AbbVie's Financial Results: Guidance Adjustment Falls Short of Whisper Expectations

Market Response: Selling on Positive News

When AbbVie released its latest earnings on February 4, the market responded with a familiar "sell the news" reaction. Despite surpassing expectations, shares declined. The reason? Investors had already factored in robust growth from the company’s immunology segment. The real test was whether Skyrizi and Rinvoq could compensate for the loss of Humira revenue—a challenge AbbVie met, but one that was widely anticipated.

AbbVie reported an adjusted profit of $2.71 per share, outpacing analyst projections of $2.65. The standout performance came from its newer immunology treatments: Skyrizi’s sales soared to $5.01 billion, a 32.5% increase that exceeded forecasts. While Rinvoq also posted gains, it was the combined strength of these drugs that drove the earnings beat—an outcome many investors had already anticipated.

Despite these strong results, the stock moved lower. The culprit was the company’s updated guidance. Although AbbVie raised its full-year outlook, investors scrutinized the details and found the increase less impressive than hoped. The market interpreted the guidance as a cautious adjustment rather than a sign of accelerating growth. As a result, the stock sold off once the company’s performance aligned with lofty expectations.

Revised Guidance: A Conservative Outlook?

The decline in AbbVie’s share price reflected not just the quarterly results, but also the company’s forward-looking statements. AbbVie lifted its full-year 2026 profit forecast, now expecting adjusted earnings per share between $14.37 and $14.57, above the consensus estimate of $14.24. While this appears to be an upgrade, the underlying message is more nuanced.

This guidance follows a year in which AbbVie achieved 8.6% operational revenue growth in 2025. The new forecast suggests a slower pace of earnings growth, especially considering the strong base established by the recent quarterly beat. Essentially, AbbVie’s updated outlook signals a more moderate expansion, resetting expectations for how quickly it can offset the decline in Humira sales.

This cautious tone has weighed on the stock. AbbVie’s shares have lagged behind both the broader market and its healthcare peers, reflecting skepticism about the company’s growth prospects. Investors appear to be factoring in ongoing challenges, including competitive pressures and the transition away from legacy products, despite the strength in immunology.

Upcoming Catalysts and Potential Risks

The gap between AbbVie’s valuation and its peers hinges on several near-term developments. The most immediate is the next earnings release, which will test whether the company can outpace the implied slowdown in its guidance. The market will be closely watching for evidence that AbbVie can overcome anticipated pricing pressures on Skyrizi and Rinvoq in 2026. Any shortfall in reaching the midpoint of the $14.37–$14.57 earnings range could reinforce concerns about future growth.

Beyond quarterly results, AbbVie’s drug pipeline represents a significant opportunity. Positive clinical trial outcomes for Rinvoq in 2026 could be transformative, with approvals expected for two new uses and key phase III data for additional indications. Each successful approval would introduce new revenue streams and help counteract pricing challenges. If the pipeline advances more rapidly than expected, it could prompt a reassessment of AbbVie’s valuation.

However, risks remain. The company’s recent dividend announcement—$1.73 per share quarterly—underscores its commitment to shareholder returns, but may also suggest a conservative approach to reinvestment. Additionally, ongoing weakness in the aesthetics and oncology divisions presents headwinds that immunology gains alone may not offset. Until these challenges subside, AbbVie’s shares may continue to trade at a discount.

Conclusion: Waiting for the Next Shift

Ultimately, AbbVie’s future trajectory will be shaped by how it navigates these catalysts and risks. The company’s ability to deliver results that surpass its tempered guidance—or to overcome persistent headwinds—will determine whether investor sentiment improves. For now, a cautious approach appears warranted as the market awaits clearer signs of renewed momentum.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

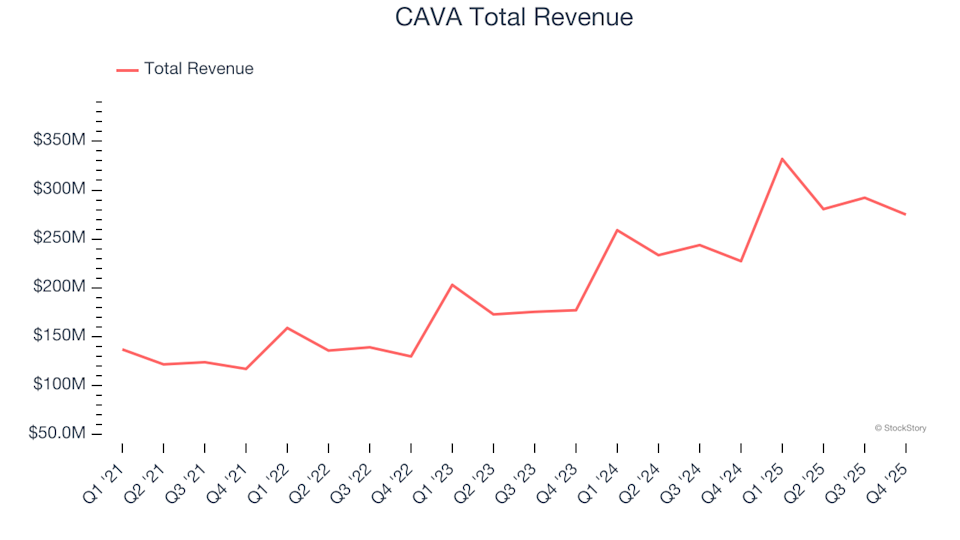

Q4 Results Overview: CAVA (NYSE:CAVA) Outperforms Contemporary Fast Food Chains

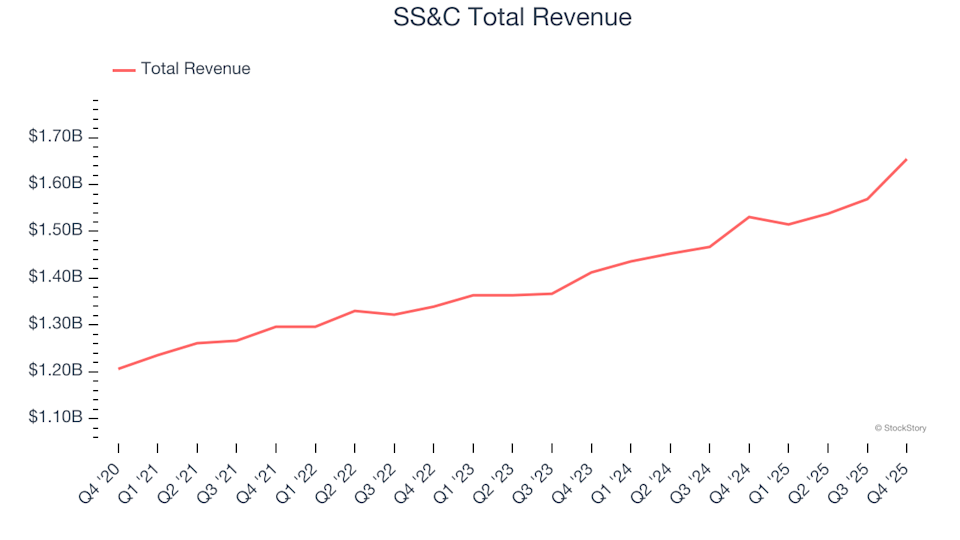

Q4 Financial Results Overview: SS&C (NASDAQ:SSNC) Compared to Other Data & Business Process Services Companies

Gold holds losses as strong dollar outweighs haven demand; set for weekly drop