Intrepid Potash Navigates Oversupply with Trio Premium Pricing Strategy

Intrepid Potash's 2025 performance was a story of strong execution within a challenging market backdrop. The company achieved record sales volumes while simultaneously improving its cost structure, all against a global potash market characterized by ample supply and persistent pricing pressures.

The core of the story is volume growth. IntrepidIPI+10.57% posted combined potash and Trio sales volumes of over 590,000 tons in 2025, a 20% increase from 2024. This expansion was powered by a standout performance in its specialty fertilizer, Trio. The product hit a company record of 303,000 tons in sales volume for the year. More importantly, the company captured a meaningful price increase for Trio, with its average realized price in Q4 2025 at $379 per ton, which was 20% higher than the prior year quarter. This demonstrates the company's ability to command a premium for its differentiated product even as the broader market faced headwinds.

Cost efficiency was the other pillar of the 2025 results. Management achieved significant improvements in its unit economics, with potash COGS per ton down approximately 5% and Trio COGS per ton down over 10% year-over-year. These reductions were critical for protecting margins, especially for potash where the full-year average price saw a $25 per ton decline compared to 2024. The company's ability to lower costs while ramping production is a key competitive advantage.

This performance must be viewed through the lens of a well-supplied global market. The industry's scale is immense, with global potash shipments estimated at 75 million tons and projected growth of about 1.5 million tons in 2026. In this context, Intrepid's volume gains and cost cuts were necessary to maintain profitability.

| Total Trade | 3 |

| Winning Trades | 3 |

| Losing Trades | 0 |

| Win Rate | 100% |

| Average Hold Days | 6.33 |

| Max Consecutive Losses | 0 |

| Profit Loss Ratio | 0 |

| Avg Win Return | 10.45% |

| Avg Loss Return | 0% |

| Max Single Return | 17.7% |

| Max Single Loss Return | 0.2% |

The bottom line is that Intrepid delivered a powerful operational year. It grew sales, improved costs, and posted a full-year adjusted EBITDA of $63 million, an almost 80% improvement from 2024. Yet, this success was built on navigating a market where supply is ample and pricing is under pressure. The company's strategy of focusing on high-value Trio and driving down costs is the playbook for thriving in such an environment.

The 2026 Market Context: Supply Growth vs. Demand Replenishment

The commodity balance for potash in 2026 is set for a tug-of-war between steady supply expansion and firm demand for soil replenishment. The market is already well-supplied, with global potash shipments estimated at 75 million tons and projected growth of about 1.5 million tons in 2026. This indicates a market that is expanding but not facing a shortage. The key question is whether this supply growth can keep pace with demand without triggering a price collapse.

Demand is expected to remain robust, driven by a fundamental need to replenish nutrients after large 2025 harvests. As Nutrien's CEO noted, North American sales will be "driven by the need to replenish soil nutrients following a record crop". This dynamic is a recurring theme; farmers are focused on maximizing yield, and adequate fertilizer is essential. Furthermore, potash's relative affordability compared to other nutrients provides a buffer. Even as farmers face squeezed profits, they are less likely to cut back on potash, which is often the cheapest of the three major nutrients. This supports the view that demand should hold up.

Yet, the path isn't smooth. Some downward pressure on standard potash prices emerged in the fourth quarter of 2025, a trend that could persist. A key factor was the rapid pace of imports, particularly in southeast Asia. As one analyst pointed out, Indonesia and Malaysia alone increased imports by 1.1 million tons in 2025, and this surge eventually put some downward pressure on standard MOP prices. While Brazil's imports slowed late in the year, the overall trend of strong, affordable demand in key regions like Southeast Asia and Latin America suggests supply is meeting demand quickly, which can cap prices.

This context directly shapes Intrepid's 2026 outlook. The company's production guidance reflects a market where supply is ample and price pressure is a reality. Its potash output is projected to be flat to slightly down due to operational factors, a prudent move in a market where adding more tons could exacerbate oversupply. Conversely, the company is doubling down on its high-value specialty product, with Trio production guided to increase 7% at the midpoint. This strategy is a direct response to the commodity balance: by focusing on differentiated products where it can command a premium, Intrepid aims to insulate itself from the price pressures affecting standard potash. The market may be well-supplied, but the company's path to profitability is through selective growth and premium pricing.

