3 Reasons to Steer Clear of WFC and One Alternative Stock Worth Buying

Wells Fargo: Recent Performance and Investment Outlook

Since September 2025, Wells Fargo’s stock has remained relatively stable, delivering a modest 4.1% return and hovering near $82.37 per share.

Should you consider adding Wells Fargo to your portfolio now, or is caution warranted?

Why We’re Not Enthusiastic About Wells Fargo

We approach Wells Fargo with caution. Below are three key reasons why WFC doesn’t stand out to us, along with a stock we prefer instead.

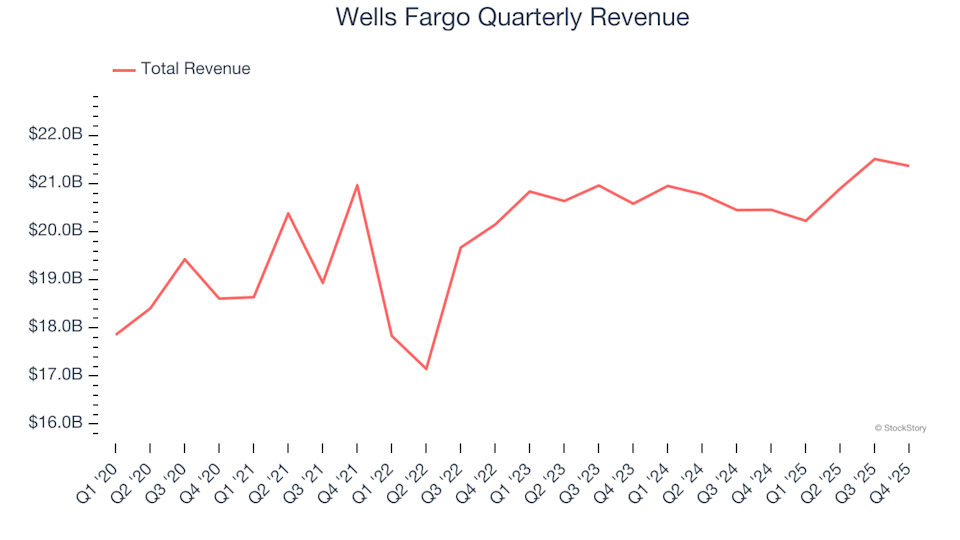

1. Underwhelming Long-Term Revenue Growth

Banks generally generate income from two main sources: net interest income (the difference between interest earned on loans, mortgages, and securities and interest paid on deposits) and non-interest income (fees from banking services, credit cards, wealth management, investment banking, and trading).

Unfortunately, Wells Fargo’s revenue has only increased at a compounded annual rate of 2.5% over the past five years, falling short of our expectations.

Wells Fargo Quarterly Revenue

2. Net Interest Income Is Declining

Net interest income is closely watched by investors because of its stability, while one-off fees are often seen as less reliable sources of revenue.

Over the last five years, Wells Fargo’s net interest income has decreased by an average of 1.5% per year, underperforming the broader banking sector. This suggests that the company’s lending business has lagged behind its other operations.

Wells Fargo Trailing 12-Month Net Interest Income

3. Shrinking Net Interest Margin

Net interest margin (NIM) measures how much a bank earns relative to its outstanding loans and is a crucial indicator of loan profitability and pricing power.

In the past two years, Wells Fargo’s average NIM was 2.7%, with a contraction of 46.7 basis points (where 100 basis points equals 1 percentage point) during that time.

This downward trend has pressured the bank’s net interest income. While changes in prevailing interest rates play a significant role, the decline may also reflect increased competition for loans and deposits or an unfavorable shift in the bank’s asset mix.

Wells Fargo Trailing 12-Month Net Interest Margin

Our Verdict

While Wells Fargo is not a poor business, it doesn’t make our list of top picks. The stock is currently valued at 1.5 times forward price-to-book (about $82.37 per share). Investors willing to take on more risk may find it appealing, but we believe there are more attractive opportunities elsewhere. We suggest considering a leading digital advertising platform benefiting from the creator economy.

Stocks We Prefer Over Wells Fargo

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to invest in a standout company is when the market begins to recognize its potential. These businesses not only have strong fundamentals but are also experiencing positive momentum right now.

Discover which stocks our AI platform is highlighting this week. Check out the current list of Strong Momentum stocks—completely free.

Our selections have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Exlservice, which delivered a 354% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Daily timeframe chart up of Nvidia

Quack AI Unveils Production-Ready Q402 on Avalanche C-Chain to Scale Agent Workflows

Samsara (IOT) Climbs 19.5% as Firm Nearing Profitability