Analysis-Investors cling to shock-absorber trades as Iran war brings economic visibility to zero

By Amanda Cooper

LONDON, March 6 (Reuters) - Some of the most crowded trades of the past year are emerging as the key shock absorbers for any potential market pain as war in the Middle East moves into a second week, bringing visibility over inflation and monetary policy to zero.

The dollar has emerged as the antidote of choice to combat angst. It’s set for its strongest weekly performance since late 2024, with a gain of 1.7%.

Surging oil and gas prices have reawakened fears of a 2022-style energy crunch, but there is not the sense of panic that has accompanied previous geopolitical or financial crises, investors and strategists say.

For starters, the classic indicators of market stress in times of turmoil, such as corporate bond spreads and the VIX volatility index, have not flared up, suggesting that investors still believe U.S. President Donald Trump’s assertion that the conflict will be resolved soon.

In addition, the vast amounts of capital that had pooled in some popular trades from gold to emerging-market assets have been deployed to plug losses elsewhere and insulate portfolios.

The most recent Bank of America monthly survey of global fund managers showed 50% believed owning gold, which has risen 70% in the last year, was the most crowded trade, followed by owning Big Tech stocks, while more asset managers were overweight emerging equities than at any time in the last five years.

It is these assets that have been hammered in the last week, along with bonds, which have encountered their worst weekly selloff in at least a year, as inflation expectations jump -- upending interest rate expectations.

But there is nothing that is bringing trading to a halt or creating enormous counterparty risk for the vast majority of the market participants, Kit Juckes, head of FX Strategy at Societe Generale, said. "There’s nothing that gums up the works of the system."

"There’s just a geopolitical shock that, for the sake of argument, has sent the dollar up, stocks down, and boosted some volatility and sent oil prices up very quickly."

VOLATILITY CONTAINED FOR NOW

Derivatives like cross-currency basis swaps, which reflect demand from foreign investors for dollars, or swap spreads, which can reflect risk appetite, and even junk bond indexes have been largely stable.

Those metrics surged after last April’s U.S.-triggered tariff turmoil, as they did during 2023’s regional banking crisis, the onset of COVID in 2020 and Russia’s invasion of Ukraine, as investors dumped assets in favour of hard cash.

Various measures of market volatility have spiked this week, but even those moves have been relatively benign.

The VIX index of equity volatility is hovering above 20, having risen by the most in a week since last November. This is a far cry from a doubling in value to a record 60 following Trump’s "Liberation Day" last April.

Similarly, in the bond market, the ICE BofA MOVE volatility index is also at its highest since November, at 75, but below last April’s highs around 140. And currency volatility has picked up, but far less so than it did even in late January, when Trump threatened to annex Greenland.

WARNING SIGNS FROM OIL

Energy is the fault line running through markets right now. Oil has risen more than 20% in a week, its biggest weekly gain in four years.

"When you look at past crises, we can see that generally the impact of past conflicts are relatively neutral for equities. We can see some shock, but after three months, six months, it’s relatively manageable," said Nicolas Forest, chief investment officer at Candriam.

When it comes to the oil price reaching $100, Forest said:

"That’s another story."

A potential energy shock adds to a plethora of market risks that the guardians of financial stability, such as central bankers and regulators, have warned about in recent months. From excess borrowing by hedge funds that dominate government bond trading, to a possible AI bubble, to risks building in private credit, banks and investors are already exposed to a range of vulnerabilities.

Kevin Thozet, an investment committee member at fund manager Carmignac, has maintained for some time that markets are underestimating the risk of a sustained pickup in inflation, particularly as global growth so far has been relatively resilient.

He believes inflation-linked bonds are a better portfolio option than nominal bonds.

"Even with oil nearing $90 a barrel, people are still underappreciating the risk of inflation over the medium term," he said.

For now, with so many questions about the rate outlook and long-term impact on the economy, investors are sticking with what they know.

"People are struggling to understand the answer of, ‘what do I buy?’" hedge fund BLKBRD’s owner and founder Dan Izzo said.

"Earlier this year and before the war in Iran, people were firmly rooted in buying assets in the rest of the world, certainly as AI and credit-related U.S. risks have emerged," he added.

"The war has shifted this thinking."

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Altcoins To Watch This Weekend | March 7 – 8

HYPE Price Upside May Struggle Despite $2.8 Million Short Squeeze Ahead

Jupiter Moves Forward with Two-Pronged Approach in Parkinson’s Studies and Consumer Goods

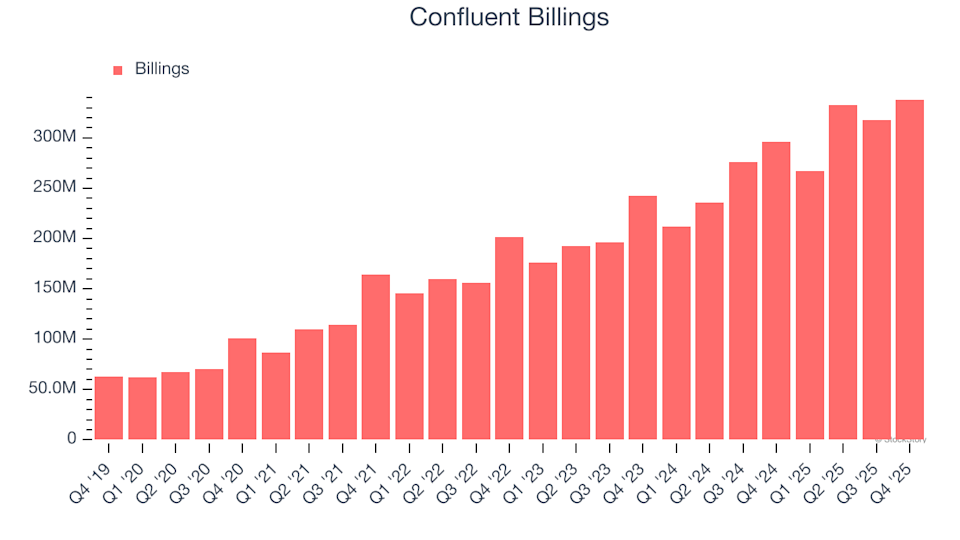

2 Things to Appreciate About CFLT (and 1 Drawback)