3 Reasons Why AN Is a Risky Choice and One Alternative Stock Worth Buying

AutoNation Stock Performance: Recent Trends and Investor Concerns

In the last half-year, AutoNation shares have dropped to $195.73, resulting in a 13.7% loss for investors. This decline stands in stark contrast to the S&P 500’s 5.1% gain over the same period. Weaker-than-expected quarterly earnings have contributed to this underperformance, leaving shareholders questioning their next steps.

Is AutoNation a smart buy at these levels, or could it pose additional risk to your investments?

Why We Expect AutoNation to Lag Behind

Despite the stock’s lower price, we’re choosing to stay on the sidelines for now. Here are three key reasons we’re not optimistic about AutoNation and prefer other investment opportunities.

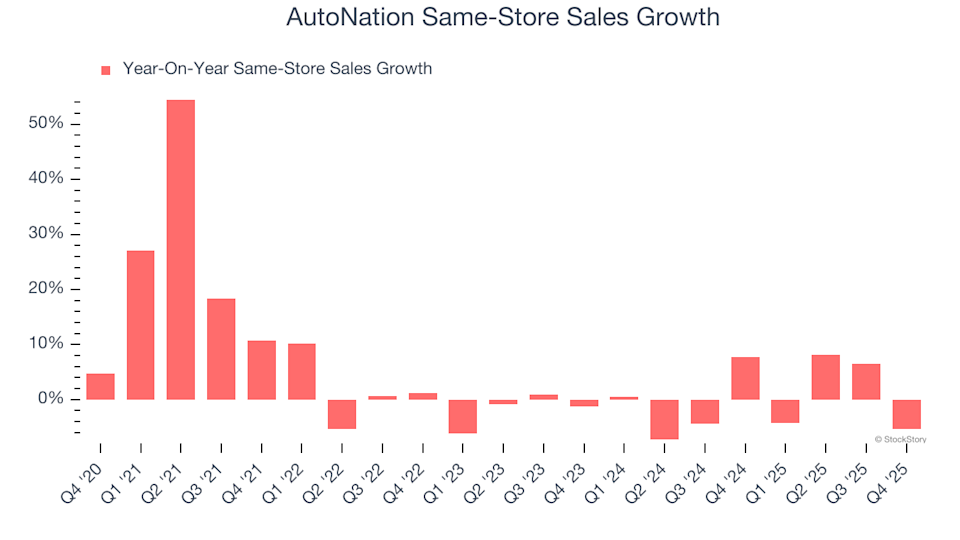

1. Stagnant Same-Store Sales Signal Weak Consumer Interest

Same-store sales track the year-over-year performance of retail locations and online platforms that have been open for at least twelve months, serving as a vital measure of organic growth.

For AutoNation, sales at established locations have shown little to no growth over the past two years, indicating tepid demand.

AutoNation Same-Store Sales Growth

2. Slim Gross Margins Highlight Structural Challenges

Gross margin is a crucial indicator of a retailer’s ability to set prices, differentiate products, and negotiate with suppliers.

AutoNation’s gross margin averaged just 17.9% over the last two years, reflecting limited pricing power and intense competition. For every $100 in revenue, the company spent $82.11 on supplier costs, which is a red flag for profitability.

AutoNation Trailing 12-Month Gross Margin

3. Limited Cash Reserves Raise Dilution Risks

For long-term investors, the greatest concern is a permanent loss of capital, which can occur if a company faces bankruptcy or is forced to raise funds under unfavorable conditions. Short-term price swings are less of a worry.

Over the past year, AutoNation used up $197.5 million in cash, and its debt of $10.18 billion far outweighs the $58.6 million in cash it holds. This heavy debt load, combined with ongoing losses, is a major concern.

AutoNation Net Debt Position

If AutoNation’s financial situation doesn’t improve soon, it may need to seek additional funding from investors, which could dilute existing shareholders’ stakes and put further pressure on returns.

We remain cautious on AutoNation until it can consistently generate free cash flow or successfully execute its financing plans.

Our Verdict

While we appreciate companies that provide value to consumers, we’re steering clear of AutoNation for now. After its recent drop, the stock trades at a forward P/E of 9.1 (or $195.73 per share). Although this may appear attractive, the company’s unstable fundamentals present significant downside risk. There are better investment opportunities available. For example, consider a leading digital advertising platform benefiting from the creator economy.

Stocks We Prefer Over AutoNation

Don’t Miss: This Week’s Top 6 Stock Picks — The market is quickly distinguishing high-quality stocks from overpriced ones, especially as AI disrupts entire sectors. In such a fast-moving environment, you need more than just a list of solid companies.

- Our AI identified Palantir before its 1,662% surge.

- It flagged AppLovin ahead of its 753% rally.

- It spotted Nvidia before its 1,178% climb.

Each week, our system highlights six new stocks that meet these rigorous criteria.

Our recommendations have included well-known names like Nvidia (+1,326% from June 2020 to June 2025) and lesser-known companies such as Kadant, which delivered a 351% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Expedia Group (EXPE) Stock Is Trending Overnight: What You Should Know

Foxconn reports that the Iran conflict has had minimal effects up to now

Spotting Top Performers: Lyft (NASDAQ:LYFT) and Gig Economy Shares in the Fourth Quarter

Bittensor (TAO) Tests Crucial $180 Level Amid Renewed AI + Crypto Interest