Best Artificial Intelligence Technology Shares to Purchase During the March Downturn

Why Long-Term Investors Should Consider AI and Tech Stocks During Market Dips

Entering March, those with a long-term investment horizon may want to take advantage of market pullbacks to acquire high-quality technology and artificial intelligence stocks.

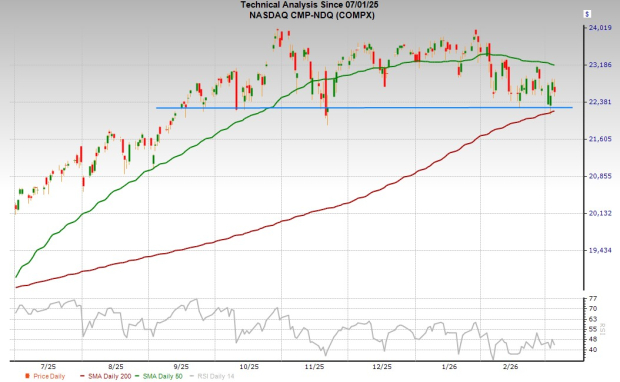

Despite heightened tensions in Iran and neighboring regions, buyers stepped in mid-week to support the Nasdaq at its 200-day moving average.

Of course, the situation in the Middle East remains fluid, and market conditions could shift rapidly in the coming days and weeks.

Image Source: Zacks Investment Research

Regardless of short-term volatility, history shows that purchasing stocks during periods of uncertainty and market downturns can be a successful strategy over time.

Additionally, Wall Street has largely looked past other recent global conflicts.

March Opportunity: Add Leading AI and Tech Stocks on Weakness

Investors should focus on the fundamentals—earnings and interest rates—which continue to favor equities. Recent results from Nvidia reinforced the ongoing surge in AI-related spending, even as some worry about a potential bubble.

In early January, Taiwan Semiconductor Manufacturing Company (TSMC) raised its 2026 capital expenditure forecast to $52–56 billion, a significant jump from $40.9 billion in 2025.

Major AI infrastructure providers are expected to collectively invest around $530 billion in capital expenditures this year, up from approximately $400 billion last year. This figure is likely to rise further, given the strong guidance from leading tech companies.

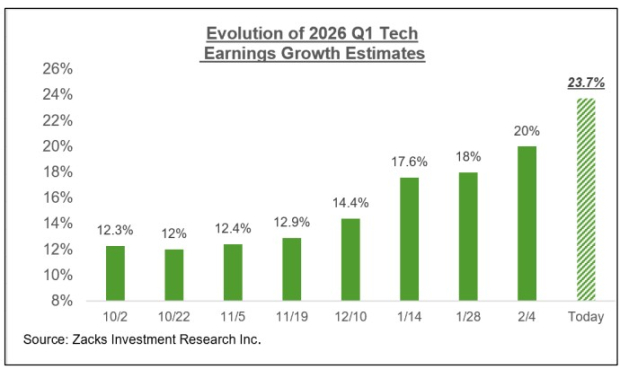

The chart below illustrates that projected Q1 2026 earnings growth for the technology sector has climbed to 24%, up from 18% in mid-January and 12% in early October.

Image Source: Zacks Investment Research

Furthermore, earnings growth is broadening across the market, with 15 out of 16 Zacks sectors expected to report year-over-year EPS gains in 2026.

On the interest rate front, many investors anticipate that the Federal Reserve will lower rates again in the latter half of 2026.

Let’s take a closer look at two AI-focused technology stocks that could be attractive buys during the current dip.

ServiceNow: Poised for a Potential 100% Rebound?

First up is ServiceNow (NOW), which has declined nearly 50% from its January 2025 peak, creating the possibility for a significant recovery if it returns to those highs.

ServiceNow exemplifies how AI-driven disruption is reshaping the software industry. The company has spent years integrating artificial intelligence into its digital workflow solutions, enhancing its value proposition for enterprise clients eager to innovate.

Specializing in software for IT, customer service, HR, and other business functions, ServiceNow describes itself as the “AI control tower for business reinvention,” reflecting its rapid adaptation to AI technologies.

Image Source: Zacks Investment Research

The company has strengthened partnerships with AI leaders, including a deepened multi-year agreement with OpenAI announced in January to enhance AI-driven enterprise experiences. ServiceNow is also expanding its collaboration with Anthropic to further embed Claude models into its AI platform.

