The global passenger EV market, including plug-in and conventional hybrids, fell short of 30 million units last year, but still showed robust growth of 18% year over year. In combined battery capacity deployed – a better indicator of battery materials demand than unit sales alone – the electric car market expanded by 22%.

According to data from Toronto-based EV supply chain advisory Adamas Intelligence, 2025 was the first calendar year battery capacity deployment topped 1 TWh. To put that in perspective, for calendar 2021, the total was 286 GWh, meaning the global market measured in GWh has nearly quadrupled in just four years and is ten times larger than in 2019 – powering through the pandemic.

Turnaround

The EV Metal Index pairs metals demand with prices in the EV battery supply chain. That paints a very different picture of the battery metals market and shows just how deep the slump of the last few years has been for raw material suppliers to the industry.

But even by this measure, the outlook has become much brighter. The raw material bill for the contained lithium, graphite, nickel, cobalt and manganese in the batteries of EV sold over the course of 2025 climbed to $15.6 billion, an 11% gain over the year before.

If $15.6 billion sound modest, the installed tonnage does not take into account any losses during processing, chemical conversion or battery production scrap (where yield losses often go well into double digit percentages and at much higher rates during startup) so required tonnes and revenues are meaningfully higher at supply chain entry points.

Granted, that’s still almost half of the extraordinary level reached in 2022, but 2026 is already shaping up to be another year of strong growth as rising lithium and nickel prices continue to work its way through the supply chain and cobalt prices stay on the boil.

The right chemistry

While lithium and graphite represents a relative constant in the EV industry, the demand for nickel and cobalt have been impacted by ongoing thrifting of the latter by automakers in NCM (nickel-cobalt-manganese) and NCA (nickel-cobalt-aluminum) batteries and both by ever faster adoption of LFP (lithium-iron-phosphate) cathode chemistries.

In 2025 LFP packs accounted for nearly half of the total in battery capacity deployed terms, despite a limited presence outside China (where it now commands a 70% and growing share of the market).

Some of the negative effects of LFP’s intrusion in markets in North America and Europe are being blunted by a parallel trend towards higher nickel content NCM batteries (60%-plus nickel content and more often 80% and above) which remains the go-to chemistry outside China.

