Serve Robotics to Report Q4 Earnings: Buy Now or Wait for Results?

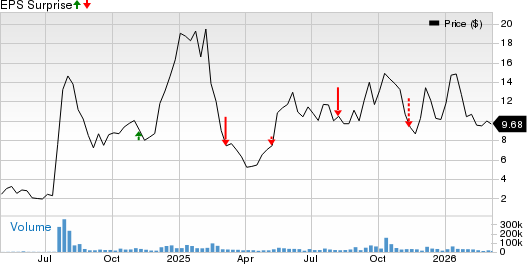

Serve Robotics Inc. SERV is scheduled to report fourth-quarter 2025 results on March 11, before the opening bell. In the last reported quarter, the company registered an earnings miss of 46%.

SERV’s Estimates Revisions

The Zacks Consensus Estimate for fourth-quarter adjusted loss per share is pegged at 49 cents. In the past 30 days, earnings estimates for the current quarter have been stable. In the prior-year quarter, the company reported an adjusted loss per share of 23 cents. For revenues, the consensus estimate is $0.8 million, implying a 320.6% year-over-year increase.

What the Zacks Model Unveils

Our proven model doesn't conclusively predict an earnings beat for Serve Robotics this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. This is not the case here.

Earnings ESP: Serve Robotics has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank: The company carries a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Serve Robotics Inc. Price and EPS Surprise

Serve Robotics Inc. price-eps-surprise | Serve Robotics Inc. Quote

What’s Shaping SERV’s Q4 Results?

SERV’s revenues in fourth-quarter 2025 are likely to have been aided by the rapid expansion of its autonomous delivery robot fleet and broader market presence. The company crossed a key milestone of deploying more than 1,000 robots and significantly increased its operational footprint across multiple cities. A larger fleet and expanded coverage are likely to have enabled higher delivery volumes and improved robot utilization, supporting stronger revenue generation during the quarter.

SERV’s top line is also likely to have been supported by the expansion of strategic partnerships with major delivery platforms and restaurant brands. The company added a partnership with DoorDash while continuing to collaborate with Uber, giving its robots access to a large portion of the U.S. food delivery market. This multi-platform approach allows robots to complete deliveries from different platforms, increasing order flow and operational efficiency, which are likely to have boosted revenue growth.

Another factor that is likely to have aided SERV’s fourth-quarter revenues is the growing contribution from additional monetization streams such as branding and software services. As the robot fleet scaled, the company unlocked more branding opportunities and continued transitioning its software offerings toward recurring revenues. The combination of fleet expansion, higher delivery activity and growing platform-related revenues is likely to have provided a meaningful boost to SERV’s top line.

However, SERV’s bottom line in fourth-quarter 2025 is likely to have been pressured by elevated operating costs tied to aggressive expansion and technology investments. The company continued spending heavily on research and development to advance its autonomy technology, while also investing in new market launches, robot production and integration of acquisitions. These investments are likely to have driven higher operating expenses, weighing on profitability despite revenue growth.

Price Performance & Valuation

SERV’s shares have surged 30.3% in the past year, outperforming the Zacks Leisure and Recreation Services industry and the S&P 500. The stock has also outpaced its industry peers, including C3.ai, Inc. AI and Cognizant Technology Solutions Corporation CTSH, down 58.4% and 21%, respectively, in the same time frame.

Price Performance

Image Source: Zacks Investment Research

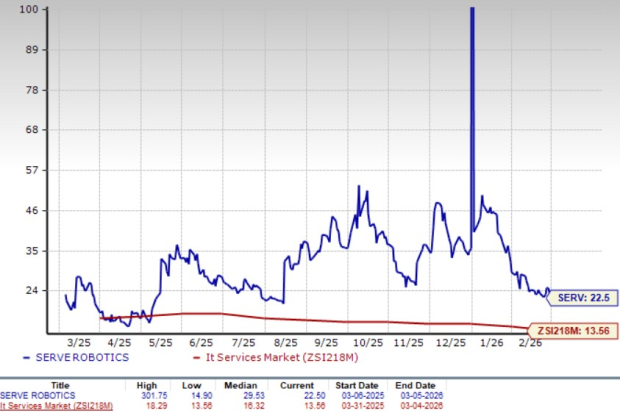

From a valuation perspective, SERV is trading at a premium. The company has a forward 12-month price-to-earnings of 22.5X, above the industry average.

P/S (F12M)

Image Source: Zacks Investment Research

Investment Considerations

Serve Robotics appears to be building strong long-term growth momentum, supported by the rapid expansion of its autonomous delivery robot fleet, a wider operational footprint and partnerships with major delivery platforms and restaurant brands. These initiatives are likely to have improved delivery volumes, platform utilization and new revenue streams such as branding and software services, indicating a promising demand outlook for the company’s technology.

However, the company is still in a heavy investment phase, with rising spending on research, technology development and market expansion continuing to pressure profitability. At the same time, the stock trades at a relatively rich valuation after a strong run, which limits near-term upside and increases the risk of volatility around earnings. Given the company’s growth potential but ongoing cost pressures and premium valuation, existing investors may consider holding the stock to benefit from its long-term opportunities, while new investors may be better off waiting for a more attractive entry point or clearer signs of sustained profitability.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Samsara (IOT) Climbs 19.5% as Firm Nearing Profitability

Amprius (AMPX) Soars to All-Time High on PT Hike After Earnings Blowout

Bitcoin Big-Money On The Move: Exchange Whale Ratio Spikes To 0.6

JD.com (JD) Climbs 6% on Analyst 'Buy' Reco