While some fear AI could disrupt traditional software businesses, ServiceNow is proactively integrating advanced AI and forging alliances with top innovators. Its growth in 2025 and positive outlook highlight its momentum.

Image Source: Zacks Investment Research

In 2025, ServiceNow achieved its fourth consecutive year of 21–24% revenue growth, reaching $13.28 billion—more than double its 2021 revenue. This followed an earlier period of even faster expansion.

During Q4 2025, the company secured 244 deals worth over $1 million in new annual contract value, a 40% increase year-over-year. It ended the year with more than 600 customers generating over $5 million in ACV, up 20% from 2024.

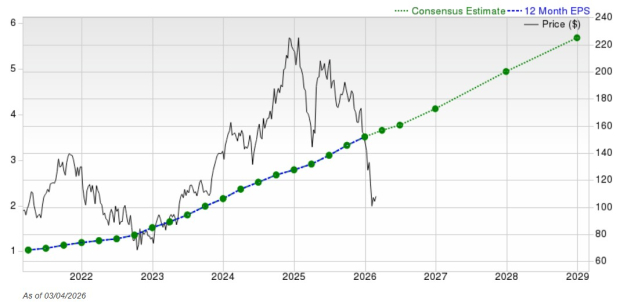

GAAP earnings rose 22% to $1.67 per share, compared to $0.23 in 2021, with adjusted EPS up 27%. The chart below shows ServiceNow’s strong long-term earnings growth trajectory.

Image Source: Zacks Investment Research

Looking ahead, ServiceNow is expected to grow revenue by 20% in 2026 and 18% in 2027, with adjusted earnings projected to rise 18% and 20%, respectively. Analyst estimates have improved since the Q4 report in January.

The company also announced an additional $5 billion for share repurchases, and CEO Bill McDermott recently purchased $3 million in NOW shares, calling it an ideal entry point.

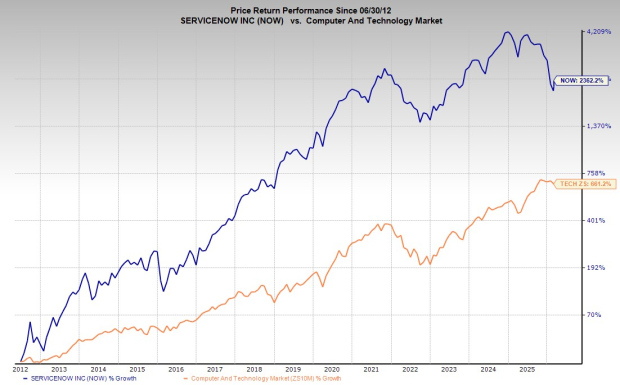

Since its IPO in 2012, NOW shares have outperformed the broader tech sector, soaring by approximately 2,300%—even after a 50% decline from 2025 highs. The stock recently found technical support after reaching its most oversold levels in a decade. A return to its previous peak could nearly double investors’ money, with the average Zacks price target suggesting about 70% upside from current levels.

Celestica: A Top AI Infrastructure Pick After a 25% Pullback

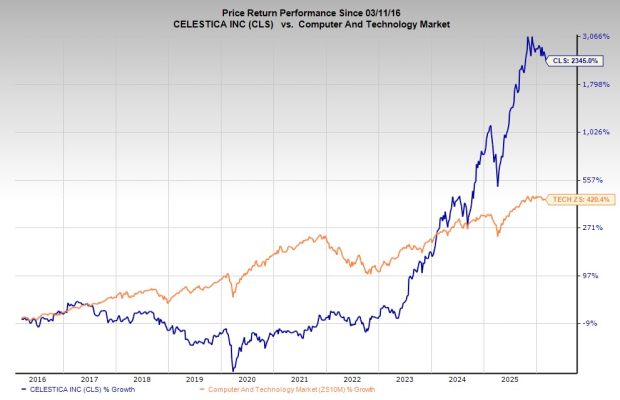

Celestica Inc. (CLS) is a major player in technology manufacturing, providing advanced electronic solutions for AI data centers and other cutting-edge applications. After years of challenges post-IPO, the surge in AI demand has transformed Celestica’s prospects.

