EQT's Modest Gains Backed by Analyst Optimism Navigating 304th Volume Rank and Attractive PEG Ratio

Market Snapshot

EQT Corporation’s stock (NYSE: EQT) rose 0.59% on March 5, closing at $61.45, with a trading volume of $0.47 billion, ranking 304th in market activity. The stock’s performance was modest despite a 24.8% year-over-year revenue increase and a $0.90 quarterly earnings per share (EPS), surpassing the $0.76 consensus estimate. EQT’s market capitalization stood at $38.4 billion, with a P/E ratio of 18.57 and a PEG ratio of 0.41, reflecting relatively low valuation pressures compared to peers.

Key Drivers

The stock’s slight gain was influenced by a mix of analyst activity, earnings momentum, and sector dynamics. UBS Group lowered its price target to $75 (from $76) while maintaining a “buy” rating, signaling a potential 22.05% upside from the previous close. This adjustment came amid a broader consensus of analyst optimism: 20 of 26 analysts rated the stock as a “Buy” or “Strong Buy,” with a collective $65.86 price target. BMO Capital Markets and Mizuho also raised their targets to $68 and $68, respectively, reinforcing confidence in EQT’s near-term prospects.

EQT’s financial results further supported the positive sentiment. The company reported a $0.14 beat on EPS and a $2.09 billion quarterly revenue increase, driven by higher natural gas prices and production efficiency. Analysts highlighted the 7.25% return on equity and 23.59% net margin as indicators of robust operational performance. However, revenue fell short of the $2.13 billion estimate, introducing some short-term volatility. Zacks Research revised its FY2026/2027 EPS forecasts upward, reflecting improved earnings visibility, though it retained a “Hold” rating, underscoring cautious optimism.

Sector-level tailwinds also played a role. Rising U.S. LNG exports and clean-energy demand bolstered natural gas prices, directly benefiting EQT’s upstream operations in the Appalachian Basin. MarketBeat analysts noted EQT’s strong free cash flow and disciplined capital allocation as key differentiators, positioning the stock as a growth-at-a-reasonable-price (GARP) candidate. Conversely, insider transactions introduced uncertainty: CFO Todd James and EVP Sarah Fenton sold significant stakes, reducing their holdings by 35.6% and 6.7%, respectively. While these sales were disclosed as personal financial decisions, they raised questions about management’s long-term confidence.

Institutional activity added another layer of complexity. Hedge funds like Fortitude Family Office and Anchor Investment Management increased their stakes by 95.6% and 133.3%, respectively, while others, including Greykasell Wealth Strategies, entered new positions. Despite these inflows, 90.81% institutional ownership suggests a balanced investor base. Meanwhile, the AES acquisition by a related entity (EQT AB) sparked confusion but had no direct impact on EQT CorporationEQT+0.59%.

The stock’s trajectory remains tied to macroeconomic and operational factors. While natural gas prices and LNG demand provide near-term support, EQT’s ability to sustain earnings growth and execute capital discipline will be critical. Analysts’ mixed signals—from UBS’s 22% upside to MarketBeat’s $65.86 consensus—highlight divergent views on valuation and risk. For now, EQT’s moderate gains reflect a balance of sector optimism and cautious execution, with institutional and analyst dynamics shaping its near-term trajectory.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

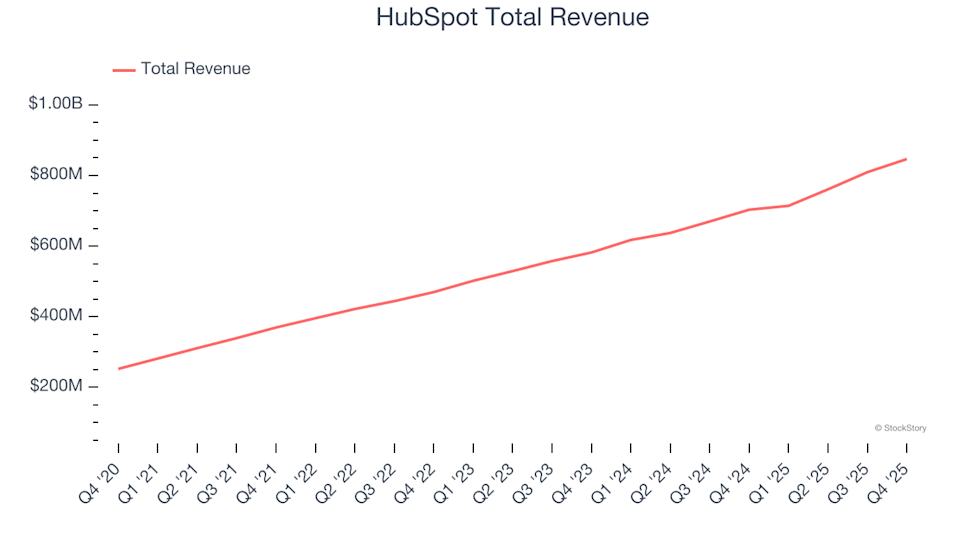

Sales Software Stocks Q4 Results: HubSpot (NYSE:HUBS) Delivers Strong Performance Across the Board

uniQure's Huntington's Therapy: A Regulatory Reset and the Price of Priced-In Hype

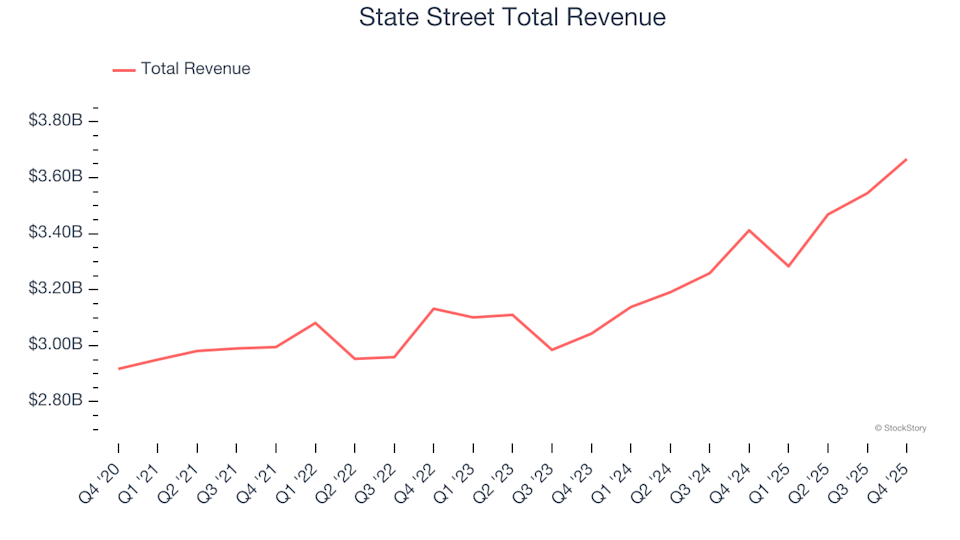

Custody Bank Stocks Q4 Performance: Comparing State Street (NYSE:STT)