Crocs' Profit Margins Face Challenges: Short-Term Setback or Lasting Change?

Crocs Margins: Assessing the Recent Decline

Recently, Crocs Inc. has experienced margin compression, prompting debate over whether this is a temporary setback or signals a more fundamental issue. The company's latest financials indicate that the margin pressure is primarily due to external influences and strategic decisions, rather than any inherent weakness in its core operations.

For 2025, Crocs reported an adjusted gross margin of 58.3%, a decrease of 50 basis points compared to the previous year. This reduction was mainly attributed to increased costs from tariffs, which negatively impacted margins by 130 basis points over the year. The fourth quarter mirrored this trend, with gross margin dropping 320 basis points year-over-year, largely due to a 300-basis-point hit from tariffs. Despite these external challenges, consumer demand has remained robust.

Additionally, the HEYDUDE brand contributed to margin fluctuations. As Crocs undertook wholesale inventory adjustments and increased returns and markdowns to strengthen distribution channels, HEYDUDE’s adjusted gross margin declined notably. While these measures affected short-term profitability, they are intended to lay the groundwork for healthier, more profitable growth in the future.

On a positive note, the main Crocs brand has maintained strong margin performance, with gross margins staying above 60% for the year. This resilience is supported by efficient sourcing, strong direct-to-consumer sales, and prudent inventory management.

Looking forward, Crocs’ management anticipates a gradual recovery in margins. Initiatives focused on cost reduction and supply chain improvements are expected to help offset ongoing tariff pressures. With a targeted $100 million in cost savings and continued expansion in higher-margin direct-to-consumer channels, the company is positioned to stabilize its profitability.

Overall, the recent margin decline appears to be more cyclical, driven by tariffs and brand repositioning, rather than a sign of weakening brand strength or demand.

CROX: Recent Performance and Valuation

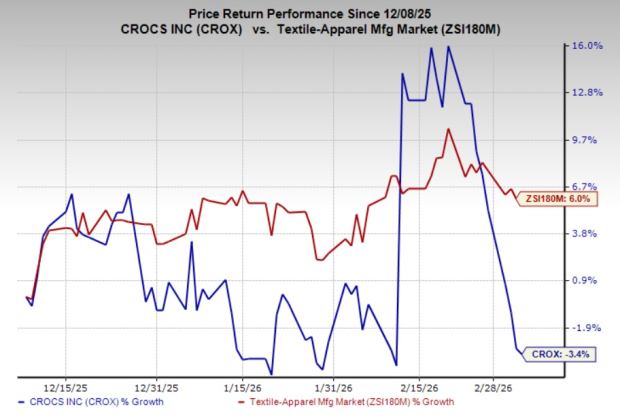

Over the past quarter, Crocs’ share price has fallen by 3.4%, while the broader textile and apparel industry has grown by 6%. Currently, CROX holds a Zacks Rank #2 (Buy), reflecting a favorable outlook.

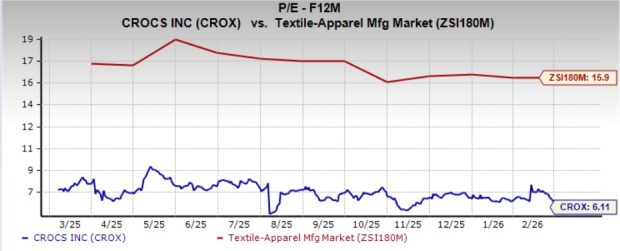

From a valuation perspective, CROX trades at a forward price-to-earnings ratio of 6.11, which is significantly below the industry average of 15.9.

The Zacks Consensus Estimates project year-over-year earnings per share growth of 7.2% for 2026 and 8.4% for 2027. Notably, consensus EPS estimates for both years have been revised upward by 7.5% and 9.5%, respectively, over the past month.

Alternative Investment Opportunities

- Columbia Sportswear Company (COLM): Specializing in outdoor and active lifestyle products, Columbia Sportswear currently holds a Zacks Rank #1 (Strong Buy). The consensus estimate points to a 2% sales increase for 2026, though earnings per share are expected to decrease by 6.2%. Over the past four quarters, the company has delivered an average earnings surprise of 25.2%.

- Vince Holding (VNCE): Vince offers a wide selection of men’s and women’s apparel, including signature cashmere, leather, and denim pieces. The company is rated Zacks Rank #1, with estimates suggesting 2.1% sales growth and a 26.3% increase in earnings for fiscal 2025. However, Vince has posted an average negative earnings surprise of 229.6% over the last four quarters.

- Ralph Lauren Corporation (RL): As a leading designer and marketer of premium lifestyle products, Ralph Lauren holds a Zacks Rank #2. Projections for fiscal 2026 indicate sales growth of 12.4% and earnings growth of 31.8%. The company has averaged a 9.7% positive earnings surprise over the past year.

Top Stock Picks from Zacks

Zacks’ research team has identified five stocks with the potential to double in value in the coming months. Among these, the Director of Research, Sheraz Mian, spotlights a lesser-known satellite communications company poised for significant growth as the space industry expands toward a trillion-dollar market. Analysts anticipate a major revenue surge for this company in 2025. While not all top picks achieve outsized gains, this one could outperform previous winners like Hims & Hers Health, which soared over 200%.

Additional Resources

For the latest stock recommendations from Zacks Investment Research, you can download the report on the 7 Best Stocks for the Next 30 Days.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Robinhood’s startup fund stumbles in NYSE debut

Manhattan Associates (MANH) Shares Rise, Here's the Reason

Why Bloom Energy (BE) Stock Is Dropping Sharply Today

Guidewire Software (GWRE) Stock Surges Dramatically, Essential Information You Should Be Aware Of