Hillman (HLMN): Should You Buy, Sell, or Hold After Q4 Results?

Hillman Stock Performance: Recent Trends

In the last half-year, Hillman’s share price dropped to $8.33, resulting in a 17.9% loss for investors. This decline stands in stark contrast to the S&P 500’s 5.1% gain during the same period. The downturn was influenced in part by weaker-than-expected quarterly earnings, leaving many shareholders reconsidering their investment strategy.

Should You Consider Buying Hillman?

Is Hillman a smart addition to your portfolio, or does it carry too much risk?

Why We’re Not Enthusiastic About Hillman

Although the current price may seem attractive, we’re choosing to stay on the sidelines. Here are three key reasons why HLMN doesn’t stand out to us, along with an alternative stock we prefer.

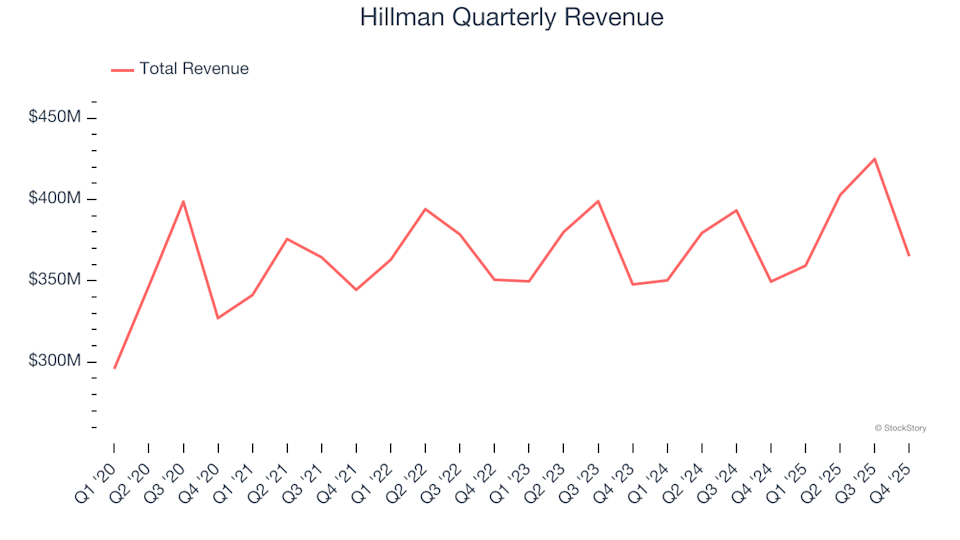

1. Underwhelming Long-Term Revenue Growth

Consistent sales growth over the years is a hallmark of a strong company. While any business can perform well in the short term, the best companies deliver sustained growth. Hillman’s annualized revenue increase of just 2.6% over the past five years falls short of our expectations.

Hillman Quarterly Revenue

2. Weak Free Cash Flow Margins Restrict Growth

Free cash flow is a crucial indicator because it reflects all operational and capital expenditures, making it difficult to manipulate. Over the last five years, Hillman’s free cash flow margin averaged only 2.6%, which is lower than what we typically expect from companies in the industrial sector. This limited cash profitability reduces the company’s ability to reinvest or return value to shareholders.

Hillman Trailing 12-Month Free Cash Flow Margin

3. Lackluster Results from Past Growth Investments

Evaluating how efficiently a company grows is essential, and return on invested capital (ROIC) measures how much profit is generated from the funds raised. Hillman’s five-year average ROIC was just 2.5%, which is below the average cost of capital for industrial firms. This suggests that previous growth initiatives have not delivered strong returns.

Hillman Trailing 12-Month Return On Invested Capital

Our Verdict

Overall, Hillman’s fundamentals do not meet our criteria for a high-quality investment. After the recent drop, the stock is trading at a forward P/E of 13.8 (or $8.33 per share), which is a reasonable valuation. However, the potential for gains appears limited compared to the risks. We believe there are more compelling opportunities in the market right now. For example, you might consider instead.

Top Stocks for Any Market Environment

DON’T MISS: Our Top 9 Market-Beating Stocks. The most successful stocks consistently outperform the market, year after year. These companies are characterized by strong revenue growth, increasing free cash flow, and exceptional returns on capital. The market has already recognized their strengths.

But according to our AI-driven analysis, there’s still room for further gains. Discover which nine stocks made our list this week—absolutely free.

Our selections include well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Exlservice, which delivered a 354% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Neo’s 2025 Financial Report Offers a Window Into Its $461M Treasury And Plans For Future Cycles

Wind farms increase the average household energy bill by £70

DOGEBALL vs Eggman vs Ozak AI: Which Project Qualifies as the Next 100x Crypto Presale in 2026

Here’s Why XRP’s Links to the Derivatives Market Are Important