Richardson Electronics (RELL): Should You Buy, Sell, or Keep After Q4 Results?

Richardson Electronics: Recent Performance and Investor Considerations

Over the last half-year, Richardson Electronics has delivered a notable performance, with its stock price climbing 26.9% to reach $12.40—outpacing the S&P 500 by 21.8%. This surge has been fueled in part by strong quarterly earnings, prompting investors to reassess their strategies regarding this stock.

Should you consider adding Richardson Electronics to your portfolio, or does it carry more risk than reward?

Reasons for Caution: Why Richardson Electronics May Lag

Despite recent gains, we remain cautious about Richardson Electronics. Below are three key concerns that make us hesitant about RELL, along with an alternative stock we prefer.

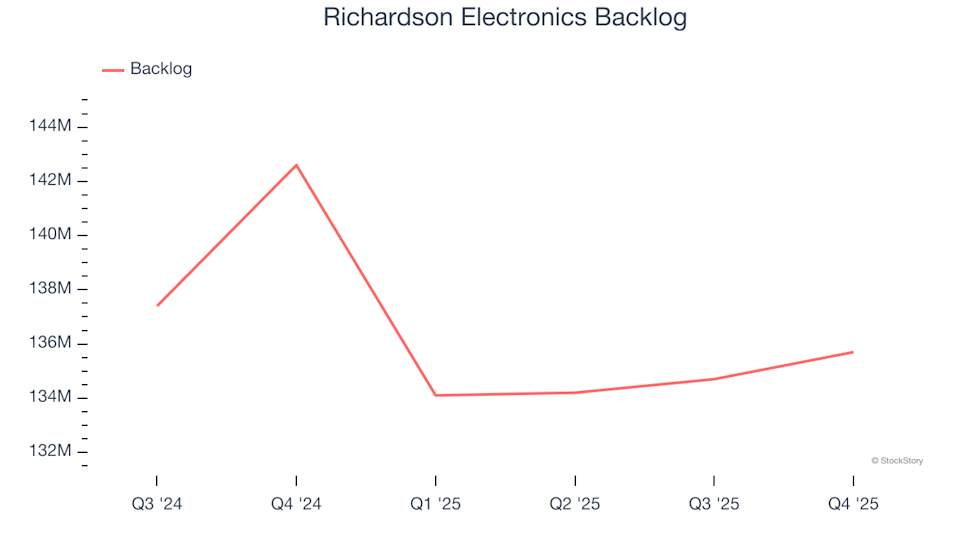

1. Shrinking Backlog Signals Fewer New Orders

For companies in the Specialty Equipment Distributors sector, backlog figures provide insight into future revenue potential by showing the value of orders yet to be fulfilled. In the most recent quarter, Richardson Electronics reported a backlog of $135.7 million, reflecting an average annual decline of 3.4% over the past two years. This downward trend suggests the company is struggling to secure new business, possibly due to heightened competition or a saturated market.

2. Flat Free Cash Flow Restricts Growth Opportunities

We place significant emphasis on free cash flow, as it represents the cash available to cover expenses and reward shareholders—unlike accounting profits. Over the last five years, Richardson Electronics has essentially broken even in terms of free cash flow, limiting its ability to reinvest in the business or return value to investors.

3. Declining ROIC Indicates Weak Returns on New Investments

Return on invested capital (ROIC) measures how efficiently a company generates operating profit from its capital base. While high ROIC is attractive, the direction of this metric is equally important. Unfortunately, Richardson Electronics has seen its ROIC fall sharply in recent years, compounding its already modest returns and signaling a lack of lucrative growth prospects.

Our Verdict

While we appreciate companies that deliver value to their customers, Richardson Electronics does not currently meet our investment criteria. The stock, trading at a forward P/E of 37.6 (or $12.40 per share), appears richly valued with much optimism already reflected in its price. We believe there are stronger opportunities elsewhere. Consider exploring a stable industrial company poised to benefit from ongoing industry upgrades.

Alternative Investment Ideas

Don’t Miss: This Week’s Top 6 Stock Picks

The current market environment is quickly distinguishing high-quality stocks from overpriced ones, especially as AI-driven shifts impact entire sectors. In such a fast-moving landscape, you need more than just a list of reputable companies.

Our AI-powered system identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rally, and Nvidia prior to its 1,178% climb. Each week, it highlights six new stocks that meet our rigorous criteria.

Our recommendations have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Kadant, which delivered a 351% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Quipt Home Medical Receives Final Order Approving Arrangement

From 5x to 15x? Top 5 Altcoins That Could Surge 400% in the Coming Epic Altseason

Banks Balk At Clarity Act As White House Pushes On

3 Major Reasons to Appreciate Brady (BRC)