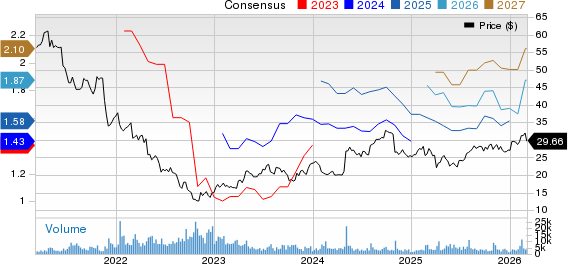

QQQ’s 29% Weight in Mega-Caps Turns Portfolio Exposure Into an All-or-Nothing Tech Play

Understanding Core ETF Risk and Return Profiles

When constructing any investment portfolio, it's essential to first grasp the distinct risk and return characteristics of foundational ETFs. SPY, DIA, and QQQ each provide exposure to different segments of the market, shaped by their unique historical performance and composition.

Between 1999 and early 2026, QQQ has outpaced its peers in total returns, transforming a $10,000 investment into $71,105.76. This impressive growth is largely attributed to its significant allocation to technology stocks, which have been the primary drivers of market gains. However, this comes at the cost of heightened volatility. QQQ’s annualized return of 7.56% surpasses SPY’s 5.59% and DIA’s 5.78%, but it also experienced a much steeper maximum drawdown of −83.94%, compared to −58.55% for SPY and −52.71% for DIA. Such deep losses during market downturns highlight the importance of understanding risk, not just returns.

The elevated volatility in QQQ stems from its concentrated holdings. Its top four stocks, led by Nvidia at 9.89%, make up 29.22% of the fund’s assets. This level of concentration introduces significant single-stock risk, far exceeding the diversification found in SPY or DIA. For investors seeking broad market exposure, this creates a heavy reliance on a handful of companies, increasing the risk of substantial losses if the tech sector underperforms.

In summary, SPY, DIA, and QQQ each offer different risk profiles. QQQ is geared toward aggressive growth and higher volatility, DIA provides a more defensive mix of industrials and financials, and SPY serves as a broad-market benchmark with an increasing tech presence. Portfolio managers must carefully consider how each ETF fits within their overall risk tolerance, hedging strategies, and diversification goals. Ignoring the historical risks and concentration of these funds can lead to unintended portfolio imbalances.

Thematic and Sector ETFs: Opportunities and Risks

Thematic ETFs, such as those focused on cloud computing or energy, are designed to capitalize on specific growth trends. However, they also introduce concentrated risks that require careful management. Unlike broad-market ETFs, these funds represent targeted bets on particular sectors or macroeconomic themes, often driven by a single factor that can heavily influence returns.

Recent performance in cloud-focused ETFs demonstrates this vulnerability. For example, Themes Cloud Computing ETF (CLOD) has fallen nearly 19% year-to-date, with a sharp 15% drop occurring in just one month. Similar funds like WCLD have also seen declines of about 22%. The main risk here is the sensitivity of these growth-oriented companies to changes in interest rates. Since cloud and software firms are valued based on future earnings, rising real rates can quickly erode their valuations, making Federal Reserve policy a critical factor for these ETFs.

Energy ETFs, such as XOP, present a different risk profile. These funds are closely tied to oil prices, resulting in high correlation with commodity cycles. While a surge in oil prices can boost returns, it also means the portfolio’s volatility and exposure to energy market shocks are amplified. This can leave investors vulnerable to geopolitical events and shifts in demand that may not affect the broader equity market.

For those employing quantitative strategies, the key takeaway is to treat thematic ETFs as tactical, rather than core, holdings. Their concentrated nature can magnify both gains and losses, so portfolios should be structured to manage these swings through hedging, careful position sizing, and maintaining overall diversification. Without these safeguards, thematic allocations can quickly distort a portfolio’s risk-return balance.

Case Study: SPY Mean Reversion Strategy

- Strategy Overview: Enter a long position in SPY when the closing price falls more than two times the 14-day ATR below the 20-day simple moving average (SMA). Exit the trade when the price closes above the 20-day SMA, after 10 trading days, or if a 5% take-profit or stop-loss is hit. The backtest covers the past two years.

- Performance Metrics:

- Strategy Return: 9.51%

- Annualized Return: 5.01%

- Maximum Drawdown: 7.49%

- Profit-Loss Ratio: 1.63

- Total Trades: 7

- Winning Trades: 4

- Losing Trades: 3

- Win Rate: 57.14%

- Average Hold Days: 6.57

- Max Consecutive Losses: 2

- Average Win Return: 4.46%

- Average Loss Return: 2.69%

- Max Single Trade Return: 8.58%

- Max Single Loss: 5.65%

Building a Balanced Portfolio: Allocation and Diversification

Effective portfolio construction for quantitative investors centers on maximizing risk-adjusted returns, rather than simply chasing the highest gains. This involves balancing core holdings with tactical satellite positions, while remaining vigilant about concentration risks.

The foundation of a robust portfolio typically consists of broad-market ETFs like SPY and DIA, which offer diversified exposure across sectors and market capitalizations. This core provides a stable base that can help absorb the volatility introduced by more concentrated satellite positions such as QQQ. For investors seeking systematic market participation with controlled risk, a blend of SPY and DIA is a prudent starting point.

Allocations to higher-risk, higher-reward ETFs like QQQ should be carefully sized according to the investor’s risk appetite and strategic goals. While QQQ’s historical outperformance is attractive, it comes with significant volatility and concentration risk—its top four holdings account for 29.22% of assets. As such, QQQ should be treated as a tactical allocation, not a core holding, and its position size should be limited to what the portfolio can withstand in the event of a major drawdown.

External factors, such as Federal Reserve interest rate decisions, can dramatically impact the risk and return of both core and satellite holdings. For example, rising rates tend to compress valuations for growth-oriented ETFs like QQQ and cloud funds, while trade policy changes can trigger sharp declines in broad-market ETFs, as seen with SPY’s 19% drop following tariff announcements. These macro risks must be considered when determining position sizes and hedging strategies.

Overexposure to any single ETF or sector is a major risk. The recent sharp declines in cloud ETFs serve as a reminder that concentrated bets can lead to significant, non-diversifiable losses. True diversification involves spreading investments across various ETF types—broad market, sector, and thematic—and ensuring that no single holding dominates the portfolio.

Ultimately, a disciplined, systematic approach is essential. Start with a diversified core, add tactical satellites with strict position limits, and hedge against key macro risks. This strategy is the most reliable way to manage volatility and pursue consistent, risk-adjusted returns over time.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Philips Unveils Rembra CT Scanner to Speed Up Medical Imaging

UVIX Jumps 13% As VIX Nears 'Fear Zone' Of 30, Volatility ETFs Surge

Boeing close to 500-Jet Order with Trump-Xi Summit, Bloomberg News reports