AppLovin Surges 25% Over the Past Month: Is It Still a Good Time to Invest?

AppLovin Stock: Recent Performance and Outlook

AppLovin Corporation (APP) has experienced significant price swings recently. Over the past three months, the stock dropped by 26.5%, but it has rebounded with a 25% increase in the last month. This recovery hints that the company may be regaining traction after a challenging half-year period.

To determine if AppLovin remains a solid investment, it’s important to examine its technological strengths, financial results, and long-term growth prospects.

Image Source: Zacks Investment Research

Axon Technology Fuels AppLovin’s Expansion

The core of AppLovin’s growth is its Axon engine—a machine learning platform that automates ad placement, pricing, and performance optimization in real time. Unlike older ad-tech systems that depend on manual adjustments and sales experience, Axon enables advertisers to launch campaigns quickly, experiment with formats efficiently, and scale budgets with greater confidence in measurable outcomes.

The company’s self-service platform further enhances this advantage by streamlining campaign management. This not only increases spending from existing clients but also attracts new advertisers who value transparency and performance. The result is rising incremental revenue, highlighting AppLovin’s operational leverage.

Axon’s reach now extends beyond mobile gaming, with its technology gaining popularity in e-commerce advertising. This broadens AppLovin’s market potential and diversifies its revenue sources, all while maintaining stable profit margins.

Management remains optimistic about sustaining robust double-digit growth and strong EBITDA margins, indicating that Axon’s scalable platform is driving long-term success. AppLovin’s progress is now more closely tied to its platform’s economics than to the ups and downs of the advertising market.

Strategic Shift: From Gaming to AI Advertising Infrastructure

AppLovin has undergone a major transformation, moving away from its dependence on the unpredictable mobile gaming sector. This shift was solidified when CEO Adam Foroughi led the divestiture of the company’s Apps segment to Tripledot Studios in June 2025, marking a clear departure from its gaming roots.

Today, AppLovin operates as a pure-play AI advertising infrastructure provider. Its MAX mediation platform manages vast amounts of in-app ad inventory, while Axon determines optimal ad placements in real time. By replacing manual decisions with advanced algorithms, AppLovin has redefined large-scale performance advertising.

This transition to an AI-driven, self-serve model has expanded AppLovin’s market reach and made its business more resilient. With no reliance on owned gaming content, the company now leverages data intelligence for growth. While this approach carries higher risks and demands flawless execution, it positions AppLovin as a market leader setting new industry standards.

Financial Results Highlight Strong Momentum

AppLovin’s financial achievements mirror its technological advancements. In the fourth quarter of 2025, revenue soared 66% compared to the previous year, reflecting strong demand. Adjusted EBITDA surged 82% year over year, demonstrating improved efficiency, while net income jumped 84%, showing the company’s ability to convert growth into profitability. For the entire year, revenue climbed 70% and adjusted EBITDA rose 87%, underscoring AppLovin’s capacity to capitalize on market opportunities while maintaining operational discipline.

Analyst Forecasts Point to Sustained Growth

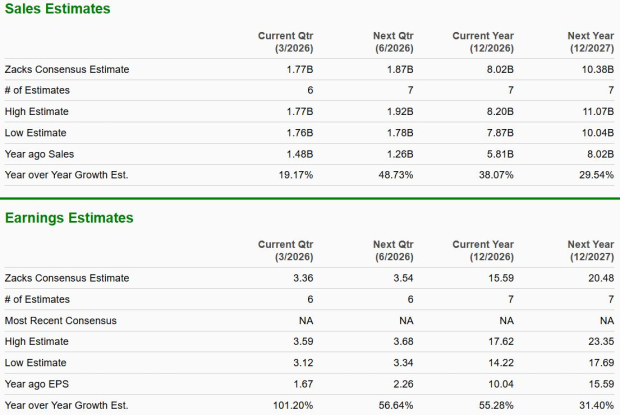

Market analysts remain upbeat about AppLovin’s future. The Zacks Consensus Estimate projects first-quarter 2026 earnings at $3.36 per share—a 101% increase from the prior year. Revenue for the same period is expected to reach $1.8 billion, up 19% year over year. For the full year 2026, earnings are anticipated to grow 55%, with another 31% increase forecasted for 2027. Revenue is expected to rise 38% in 2026 and 29.5% in 2027. These optimistic projections reflect confidence in AppLovin’s monetization strategy and its ability to deliver strong results as the digital advertising market expands.

Image Source: Zacks Investment Research

Comparing AppLovin to U.S. Competitors

- The Trade Desk (TTD): This company operates a demand-side platform specializing in programmatic advertising and excels in data-driven targeting. While The Trade Desk benefits from premium brand partnerships, its profit margins are more vulnerable to advertising market cycles than AppLovin’s. The Trade Desk focuses on reach and transparency, whereas AppLovin prioritizes performance and efficiency.

- Unity Software (U): Unity is involved in advertising through its real-time 3D and monetization tools, but its ad business is closely linked to developer ecosystems, making it more volatile. Unlike AppLovin, Unity is still working to balance growth and profitability, making AppLovin’s stable margins a notable advantage.

Valuation Concerns: Is APP Overpriced?

AppLovin’s stock currently trades at a forward price-to-earnings (P/E) ratio of 30.9, significantly higher than the industry average of 23.13. Its forward price-to-sales (P/S) ratio stands at 20.33, compared to the industry’s 2.6. These elevated multiples suggest that the market may have overly optimistic expectations for future earnings and revenue. If growth slows or guidance is less positive, the stock could face a sharp correction as valuations adjust.

Investment Recommendation: Hold for Now

Despite the recent rally, AppLovin shares appear expensive, with limited short-term upside. The high valuation increases the risk of a pullback if growth moderates or investor sentiment shifts.

Nevertheless, the company’s advanced Axon platform and expansion beyond gaming support a strong long-term growth story. Current shareholders may consider holding their positions while monitoring performance and market trends. Potential new investors might want to wait for a better entry point after possible volatility.

AppLovin currently holds a Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Robinhood’s startup fund stumbles in NYSE debut

Robinhood’s startup fund stumbles in NYSE debut

Manhattan Associates (MANH) Shares Rise, Here's the Reason

Why Bloom Energy (BE) Stock Is Dropping Sharply Today