Northern Trust Rises 12.5% Over Half a Year: Should You Buy, Hold, or Sell?

Northern Trust Corporation: Six-Month Performance Overview

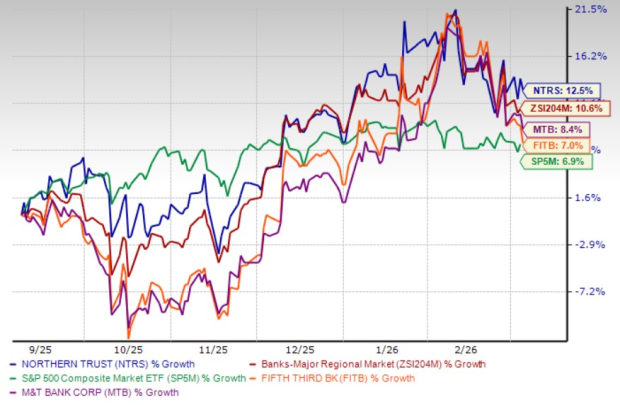

In the last half-year, Northern Trust Corporation (NTRS) shares have climbed 12.5%, outpacing both the major regional banks sector, which saw a 10.6% increase, and the S&P 500 Index, which rose 6.9%. This performance also surpasses that of competitors M&T Bank Corporation (MTB) and Fifth Third Bancorp (FITB), whose shares advanced 8.4% and 7.0%, respectively, during the same period.

Six-Month Price Performance

Image Source: Zacks Investment Research

With this notable rally, investors may wonder if Northern Trust’s stock still has upward potential or if caution is warranted. Let’s examine the key drivers behind its recent momentum.

Key Factors Fueling NTRS’s Growth

Advancements in Digital Innovation

Northern Trust has recently made strides in the digital assets space, introducing a tokenized share class for its NIF Treasury Instruments Portfolio through its asset management division, Northern Trust Asset Management (NTAM), as of March 2, 2026. This blockchain-based solution, initially available via BNY’s LiquidityDirect platform and Goldman Sachs’ Digital Asset Platform, aims to streamline settlement processes and enhance transparency for investors. This marks NTAM’s first foray into tokenized investment offerings.

By embracing blockchain technology, Northern Trust seeks to modernize its liquidity solutions, boost operational efficiency, and position itself to benefit from the increasing institutional adoption of digital asset infrastructure.

Wealth Management Expansion

The company continues to broaden its wealth management services, targeting growth in lending as its client roster—especially among ultra-high-net-worth individuals and family offices—expands. Recent initiatives include technology upgrades and strategic partnerships to improve client experience and distribution. In January 2026, Northern Trust teamed up with Envestnet to provide direct indexing solutions, enabling advisors to deliver tailored, tax-efficient portfolios to affluent clients. Earlier, in April 2025, NTAM launched Family Office Solutions, offering institutional-level services to UHNW families without the need for a dedicated family office.

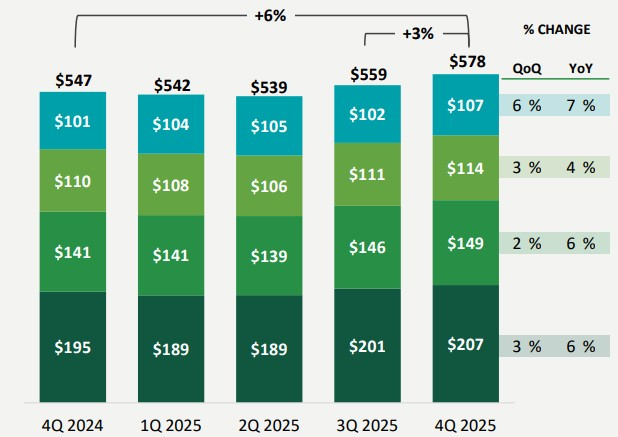

Further strengthening its advisory capabilities, Northern Trust acquired Parilux Investment Technology in May 2021, enhancing its Front Office Solutions platform. Reflecting the success of these efforts, wealth management trust, investment, and other servicing fees increased 5.7% year-over-year to $577.8 million in Q4 2025. These developments are expected to reinforce the company’s wealth management franchise, boost client assets, and drive growth in both lending and fee-based revenue streams.

Wealth Management Fees Trend

Image Source: Northern Trust Corporation

Consistent Organic Growth

Northern Trust has maintained steady organic growth, with both revenue and lending activities on the rise. From 2020 to 2025, the company’s revenues achieved a compound annual growth rate (CAGR) of 5.7%, fueled by increases in net interest income and non-interest income, despite some annual fluctuations. Over the same period, loan and lease balances grew at a CAGR of 4.2%, indicating stable demand across its lending operations.

