MRSH Ranks 382nd in Daily Trading Volume as Stock Gains 0.09% Amid Strong Earnings and Institutional Buying

Market Snapshot

On March 5, 2026, MarshMRSH+0.09% & McLennan CompaniesMRSH+0.09% (MRSH) traded with a volume of $0.37 billion, ranking 382nd in market activity for the day. The stock closed with a 0.09% gain, maintaining a market capitalization of $89.38 billion. Key metrics include a price-to-earnings ratio of 21.90, a beta of 0.74, and a 52-week range of $170.37 to $248.00. The company’s Q4 2025 earnings of $2.12 per share exceeded estimates by $0.15, while revenue rose 8.7% year-over-year to $6.6 billion. Analysts project a forward EPS of $9.61 for the current fiscal year, with an average price target of $216.18 and a “Hold” consensus rating.

Key Drivers

Institutional Investment Activity Drives Confidence

Significant institutional buying activity in Q3 2025 underscored renewed investor confidence in MRSHMRSH+0.09%. Focus Partners Advisor Solutions LLC increased its stake by 99.1%, acquiring 5,997 additional shares, while Hanson & Doremus Investment Management raised its position by 31.3%. Other firms, including D.A. Davidson & CO. and Ashton Thomas Securities LLC, also added shares, collectively reflecting a trend of portfolio managers allocating capital to the firm. Institutional ownership now accounts for 87.99% of MRSH’s equity, signaling sustained institutional backing.

Analyst Revisions Highlight Mixed Sentiment

Recent analyst reports presented a mixed outlook. JPMorgan Chase & Co. cut its price target from $242 to $226 but maintained an “overweight” rating, while Raymond James Financial upgraded MRSH to “strong-buy” with a $225 target. Cantor Fitzgerald and Keefe, Bruyette & Woods also raised their price objectives, albeit modestly. Despite these upgrades, the stock’s average rating remains “Hold,” with 13% of analysts labeling it a “Strong Buy” and 75% recommending a “Hold.” This divergence reflects cautious optimism, balancing the company’s strong earnings performance with macroeconomic uncertainties.

Earnings Outperformance and Strategic Resilience

Marsh’s Q4 2025 results reinforced its operational strength. The firm reported $2.12 EPS, surpassing estimates by 7.61%, and generated $6.6 billion in revenue, a 8.7% year-over-year increase. A net margin of 15.42% and return on equity of 31.60% highlighted efficient cost management and asset utilization. These results, coupled with the company’s diversified business model spanning risk management, reinsurance, and consulting services, positioned MRSH as a resilient player in the financial services sector. Analysts noted the firm’s ability to navigate inflationary pressures and evolving market demands.

Dividend Policy and Capital Allocation

The firm’s quarterly dividend of $0.90 per share, payable on May 15, 2026, reinforced its appeal to income-focused investors. With a 1.9% yield and a payout ratio of 42.70%, the dividend appears sustainable. This capital allocation strategy, combined with a strong balance sheet (current ratio of 1.10, debt-to-equity of 1.20), underscores management’s commitment to shareholder returns. Institutional investors, particularly those with long-term horizons, may view the dividend as a stabilizing factor amid market volatility.

Sector Position and Competitive Dynamics

As a global leader in risk advisory and consulting, Marsh’s market position remains robust. Competitors like Aon plc and Arthur J. Gallagher & Co. face similar institutional interest, but MRSH’s recent earnings outperformance and strategic acquisitions in human capital consulting differentiate it. The firm’s focus on AI-driven analytics and digital transformation, highlighted in Mercer’s Global Talent Trends 2026 report, aligns with long-term industry trends. However, regulatory scrutiny and competition in the insurance brokerage sector could pose headwinds, necessitating continued innovation to maintain margins.

Forward-Looking Catalysts and Risks

Upcoming catalysts include the April 16, 2026, earnings release, with analysts expecting $3.25 EPS, and the potential impact of the Federal Reserve’s monetary policy on risk appetite. Risks include macroeconomic slowdowns affecting corporate risk management budgets and potential rating downgrades from agencies like S&P. Investors will also monitor the firm’s ability to sustain its 8.7% revenue growth amid a competitive landscape and evolving client needs.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

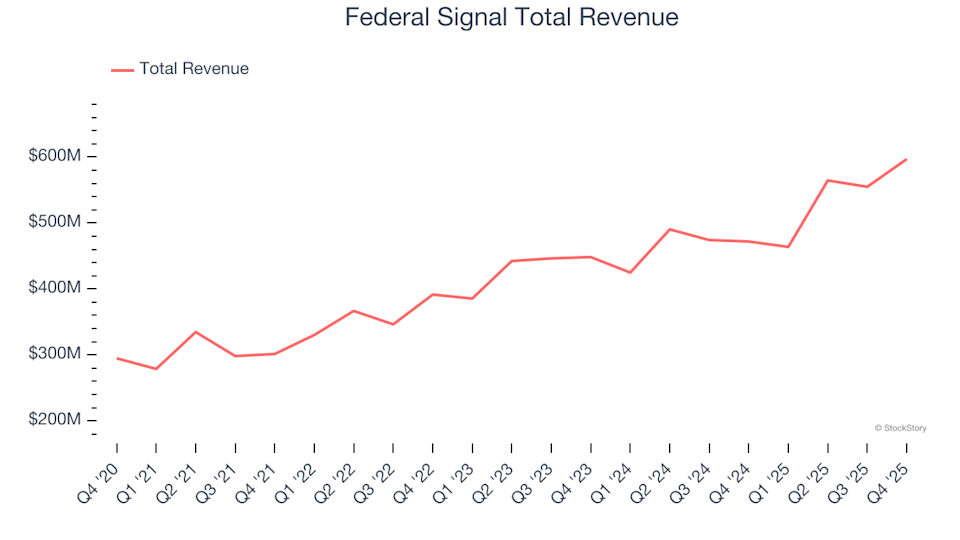

Heavy Transportation Equipment Stocks Q4 Analysis: Comparing Federal Signal (NYSE:FSS) With Its Competitors

Azitra's Failed Vote: A Tactical Play on Distressed Pricing and Dilution Risk