Financial Health and Capital Allocation: Funding the Balance

Intrepid Potash entered 2026 with a fortress balance sheet, a critical advantage in a market where supply is ample and price pressure is a reality. The company ended the year with no debt or outstanding borrowings and a cash hoard of $83.5 million. This strong liquidity position provides the company with significant financial flexibility to fund its strategic priorities without external financing constraints.

That flexibility is being directed toward capital investment. Management expects 2026 capital expenditures to land in the range of $40 million to $50 million. This budget is squarely aimed at supporting the company's production forecasts, with the primary drivers being the construction of Primary Pond 8 at Wendover and sustaining capital at the East Mine. This level of spending is a clear commitment to maintaining and slightly expanding its operational footprint, even as potash output is projected to be flat to slightly down. The investment is focused on the core business, ensuring the company can meet its production targets for both potash and its high-value Trio segment.

With its financial base secure and capital needs mapped out, the company is now turning to the next stage of capital allocation. Management has indicated that discussions with the Board will be considered following the maintenance of sufficient liquidity. This signals a potential shift from pure reinvestment to a focus on returning capital to shareholders. The company's robust cash flow from operations, which totaled $55.8 million for the full year, provides the foundation for such a move. The strategic priority remains clear: fund the growth of the premium Trio business and maintain operational resilience, while positioning the balance sheet to support future shareholder returns. In a well-supplied market, this disciplined financial approach is a key part of the company's plan to navigate volatility and deliver value.

Catalysts and Risks: What to Watch in 2026

The path forward for Intrepid PotashIPI+10.57% hinges on navigating a set of clear, forward-looking signals that will test the company's execution and its strategic positioning within the well-supplied global market.

First, watch for any new tariff threats or geopolitical disruptions that could affect global potash trade. The market saw a 15% price gain in 2025 partly due to US tariffs on nearly all of the country's import partners. While prices are expected to remain steady in 2026, the persistence of such trade barriers creates uncertainty. Any escalation could disrupt supply flows and pricing dynamics, potentially benefiting producers like Intrepid that are not reliant on those import channels. Conversely, the easing of restrictions, as seen with China's partial lifting of phosphate export controls, could increase global supply and pressure prices. The company's ability to insulate its operations from these external shocks will be a key test.

Second, the company's own production forecasts are a critical near-term catalyst. Management has guided for potash production of 270,000 to 285,000 tons and Trio production of 285,000 to 300,000 tons in 2026. Meeting these targets, especially the 7% increase for Trio, is essential. It will directly impact the supply of its high-margin product and confirm the operational discipline needed to maintain its cost advantages. A miss on these volumes, particularly for Trio, would undermine the premium pricing strategy and signal execution challenges in a market where supply discipline is paramount.

Finally, the sustainability of cost improvements and pricing power must be assessed against a backdrop of high input costs. The outlook for 2026 includes low commodity prices coupled with high production costs, with natural gas prices projected to climb. This creates a squeeze. Intrepid's 2025 success came from driving down COGS per ton for both potash and Trio. The company must now maintain this momentum while facing potentially higher energy and operational expenses. Its ability to protect margins will depend on its continued operational efficiency and its capacity to pass on costs, a challenge in a market where farmers are already under financial pressure.

The bottom line is that Intrepid's 2026 performance will be validated by its ability to hit production targets, insulate itself from trade volatility, and defend margins against rising costs. The company's strategy of focusing on high-value Trio and a fortress balance sheet provides a strong foundation, but the commodity balance will be the ultimate arbiter of its success.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Best Crypto to Buy Now: Pepeto Targets 100x as Trump Nominates Crypto-Friendly Kevin Warsh as New Fed Chair

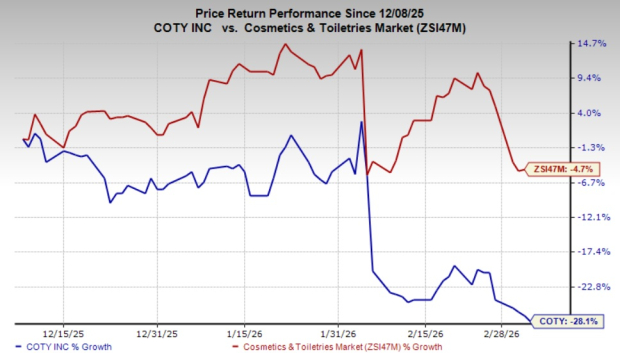

Coty Faces Slower Beauty Demand: What It Means for FY26 Sales

Ulta Beauty Q4 Earnings on Deck: Should Investors Expect a Beat?

FTAI Aviation Taps New CFO And Accounting Chief