Water Infrastructure Q4 Results: Watts Water Technologies (NYSE:WTS) Stands Out as the Top Performer

Q4 Review: Water Infrastructure Industry Leaders and Laggards

With the fourth quarter earnings season wrapping up, it's an ideal moment to evaluate which companies in the water infrastructure sector, such as Watts Water Technologies (NYSE:WTS), stood out and which struggled.

Growing emphasis on water conservation and efforts to combat groundwater depletion are driving demand for advanced water infrastructure and treatment solutions. Companies that innovate—particularly those offering automated or smart technologies—are well-positioned to benefit from these trends, potentially accelerating product replacement cycles. However, the sector remains sensitive to broader economic shifts, with factors like consumer spending and interest rates influencing industrial activity and, consequently, demand for water infrastructure products.

Among the five water infrastructure firms we monitor, the fourth quarter was generally sluggish, with collective revenues falling short of analyst forecasts by 4.5%.

This underperformance has been reflected in share prices, which have dropped an average of 12.6% since the most recent earnings announcements.

Top Performer: Watts Water Technologies (NYSE:WTS)

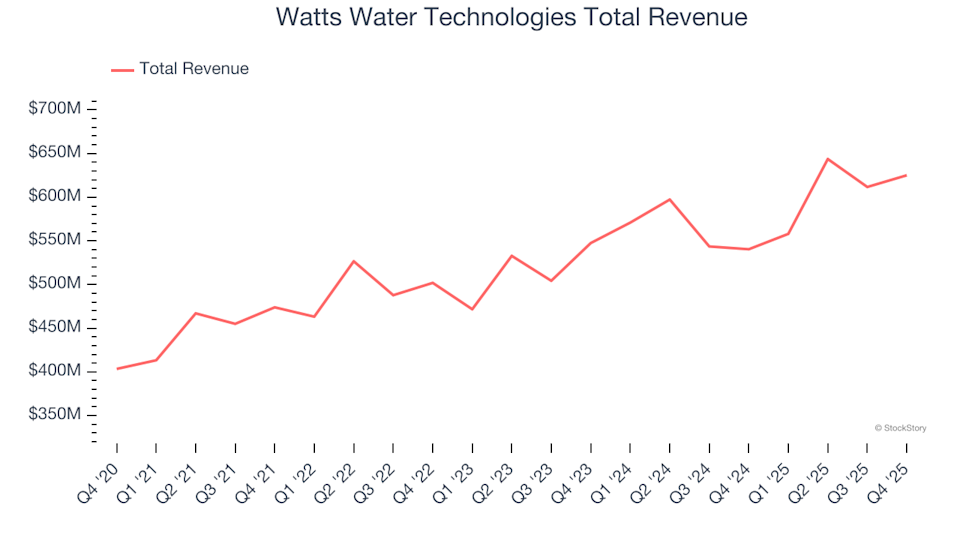

Established in 1874, Watts Water Technologies is a global provider of water systems and products serving residential, commercial, and industrial markets.

The company posted $625.1 million in revenue for the quarter, marking a 15.7% increase year-over-year and surpassing analyst projections by 2.3%. Watts delivered a standout quarter, exceeding expectations for both EBITDA and adjusted operating income.

CEO Robert J. Pagano Jr. credited the company’s record-breaking quarterly and annual results—including all-time highs in sales, operating income, and earnings per share—to the dedication of the Watts team. He also highlighted ongoing efforts to deliver innovative solutions for water safety, conservation, and energy efficiency, as well as productivity improvements through the One Watts Performance System.

Watts Water Technologies achieved the highest revenue growth and the largest outperformance relative to analyst expectations among its peers. Despite these strong results, the stock price has remained steady since the report and is currently trading at $313.19.

Mueller Water Products (NYSE:MWA)

Mueller Water Products, one of the industry’s oldest names, supplies water infrastructure and flow control solutions across multiple sectors.

For the quarter, Mueller reported $318.2 million in revenue, a 4.6% year-over-year increase and 2% above analyst expectations. The company delivered a robust quarter, outperforming on adjusted operating income and providing full-year EBITDA guidance that exceeded forecasts.

Mueller Water Products Total RevenueInvestors responded positively, with the stock rising 4.9% since the earnings release. Shares are currently priced at $28.88.

Lowest Performer: Energy Recovery (NASDAQ:ERII)

Energy Recovery, known for saving over a trillion gallons of water, supplies energy recovery devices to industries such as water treatment, oil and gas, and chemical processing.

The company’s quarterly revenue was $66.87 million, unchanged from the previous year and 19% below analyst expectations. This quarter was notably weak, with significant misses on both revenue and EBITDA estimates.

Energy Recovery posted the poorest results relative to analyst forecasts in the group. Unsurprisingly, its stock has fallen 33.3% since the earnings announcement and is now trading at $10.75.

Xylem (NYSE:XYL)

Xylem, which originated from a corporate spinoff, manufactures and services engineered products primarily for water-related applications.

The company reported $2.40 billion in revenue for the quarter, a 6.3% year-over-year increase and 1.1% above analyst estimates. Xylem also exceeded expectations for organic revenue and EBITDA.

However, Xylem issued the weakest full-year guidance update among its peers. Its stock has declined 9.6% since the earnings report and is currently valued at $126.70.

Tennant (NYSE:TNC)

Tennant, the world’s largest maker of autonomous mobile robots, designs and produces cleaning equipment for a range of industries.

Quarterly revenue came in at $291.6 million, representing an 11.3% year-over-year decline and missing analyst forecasts by 9%. The company also issued full-year EBITDA guidance and revenue estimates that fell significantly short of expectations.

While Tennant raised its full-year guidance more than any peer, it also recorded the slowest revenue growth. The stock has dropped 24.6% since the earnings release and is now trading at $62.05.

Looking for Strong Growth Opportunities?

If you’re interested in companies with robust fundamentals, explore our Top 5 Growth Stocks and consider adding them to your watchlist. These businesses are well-positioned to thrive regardless of economic or political changes.

The StockStory analyst team—comprised of experienced professional investors—leverages quantitative analysis and automation to deliver timely, high-quality market insights.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Ondas Shares Plunge 6.29% Amid $1.7 Billion Trading Surge, Ranks 57th in Overall Activity

Cisco's AI Pivot and Macro Woes Send Trading Volume to 62nd Busiest Stock

Circle Stock Drops to 56th Place in Trading Volume as Institutional Optimism Meets Insider Sell-Off