COO Drops Even After Surpassing Q1 Earnings Expectations and Upgrading FY26 Forecast

Cooper Companies Reports Strong Start to Fiscal 2026

The Cooper Companies, Inc. (COO) announced adjusted earnings per share (EPS) of $1.10 for the first quarter of fiscal 2026, marking a 19.6% increase compared to the same period last year. This result exceeded the Zacks Consensus Estimate of $1.03 by 6.8%, driven by operational improvements. On a GAAP basis, EPS reached $0.66, up 26.9% year over year.

Revenue Performance

The company generated $1.02 billion in revenue for the quarter, reflecting a 6% increase year over year on a reported basis and 3% growth organically. These results matched analyst expectations. At constant exchange rates (CER), revenue also rose 3%. Both of Cooper’s main business segments contributed to this top-line growth.

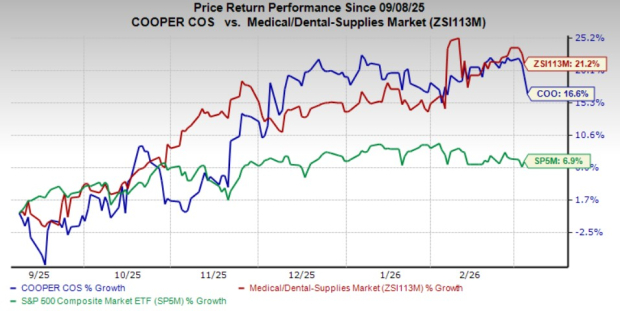

Despite the positive earnings report, COO shares fell 3.6% in after-hours trading on March 5. Over the past six months, the stock has climbed 16.6%, while the broader medical-dental supplies industry advanced 21.2% and the S&P 500 gained 6.9%.

Segment Highlights

Cooper Companies operates through two primary segments: CooperVision (CVI) and CooperSurgical (CSI).

CooperVision (CVI)

- Revenue: $695.1 million, up 8% year over year (reported), and 3% at CER and organically. This was close to the projected $696.4 million.

- Growth Drivers: Robust sales of MyDay and MiSight lenses, as well as increased demand for toric, multifocal, Biofinity, and Avaira products. MyDay lenses maintained double-digit growth, Biofinity and Avaira rose 3%, and MiSight surged 23%. However, Clariti lens sales remained weak as the market shifts toward premium products.

- By Category:

- Toric and multifocal: $351.2 million, up 10% (reported), 6% at CER and organically (projection: $352.7 million).

- Sphere and other: $343.9 million, up 5% (reported), 1% at CER and organically (projection: $343.7 million).

- By Region:

- Americas: $289 million, up 7% (reported), 6% at CER and organically (projection: $285.7 million), driven by strong demand for daily silicone hydrogel lenses.

- EMEA: $282.3 million, up 15% (reported), 4% at CER and organically (projection: $269.8 million), maintaining leadership in the region.

- Asia Pacific: $123.8 million, down 4% (reported, CER, and organically; projection: $140.9 million), as new product launches were offset by weaker sales in Japan due to declining demand for older hydrogel lenses.

CooperSurgical (CSI)

- Revenue: $329 million, up 3% (reported), 2% at CER and organically (projection: $327.9 million).

- Growth Drivers: Strong performance in global genomics, new product launches, clinical wins, and account expansions, partially offset by weaker sales in the Middle East and fewer equipment installations.

- By Category:

- Office and surgical: $202.4 million, up 2% (reported and organic), 1% at CER (projection: $206.6 million). PARAGARD sales declined after a previous quarter’s recovery, while medical devices grew 6% led by OB/GYN and specialty surgical products.

- Fertility: $126.6 million, up 6% (reported), 3% at CER and organically (projection: $121.3 million), supported by renewed clinic interest and improved cycles in the U.S. and Europe.

Profitability and Margins

Adjusted gross profit increased 5.3% to $697.7 million, though the adjusted gross margin narrowed by nearly 100 basis points to 68%, impacted by a less favorable sales mix in Asia Pacific and tariff pressures. Selling, general, and administrative expenses edged up 0.6% to $390.2 million, while R&D spending rose 8.8% to $44.3 million. Adjusted operating costs fell 0.4% to $422.3 million. Adjusted operating profit reached $275.4 million, up 13.8%, with the operating margin expanding by 200 basis points to 27%.

