Alcoa Earnings Beat Can't Stop Shares from Sliding 1.9% as 328th Ranked Volume Reflects Investor Caution Over 2026 Outlook

Market Snapshot

Alcoa (AA) closed March 5, 2026, down 1.90%, with a trading volume of $0.45 billion, representing a 49.21% decline from the previous day’s volume. This marked the 328th highest trading volume of the day, indicating subdued investor activity. The stock’s performance followed a mixed earnings report for Q4 2025, where adjusted earnings per share (EPS) of $1.26 exceeded the $0.93 forecast, and revenue of $3.4 billion surpassed the projected $3.28 billion. Despite the earnings beat, the stock fell 2.60% after hours, reflecting investor caution ahead of the 2026 outlook.

Key Drivers

Alcoa’s Q4 2025 results highlighted sequential revenue growth of 15% and a 16.4% return on equity (ROE), alongside $594 million in free cash flow for 2025. However, the stock’s post-earnings decline suggests skepticism about the company’s 2026 guidance. Management projected alumina production of 9.7–9.9 million tons and aluminum production of 2.4–2.6 million tons, with $750 million allocated for capital expenditures. These plans, while ambitious, were tempered by challenges such as alumina price pressures and global supply constraints, as noted by CEO William Oplinger.

The earnings report also revealed a significant improvement in profitability metrics. For Q4 2025, Alcoa’s operating income grew 115.8% year-over-year to $574 million, with a 16.5% EBIT margin. However, the 2026 guidance included projected EBITDA losses of $75–100 million at the San Ciprián mine, despite management’s target of cash neutrality by 2027. This discrepancy between strong recent performance and future risks may have weighed on investor sentiment.

Alcoa’s balance sheet showed $1.6 billion in cash as of year-end 2025, supporting its focus on low-cost mining and refining. Yet, the company’s capital expenditure plans for 2026—$750 million—signal a commitment to expansion that could strain near-term liquidity. The stock’s technical indicators, including a 52-week range of $21.53–$66.95 and a current price near the lower end of the 50-day moving average, suggest volatility. Analysts’ mixed signals, such as a 35.5% EPS surprise in Q4 2025 but a 41.5% revenue decline in Q3 2025, further highlight inconsistent performance.

The broader market context also influenced Alcoa’s stock. While the company’s 2025 free cash flow generation and improved ROE were positives, the aluminum sector faces headwinds from global supply chain bottlenecks and decelerating demand growth. For instance, Q3 2025 revenue fell 10.4% year-over-year to $3.02 billion, despite a 166.7% EPS beat, underscoring the volatility of commodity prices. These dynamics, coupled with Alcoa’s reliance on high-cost production at San Ciprián, may limit its ability to sustain margins in 2026.

CEO Oplinger’s emphasis on “robust market fundamentals” contrasts with the projected EBITDA losses, reflecting a strategic bet on long-term value creation amid short-term challenges. The company’s dividend policy, with a consistent $0.10 per share payout, remains stable, but investors may be prioritizing growth metrics over yield given the stock’s 1.9% decline. Overall, Alcoa’s performance reflects a tug-of-war between operational improvements and sector-specific risks, with the stock’s trajectory likely hinging on execution of its 2026 capex and production targets.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

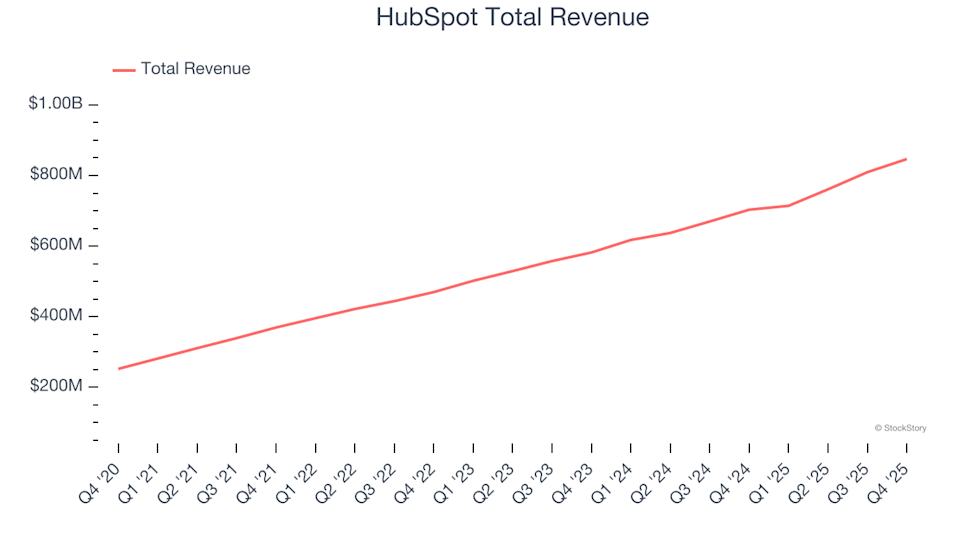

Sales Software Stocks Q4 Results: HubSpot (NYSE:HUBS) Delivers Strong Performance Across the Board

uniQure's Huntington's Therapy: A Regulatory Reset and the Price of Priced-In Hype

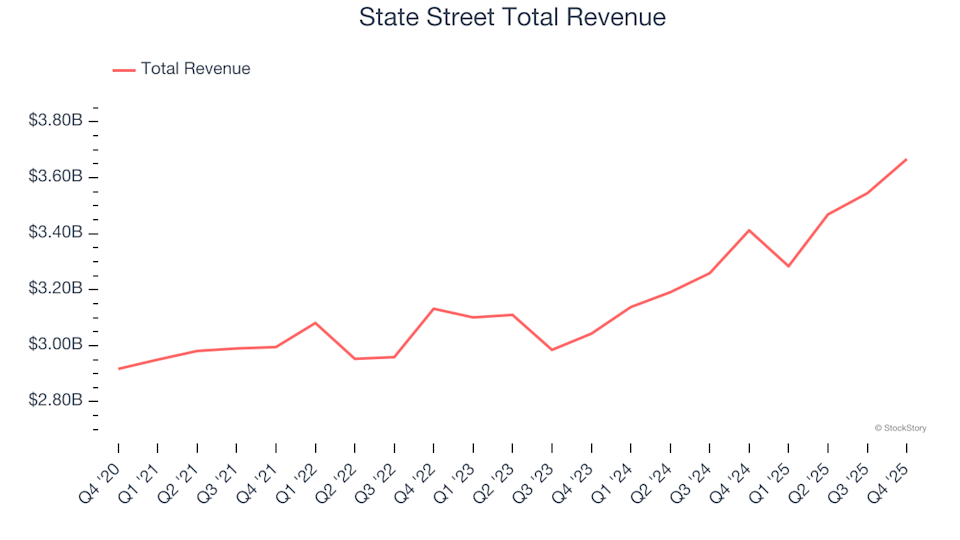

Custody Bank Stocks Q4 Performance: Comparing State Street (NYSE:STT)