Revenue Growth Pattern

Image Source: Zacks Investment Research

Looking ahead, loan growth is expected to benefit from a growing client base, particularly as the wealth management division attracts new customers. The Federal Reserve’s three rate cuts in 2025, which lowered the federal funds rate to between 3.50% and 3.75%, along with the possibility of further reductions in 2026, are likely to reduce borrowing costs and stimulate loan demand, supporting Northern Trust’s lending expansion.

Enhancing Operating Leverage

The company has implemented several cost-control measures to improve operating leverage, including careful management of staffing levels, vendor consolidation, optimizing its real estate footprint, and increasing process automation. These initiatives have already yielded positive results: in Q4 2025, Northern Trust achieved its sixth consecutive quarter of positive operating leverage and reported a return on equity (ROE) of 15.4%, surpassing its long-term target range of 10–15%. Ongoing cost discipline and efficiency improvements are expected to sustain profitability in the future.

Robust Liquidity and Capital Distribution

Northern Trust maintains a strong liquidity position, supporting both its financial obligations and capital deployment. As of December 31, 2025, the company held $53.4 billion in deposits with the Federal Reserve and other central banks, far exceeding its total debt of $10.6 billion.

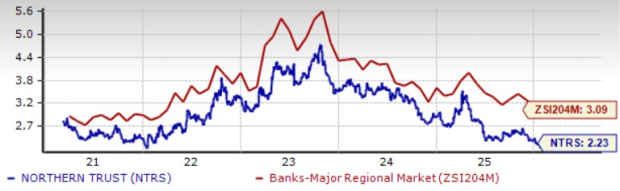

This liquidity strength enables consistent capital returns to shareholders. After passing the Federal Reserve’s 2025 stress test, Northern Trust raised its quarterly dividend by 6.7% to $0.80 per share. Over the past five years, the dividend has been increased twice, resulting in an annualized growth rate of 2.5%, with a current yield of 2.23%. For comparison, Fifth Third and M&T Bank offer yields of 3.23% and 2.74%, respectively.

Dividend Yield Comparison

Image Source: Zacks Investment Research

In addition to dividends, Northern Trust has an ongoing share repurchase program. Announced in October 2021, the plan authorizes the buyback of up to 25 million shares with no set expiration. As of the end of 2025, 1.9 million shares remained available for repurchase, and management intends to continue this activity at a similar pace in the near term. This disciplined approach to capital management should help maintain the company’s capital-return initiatives.

Is Now the Time to Invest in NTRS?

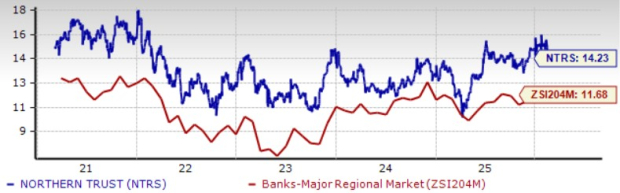

Currently, Northern Trust’s stock trades at a trailing 12-month price-to-earnings (P/E) ratio of 14.23, which is higher than the industry average of 11.68. Fifth Third and M&T Bank have P/E ratios of 11.71 and 11.27, respectively.

Price-to-Earnings Ratio (Forward 12 Months)

Image Source: Zacks Investment Research

Although the stock’s premium valuation and rising expenses may prompt some caution, these concerns are mitigated by Northern Trust’s solid liquidity, expanding wealth management operations, and improved operating leverage.

Additionally, analyst forecasts for 2026 and 2027 earnings have been revised upward in the past month, with projected growth rates of 10.1% and 9.4%, respectively, signaling continued confidence in the company’s earnings outlook.

Analyst Estimate Revisions

Image Source: Zacks Investment Research

Conclusion: Northern Trust’s Investment Appeal

Overall, Northern Trust presents an attractive option for investors seeking a well-managed custody bank with robust wealth management capabilities, improving profitability, and a consistent track record of returning capital to shareholders.

The stock currently holds a Zacks Rank #2 (Buy).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Robinhood’s startup fund stumbles in NYSE debut

Manhattan Associates (MANH) Shares Rise, Here's the Reason

Why Bloom Energy (BE) Stock Is Dropping Sharply Today

Guidewire Software (GWRE) Stock Surges Dramatically, Essential Information You Should Be Aware Of