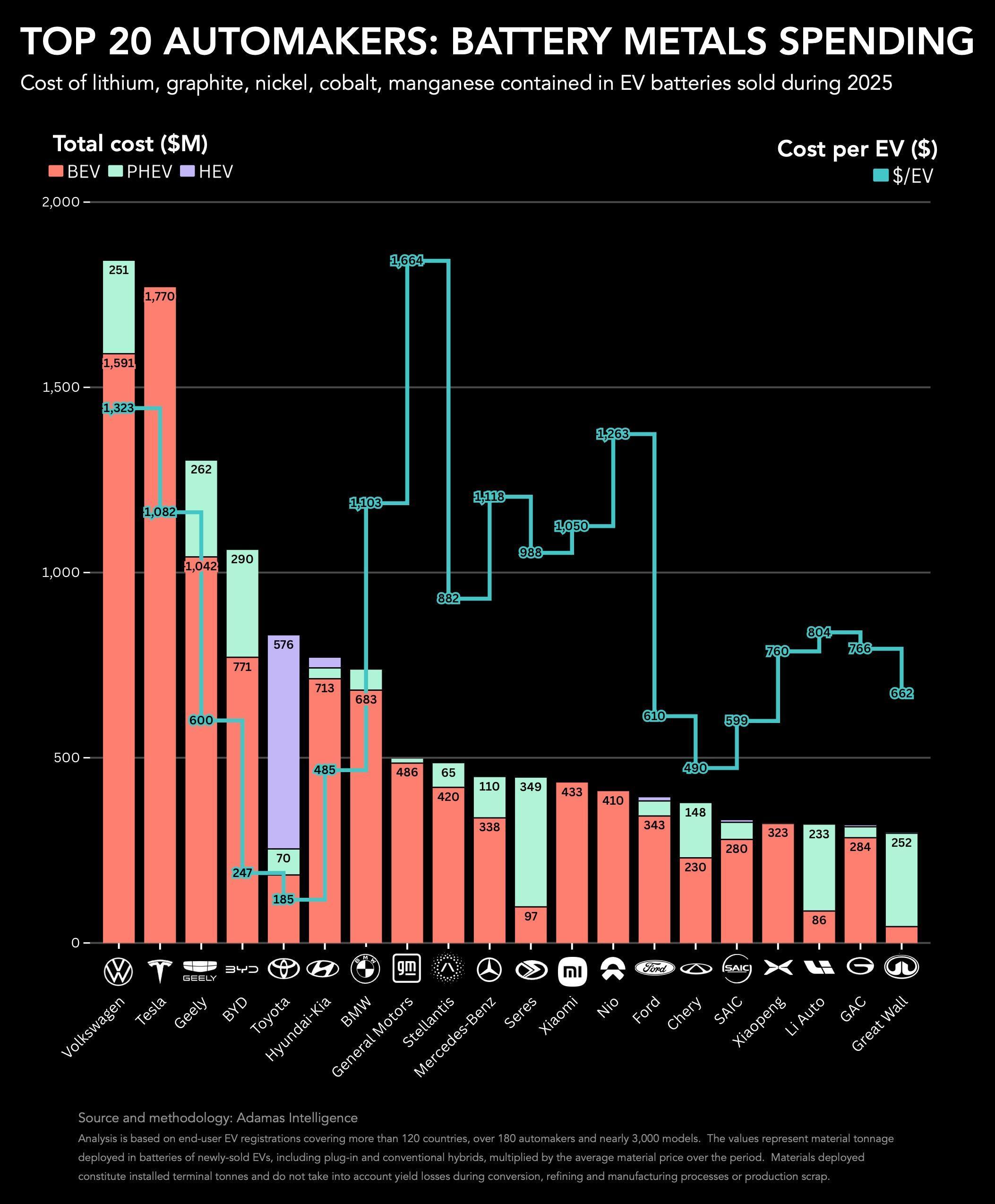

Volkswagen picks up speed

Drilling down from the overall figure shows vast differences between automakers in terms of battery metals usage and costs.

Despite selling nearly 500,00 more full electric vehicles last year than Tesla (and 2.2 plug-in hybrids), BYD’s bill of materials was $710 million below that of its Texas-based rival. BYD’s in-house manufactured batteries cost the Chinese company $1.1 billion in 2025, about the same as in 2024 despite selling 230,000 more BEVs and PHEVs than the year before.

BYD’s all lithium-iron-phosphate (LFP) battery-powered model line-up concentrated at the lower end of the market and a sales mix that is now majority plug-in hybrids kept sales-weighted average material costs per EV to just $247 versus $1,082 for every Tesla model sold.

Even when considering only fully electric vehicles, BYD’s spending on raw materials is way below the average at $366 per BEV. LFP-powered Models 3 and Y manufactured in China are a big part of Tesla’s sales but the slow buildout of LFP cell factories outside China means these nickel cobalt and manganese free powerpacks are largely absent from Western automakers’ lineups.

The comparable number for the Volkswagen stable which includes Audi, Porsche, Skoda and others – is $1,624 per BEV. EV sales by Volkswagen – for the first time the world’s biggest spender on battery metals – is split 70:30 for BEV:PHEV which accounts for some of its high-spending but the bulk of Wolfsburg’s budget went to battery nickel and cobalt. Volkswagen’s Powerco has commissioned an LFP battery plant in Germany and is building one in Spain targeting production some time next year.

Generally expensive

From Volkswagen, there’s another big step up to General Motors which has to contend with an average battery metals bill of a hefty $1,664 even after a rise of 17.6% year on year thanks to increasing use of nickel, cobalt and manganese prices and a 20 rise in EV shipments thanks the popular Equinox SUV and Silverado pickup.

On a GWh basis, 85% of GM’s batteries came from its venture with LG Energy Solution called Ultium. GM is overhauling this strategy after poaching a Tesla battery executive in 2024 and is moving away from its heavy and beefy one-size-fits-all packs. GM has been going in a different direction with the adoption of NCMA batteries, but the cost savings associated with LFP is just too compelling and the company is now retrofitting its Tennessee NCMA plant to produce LFP batteries.

On the other side of the spectrum is Toyota, which spent on average just $185 per EV sold in 2025 for a total of $830 million, up 7.2% year on year. That’s because of the Japanese giant’s focus on conventional hybrids or HEVs where battery capacity rarely exceeds 2kWh.

Last year 9 out of every ten Toyota (including Lexus) electrified vehicles sold were HEVs fitted with mostly nickel-metal-hydride batteries which also shows that the old-school Prius and its ilk are still a meaningful source of battery nickel demand (with a good dose of rare earths thrown in).

For a fuller analysis of the battery metals market check out the latest issue of the Northern Miner print and digital editions.

* Frik Els is Editor at Large for MINING.COM and Head of Adamas Inside, providing news and analysis based on Adamas Intelligence data.