CNY: Trading Volume Surge and Two-way Fluctuation

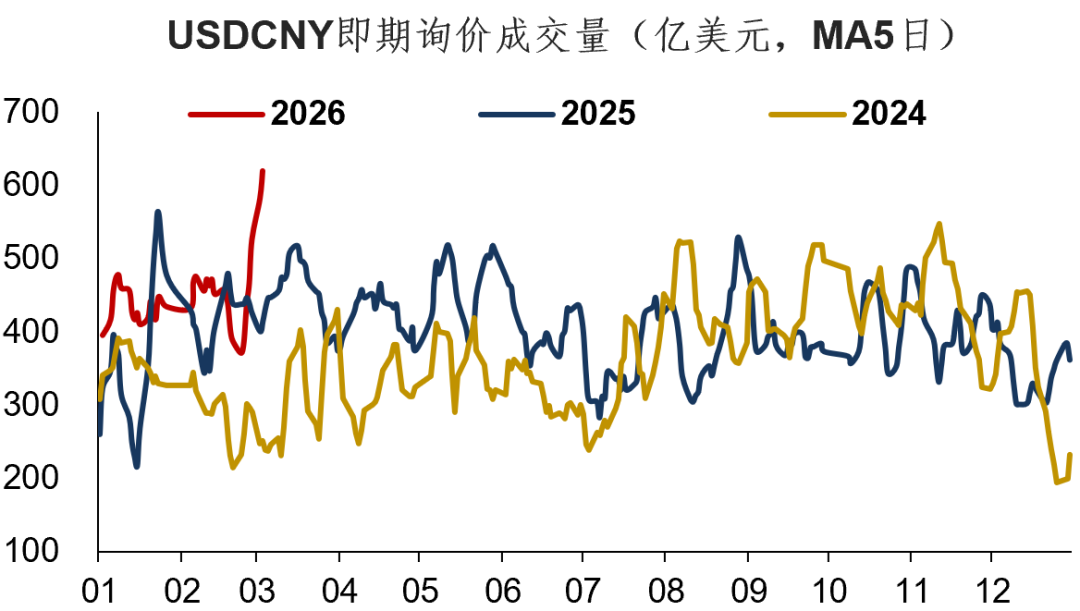

Recently, a new phenomenon in the RMB exchange rate market is the obvious increase in trading volume. Since February 25, USDCNY spot trading volume has exceeded $50 billion for six consecutive trading days, especially on March 4, when the spot trading volume reached $71.4 billion, setting a historic high.

Why is there an increase in market trading volume? In addition to changes in regulatory factors (such as the reduction of the forward FX purchase risk reserve ratio), another important reason is that the market has started to fluctuate in both directions. It's important to note that high levels of market consensus usually make it difficult for trading volume to increase; trading volume only increases when there are market divergences and two-way fluctuations…

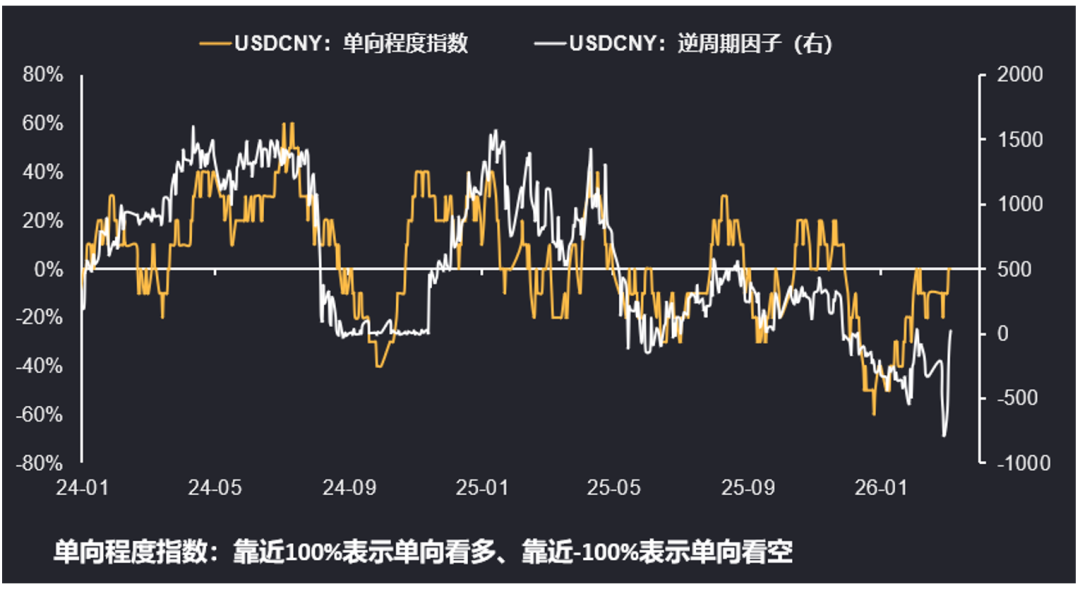

Over the past year, due to the persistent low volatility of USDCNY, many traders have developed the illusion that policies are intentionally smoothing out volatility. In reality, policy always refers to "preventing one-way fluctuations," not "preventing fluctuations"—there is a clear distinction between the two. As shown in the chart above, when the one-way degree of USDCNY is high (either purely bullish or bearish), the absolute value of the counter-cyclical factor tends to be larger.

When the market is in a state of two-way fluctuation (one-way degree close to zero), the counter-cyclical factor also tends to converge. The current forex market is in such a state, with both Spot and Fixing around 6.90, the counter-cyclical factor has basically withdrawn, and market two-way volatility has increased.

