3 Reasons Why BANF Carries Risk and One Alternative Stock Worth Considering

BancFirst’s Recent Performance: A Closer Look

In the past half-year, BancFirst’s stock price has dropped to $112.95, resulting in a 15.9% loss for shareholders. This stands in sharp contrast to the S&P 500, which has seen a 5.1% increase during the same period. Such a decline may leave investors reconsidering their positions.

Should you consider adding BancFirst to your portfolio now, or is caution warranted?

Why We’re Not Enthusiastic About BancFirst

Despite the lower share price, we remain skeptical about BancFirst’s prospects. Below are three key reasons we’re steering clear of BANF, along with a stock we prefer instead.

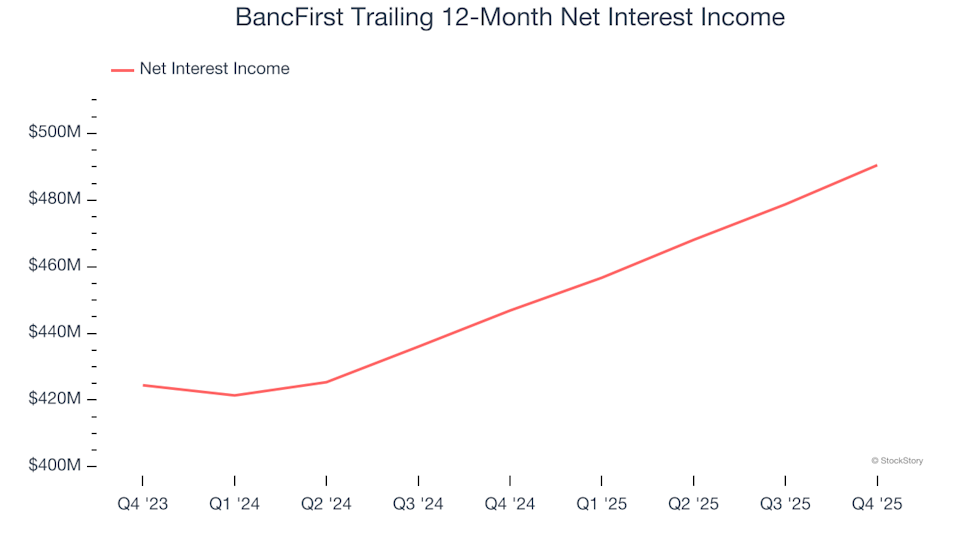

1. Net Interest Income Growth Signals Weak Demand

Based on our research, investors tend to focus on a bank’s net interest income growth, as recurring fee income is generally seen as less reliable. Over the past five years, BancFirst’s net interest income has increased at an annualized rate of 9.8%, which is slightly below the industry average and mirrors its overall revenue growth. This improvement was primarily due to a higher net interest margin, even as the bank’s loan portfolio contracted during this period.

2. Modest Net Interest Income Growth Forecast

Analyst projections for net interest income offer a glimpse into a company’s future potential. While forecasts aren’t always precise, accelerating growth often leads to higher valuations, whereas slowing growth can weigh on share prices. For BancFirst, analysts predict a 4.3% increase in net interest income over the next year—a slowdown compared to the 7.5% annualized growth seen over the previous two years.

3. Recent EPS Growth Fails to Impress

While long-term earnings trends are important, we also examine recent EPS performance for signs of change. BancFirst’s earnings per share have grown by just 6% annually over the last two years, which is consistent with its revenue growth. This suggests the company has maintained its profitability per share as it expanded.

Our Verdict

Ultimately, BancFirst’s fundamentals do not meet our investment criteria. After its recent decline, the stock is trading at 1.9 times forward price-to-book, or $112.95 per share. While some may see value here, our analysis indicates that the potential rewards are limited compared to the risks. We believe there are more attractive opportunities available. For example, consider one of our top picks in digital advertising.

Alternative Stocks Worth Considering

Discover the Top 9 Stocks Outperforming the Market. The most successful stocks consistently deliver strong results—year after year. These companies stand out for their impressive revenue growth, increasing free cash flow, and exceptional returns on capital. The market has already recognized their strength.

But according to our AI-driven platform, there’s still more room for growth. See which nine stocks made our list this week—absolutely free.

Our selections include well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Exlservice, which delivered a 354% return over five years. Start your search for the next breakout stock with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Expedia Group (EXPE) Stock Is Trending Overnight: What You Should Know

Foxconn reports that the Iran conflict has had minimal effects up to now

Spotting Top Performers: Lyft (NASDAQ:LYFT) and Gig Economy Shares in the Fourth Quarter

Bittensor (TAO) Tests Crucial $180 Level Amid Renewed AI + Crypto Interest