outperform” ratings. However, Guggenheim’s “sell” rating at $140 highlighted lingering concerns about profitability. Despite a negative P/E ratio (-641.56) and a beta of 1.98, reflecting high volatility, the stock’s $65.17 billion market cap indicates strong institutional confidence in its long-term growth potential.

Finally, Cloudflare’s 2026 guidance reinforced its strategic direction. The company projected revenue of $2.785–$2.795 billion for the year, with operating income of $378–$382 million, and Q1 2026 revenue of $620–$621 million. These forecasts, coupled with a 14.6% operating margin in Q4 2025, suggest a path toward sustained profitability. Free cash flow of $99.4 million (16% of revenue) further supports capital allocation flexibility, enhancing investor confidence in the company’s ability to reinvest in AI and developer platforms.

Together, these factors—operational improvements, revenue growth, strategic AI positioning, and analyst activity—created a compelling narrative for Cloudflare’s stock, driving its recent performance and setting the stage for continued market scrutiny in the coming quarters.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

UBS Cuts Harley-Davidson (HOG) Price Target; Morgan Stanley Sees Uneven Consumer Environment

UBS Cuts Harley-Davidson (HOG) Price Target; Morgan Stanley Sees Uneven Consumer Environment

Nick Szabo Warns Inscriptions Expose Node Operators to Legal Liability

Ford's Recall Woes Continue As Over 600,000 SUVs Recalled Over Windshield Wiper Issue