Image Source: Zacks Investment Research

Celestica is a key supplier of high-performance electronics, including AI servers, networking equipment, and data center hardware for major clients—especially AI hyperscalers. The company also benefits from growth in aerospace, defense, telecommunications, healthcare technology, and supply chain solutions.

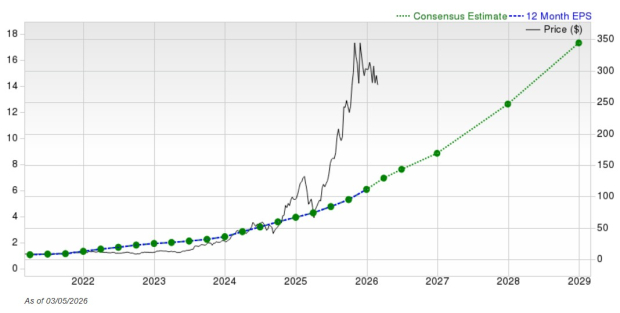

In 2025, Celestica’s revenue jumped 29% to $12.39 billion, more than doubling since 2021, fueled by AI-driven expansion. Adjusted earnings rose 56% last year, while GAAP EPS surged over 90%, following an average of 65% annual GAAP EPS growth from 2021 to 2024.

Image Source: Zacks Investment Research

In late January, Celestica issued strong guidance for 2026, citing robust demand for AI-related data center technologies. The company expects this growth trajectory to continue into 2027.

CEO Rob Mionis emphasized Celestica’s commitment to supporting customers’ long-term AI infrastructure investments. To meet this demand, the company plans to invest $1 billion in capital expenditures in 2026, funded entirely through operating cash flow.

Celestica is forecasted to grow revenue by 37% in 2026 and 39% in 2027, reaching $23.66 billion—nearly double its 2025 total.

Adjusted earnings are expected to climb 46% and 43% over the next two years. Following its Q4 report, Celestica holds a Zacks Rank #2 (Buy), with 15 out of 18 brokerage recommendations rated as “Strong Buy.”

Image Source: Zacks Investment Research

Celestica’s shares have soared nearly 3,000% over the past five years, far outpacing the Zacks Tech sector’s 100% gain—including a 220% increase in the past year alone.

For those who missed the rally, the stock is now down about 25% from its November highs, with the average Zacks price target indicating 34% upside from current levels.

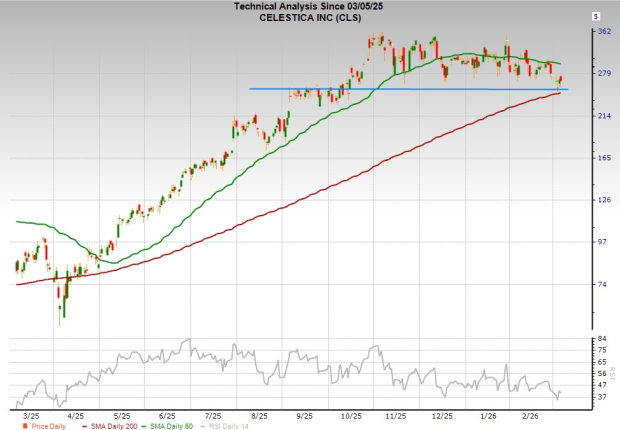

After its recent pullback and with strong earnings growth ahead, Celestica trades at 30 times forward 12-month earnings—about 50% below its peak. The stock found support at its pre-October breakout level and its 200-day moving average earlier this week.

This could be an opportune moment for both traders and long-term investors to consider this rapidly growing AI infrastructure stock at a discounted valuation.

Zacks’ Top Stock Picks for Potential 100%+ Gains

The Zacks research team has identified five stocks with the highest potential to double in value in the coming months. Among these, Director of Research Sheraz Mian highlights one lesser-known satellite communications company poised for significant growth as the space industry expands toward a trillion-dollar market. Analysts expect a major revenue surge in 2025. While not all picks will be winners, this one could outperform past standouts like Hims & Hers Health, which gained over 200%.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Iran's attacks on energy facilities in the Gulf unsettle markets and spark concerns about a possible recession

Webull’s slower path to profitability triggers sell-off as rising growth expenses outweigh revenue gains

Curve Finance accuses PancakeSwap of copying its code

SoftBank's OpenAI Bet: Positioning for the ASI S-Curve Inflection