USD: Danske Bank highlights jobs figures and yield trends

US February Jobs Report in Focus

The Danske Research Team points to the upcoming US February employment data as the main event, anticipating that Nonfarm Payrolls will decelerate to 70,000, while the unemployment rate is likely to remain at 4.3%. Initial jobless claims continue to be low, layoffs are subsiding, but productivity growth has slowed and unit labor costs have increased. Should the jobs report exceed expectations, it could intensify upward pressure on US bond yields and swap rates.

Labour Market Trends and Dollar Outlook

The most significant release today is the US February employment report. Recent high-frequency indicators—including jobless claims, ADP’s private sector employment estimates, and daily job postings tracked by Indeed Hiring Lab—have generally pointed to a strengthening labor market in February. Despite this, a moderate slowdown in Nonfarm Payroll growth is still anticipated, with an expected increase of 70,000 compared to January’s 130,000, and the unemployment rate projected to stay at 4.3%.

- Weekly jobless claims have held steady at 213,000 for the week ending February 28, remaining at historically low levels.

- Continuing claims have edged up slightly, but not significantly.

- The February Challenger report revealed a sharp drop in layoff announcements to 48,300 from 108,000 in January, even as hiring announcements stayed muted.

Productivity and Labor Costs

Preliminary data for Q4 shows productivity growth slowing to an annualized rate of 2.8%, down from 5.2% in Q3, mirroring the softer GDP figures. This slowdown has pushed unit labor cost growth up to 2.8% annualized, compared to a decline of 1.8% in the previous quarter. Overall, labor cost pressures in the US have moderated to relatively mild levels when viewed historically.

Market Implications

With the US labor market report set for release today, a stronger-than-expected outcome could further drive up bond yields and swap rates. While volatility indices like the VIX and Move, as well as credit spreads such as ITRAX, have risen, the Schatz ASW-spread has seen only minor changes. This suggests that, so far, there has not been a significant shift toward risk aversion as observed in previous periods.

(This report was produced with the assistance of artificial intelligence and subsequently reviewed by an editor.)

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin Price News: DeepSnitch AI Could Mirror BTC’s Early Run as Investors Place $2M Bet Ahead of March 31 Launch

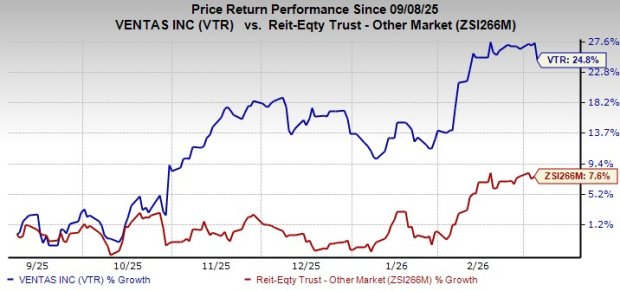

Ventas Stock Rallies 24.8% in Six Months: Will the Momentum Last?

Reasons Why You Should Retain Rollins Stock in Your Portfolio Now

Here's Why You Should Add DaVita Stock to Your Portfolio for Now