So, how should trading be conducted in such a two-way fluctuating environment? In fact, it’s quite challenging, because the markets are greatly affected by the Middle East and crude oil—a swing between risk-on and risk-off—and overall, it’s a dollar “siphoning” environment against non-dollar currencies (see "Petrodollars Start Siphoning"). Looking further ahead, I believe the RMB exchange rate market will see three new features this year:

First, trading volume will surge. Because imports, exports, and cross-border fund flows are growing at 5%-10% annually, and if the FX settlement rate returns to neutral, an increase in trading volume is almost inevitable. In addition, a recovery in forward FX purchase demand will also contribute to trading volume.

Second, two-way volatility will intensify. The rise in market trading capacity naturally provides fertile ground for two-way fluctuations. And a certain degree of two-way fluctuation (rather than one-way expectations) is also desirable from a policy perspective. Of course, in this two-way fluctuating process, forward FX settlement, forward FX purchases, and options hedging will all present opportunities.

Third, the market will be more like "taking cues from commodities when trading FX". In fact, this state has been quite apparent in Q1: when oil prices are high, the dollar "siphons" non-US currencies, G7 currencies compete in weakness, and the dollar strengthens; when base metals and precious metals rise, commodity and emerging market currencies strengthen, and the CNY will also benefit indirectly... Essentially, this remains a market environment dominated by geopolitics and commodities, with equities, bonds, and FX all revolving around commodities.

To summarize today's insights:

1. Recently, trading volume in the RMB exchange rate market has begun to increase. In addition to changes in regulatory factors, another important reason is the start of two-way market volatility.

2. Over the past year, USDCNY’s continued low volatility has created the illusion of “low volatility” for many traders. In reality, policy always refers to “preventing one-way fluctuations” rather than “preventing fluctuations” itself, and there is a clear difference between the two.

3. In the short term, the forex market environment is dominated by petrodollars “siphoning” other currencies. Looking further out, the RMB exchange rate market may show three characteristics this year: increased trading volume, intensified two-way volatility, and “looking at commodities when trading FX.”

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

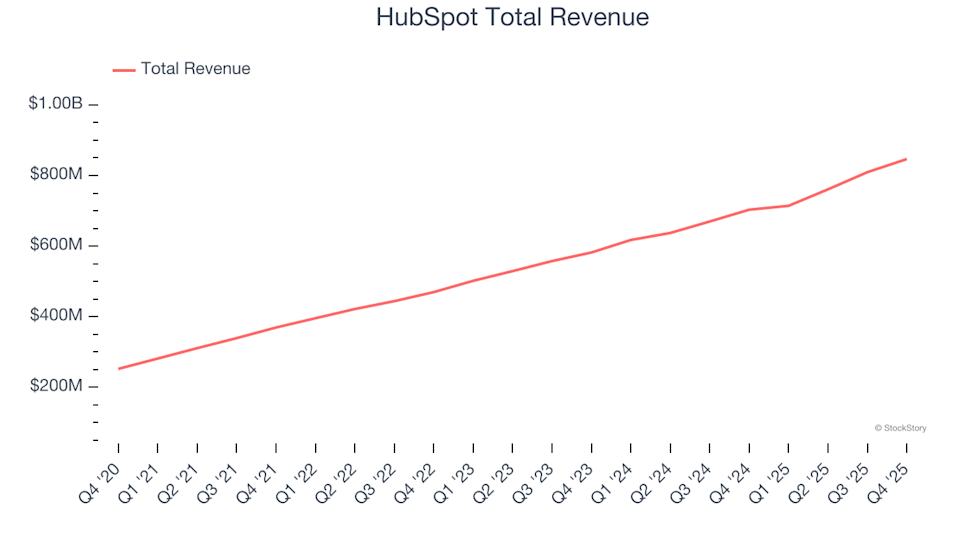

Sales Software Stocks Q4 Results: HubSpot (NYSE:HUBS) Delivers Strong Performance Across the Board

uniQure's Huntington's Therapy: A Regulatory Reset and the Price of Priced-In Hype

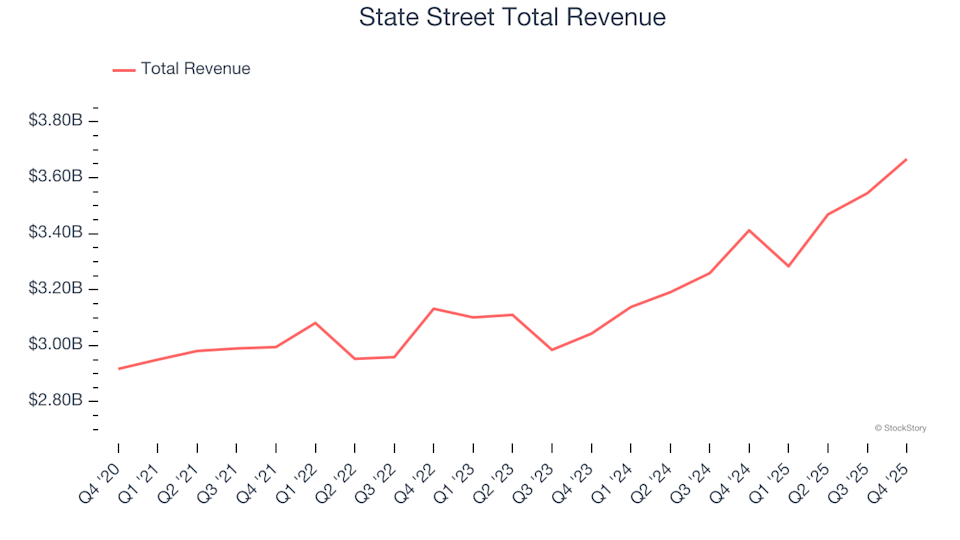

Custody Bank Stocks Q4 Performance: Comparing State Street (NYSE:STT)