DVN Has Surpassed Industry Performance Over the Last Six Months: What’s the Best Way to Trade This Stock?

Devon Energy's Recent Market Performance

Over the last half-year, Devon Energy Corporation (DVN) has seen its stock price climb by 29%. This growth has surpassed the returns of both the Zacks Oil & Gas Exploration and Production - United States sector, which rose 14%, and the broader Zacks Oil and Energy sector, which increased by 26.7%. Devon Energy also outperformed the S&P 500, which posted a 6.9% gain during the same period.

The company’s success is driven by its high-quality assets across multiple basins, ongoing cost control measures, prudent debt management, and targeted investments to enhance and expand its operations. However, Devon faces headwinds from industry competition and volatile energy prices.

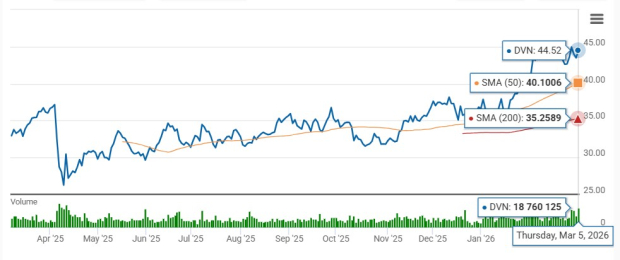

Six-Month Price Trend

Source: Zacks Investment Research

Another notable performer in the sector is Diamondback Energy (FANG), which focuses on the Permian Basin and has achieved a 30.4% increase in its stock price over the past six months.

Traders and analysts often monitor the 50-day and 200-day simple moving averages (SMAs) to identify key support and resistance levels, as these indicators can signal the beginning of upward or downward trends in stock prices.

DVN’s 50-Day and 200-Day Moving Averages

Source: Zacks Investment Research

Is DVN’s recent price momentum enough reason to add it to your investment portfolio? Let’s examine the underlying factors that could influence whether now is a good time to invest in DVN shares.

Key Factors Shaping Devon Energy’s Long-Term Prospects

Devon Energy maintains a strong operational footprint across major U.S. oil regions, including the Delaware Basin, Eagle Ford, Anadarko Basin, Rockies, and Powder River Basin. The company has consistently improved production rates from new wells in these areas. Enhanced operational efficiency, faster project cycles, and ongoing cost-cutting efforts have helped lower breakeven costs across its asset base.

Devon has also followed a disciplined approach to acquisitions, expanding its portfolio, increasing operational scale, and aiming to deliver greater value to shareholders. A planned all-stock merger with Coterra Energy, expected to close in mid-2026, would create a combined entity producing over 1.6 million barrels of oil equivalent per day and controlling nearly 750,000 net acres in the Delaware Basin. This merger is projected to yield $1 billion in annual pre-tax synergies by the end of 2027 through operational improvements and eliminating redundant services.

By divesting higher-cost assets and focusing on more efficient production, Devon has significantly improved its cost structure. The company continues to streamline drilling and completion costs and optimize its workforce to align with strategic goals, supporting robust operating margins.

Devon’s balanced exposure to oil, natural gas, and natural gas liquids further strengthens its portfolio, allowing it to adapt to changing market conditions and pursue high-quality resource opportunities.

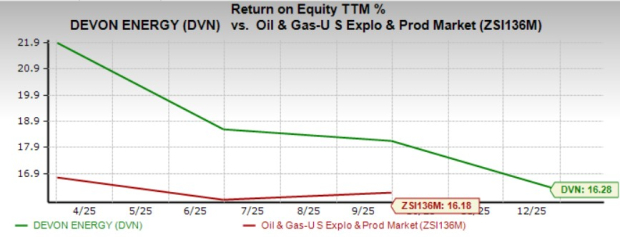

Devon Energy’s Return on Equity Surpasses Industry Average

Return on equity (ROE) is a key metric that reflects how effectively a company uses shareholders’ capital to generate profits. Over the past year, Devon’s ROE reached 16.28%, slightly above the industry average of 16.18%.

Source: Zacks Investment Research

In contrast, Occidental Petroleum (OXY), another major player in the sector, currently has an ROE of 9.89%, which is below the industry norm.

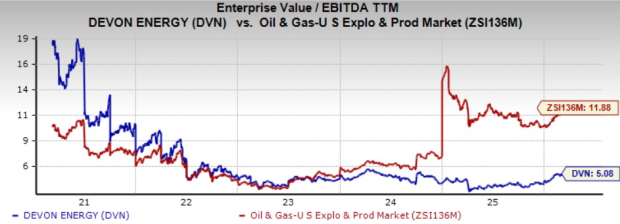

Valuation Overview for DVN Stock

Devon Energy’s shares are currently valued at a discount compared to the industry, based on the trailing 12-month Enterprise Value to EBITDA (EV/EBITDA) ratio. DVN’s EV/EBITDA stands at 5.08x, lower than the industry average of 11.88x, though slightly above its five-year median of 4.79x.

Source: Zacks Investment Research

Diamondback Energy is also trading at a discount, with an EV/EBITDA of 7.97x.

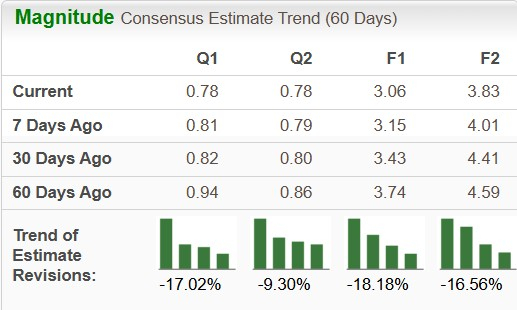

Recent Changes in DVN’s Earnings Forecasts

Over the past two months, consensus estimates for Devon Energy’s earnings per share for 2026 and 2027 have been revised downward by 18.18% and 16.56%, respectively.

Source: Zacks Investment Research

Meanwhile, Occidental Petroleum’s 2026 earnings estimate has increased by 5.79%, while its 2027 projection has decreased by 5.74% over the same period.

Conclusion

Devon Energy’s diverse asset base across multiple basins generates strong free cash flow and supports ongoing improvements to its balance sheet. Its well-diversified production mix across oil, natural gas, and NGLs enhances operational flexibility and competitive strength.

Despite recent downward revisions to earnings forecasts, DVN remains attractive due to its discounted valuation and above-average return on equity. The stock currently holds a Zacks Rank #3 (Hold), suggesting investors may consider maintaining their positions.

Further Reading and Resources

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin dip may not be over as retail ramps up buying below $70K: Santiment

CleanSpark and Bitcoin miners’ selling spree – Is the miner HODL era ending?

Bitcoin’s $70K bull-bear battle: How FOMO could tip BTC’s scales

Lantronix’s MediaTek Edge AI Venture Awaits Proof at Embedded World 2026 Challenge