Financial Position

At the end of the first quarter, Cooper Companies held $124.9 million in cash and cash equivalents, up from $110.6 million at the close of fiscal 2025. Total debt stood at $2.5 billion, slightly lower than the $2.51 billion reported previously.

Updated Outlook for Fiscal 2026

Cooper Companies raised its guidance for the full fiscal year:

- Total revenue: $4.306–$4.346 billion (previously $4.299–$4.338 billion), indicating 4.5–5.5% organic growth. The Zacks Consensus Estimate is $4.32 billion.

- CVI segment revenue: $2.906–$2.932 billion (previously $2.900–$2.925 billion), also reflecting 4.5–5.5% organic growth.

- CSI segment revenue: $1.400–$1.413 billion (previously $1.399–$1.413 billion), suggesting 4–5% organic growth.

- Adjusted EPS: $4.58–$4.66 (previously $4.45–$4.60). The consensus estimate is $4.51.

Company Performance and Outlook

Cooper Companies began fiscal 2026 on a strong note, surpassing earnings expectations for the first quarter. The company’s operating margin continued to improve, supported by effective cost controls. Free cash flow reached $159 million, reflecting robust profitability and better working capital management. The CVI segment led performance, fueled by demand for premium daily silicone hydrogel lenses and the MyDay product line. CSI benefited from positive fertility trends and steady demand for consumables and surgical devices. However, the Asia Pacific region faced challenges, mainly due to declining sales of older hydrogel lenses in Japan.

Looking ahead, several factors are expected to drive growth, including the expansion of premium lens offerings (notably MyDay and MiSight), new private-label contracts, and stronger commercial momentum in the Americas and EMEA. Operational efficiencies from last year’s restructuring and increased use of AI-driven automation are also anticipated to support margin gains and free cash flow. Nevertheless, softness in Asia Pacific—especially Japan—and uncertainties in the Middle East fertility markets, along with pricing competition in parts of Asia, may limit growth in the near term. Management anticipates stronger momentum in the second half of the year as new product launches and market recoveries take effect.

Stock Ranking and Other Notable Picks

COO currently holds a Zacks Rank #2 (Buy).

Other highly ranked stocks in the medical sector include:

- Globus Medical (GMED): Zacks Rank #1 (Strong Buy). Reported Q4 2025 adjusted EPS of $1.28, beating estimates by 20.8%. Revenue of $826 million exceeded expectations by 4.9%. Long-term earnings growth is projected at 9.6% versus the industry’s 14%. The company has outperformed earnings estimates in the last four quarters, with an average surprise of 13.2%.

- Pacific Biosciences of California (PACB): Zacks Rank #1. Reported a Q4 2025 adjusted loss per share of $0.12, surpassing estimates by 36.8%. Revenue of $45 million topped expectations by 9.4%. The company’s estimated earnings decline rate is 1.9%, compared to the industry’s 11.4% improvement. PACB has beaten earnings estimates in each of the last four quarters, with an average surprise of 27.7%.

- Edwards Lifesciences (EW): Zacks Rank #2. Reported Q2 fiscal 2026 adjusted EPS of $0.58, missing estimates by 6.5%. Revenue of $1.57 billion exceeded expectations by 2%. Long-term earnings growth is projected at 12.9% versus the industry’s 14%. The company beat estimates in three of the last four quarters, with an average surprise of 5.5%.

Analyst Insights and Additional Resources

Zacks’ research team has identified five stocks with the potential to double in value, including a standout satellite-based communications company poised for significant growth as the space industry expands. While not all picks are guaranteed winners, this selection could outperform previous high-flyers like Hims & Hers Health.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin dip may not be over as retail ramps up buying below $70K: Santiment

CleanSpark and Bitcoin miners’ selling spree – Is the miner HODL era ending?

Bitcoin’s $70K bull-bear battle: How FOMO could tip BTC’s scales

Lantronix’s MediaTek Edge AI Venture Awaits Proof at Embedded World 2026 Challenge