3 Motives to Offload PEBO and One Alternative Stock Worth Buying

Peoples Bancorp: Recent Performance and Market Comparison

Currently, Peoples Bancorp is trading at $32.76 per share, reflecting a 6% increase over the past six months—slightly ahead of the S&P 500’s 5.1% gain during the same period.

Should You Consider Investing in Peoples Bancorp?

Is this a good moment to add Peoples Bancorp to your portfolio, or is caution warranted?

Why Peoples Bancorp Fails to Impress

We’re opting to stay on the sidelines for now. Here are three reasons why Peoples Bancorp doesn’t stand out to us, along with a stock we prefer.

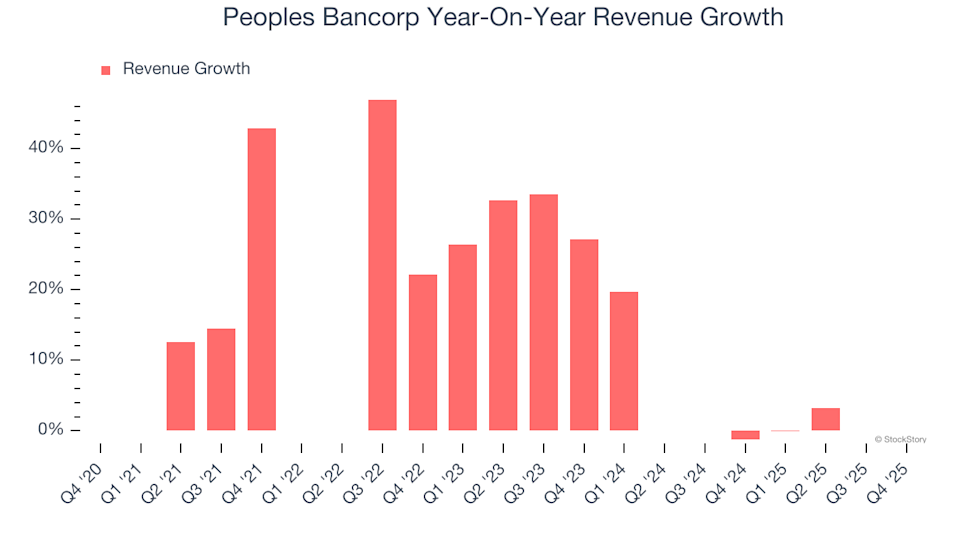

1. Sluggish Revenue Expansion

While long-term growth is crucial, focusing solely on historical trends can overlook recent shifts in interest rates and market dynamics. Over the past two years, Peoples Bancorp’s annualized revenue growth was just 3.5%, falling short of its five-year average and indicating a notable slowdown in demand.

Note: Certain quarters are excluded as they were affected by significant investment gains or losses, which do not reflect the company’s ongoing business fundamentals.

2. Declining Net Interest Margin

The net interest margin (NIM) measures how much a bank earns relative to its outstanding loans and is a key indicator of loan performance and pricing power. Over the last two years, Peoples Bancorp’s average NIM was 4.2%, but it shrank by 45.3 basis points during this period. This contraction put pressure on net interest income and may suggest increased competition for loans and deposits or an unfavorable shift in the company’s balance sheet mix.

3. Weak Earnings Per Share Growth

Examining long-term changes in earnings per share (EPS) helps determine if a company’s additional sales are translating into higher profits. Peoples Bancorp’s EPS grew at a modest 9.4% compound annual rate over the past five years, lagging behind its 17.9% annualized revenue growth. This indicates that profitability per share has diminished as the company expanded.

Our Verdict

While Peoples Bancorp is not a poor business, it doesn’t meet our standards for quality. The stock is currently valued at 0.9× forward price-to-book (or $32.76 per share), which is reasonable, but we don’t see significant upside at this time. We believe there are more attractive opportunities elsewhere. For example, consider exploring the leading e-commerce and payments company in Latin America.

Alternative Stocks Worth Considering

Don’t Miss: Top 5 Growth Stocks. The most successful stocks often share one trait: explosive revenue growth. Companies like Meta, CrowdStrike, and Broadcom were all identified early by our AI and have delivered returns of 315%, 314%, and 455%, respectively.

Discover which five stocks are on our radar this month—absolutely free.

Our list includes well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Comfort Systems, which delivered a 782% five-year return. Find your next potential winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Federal Realty (FRT) Price Target Raised to $125 at Ladenburg amid Retail REIT Re-Rating

UBS Cuts Harley-Davidson (HOG) Price Target; Morgan Stanley Sees Uneven Consumer Environment

UBS Cuts Harley-Davidson (HOG) Price Target; Morgan Stanley Sees Uneven Consumer Environment

Nick Szabo Warns Inscriptions Expose Node Operators to Legal Liability