Block Gains 23.6% Post Q4 Earnings: Buy, Hold or Fold the Stock?

Block XYZ shares gained 23.6% following an impressive fourth-quarter 2025 results announcement on Feb. 26, 2026, through yesterday’s closing session. The company also raised its full-year 2026 outlook.

Block is reducing its workforce, from over 10,000 to under 6,000 employees, letting go of more than 4,000 people. The company highlighted that this step was taken to leverage advancing AI and intelligence tools that enable smaller teams to perform more efficiently and effectively.

Given the solid results and increased outlook, we intentionally waited before publishing our review to gauge whether price movements might reveal deeper sentiment trends.

Let’s delve deeper and find out.

Key Highlights of XYZ’s Q4 Earnings Release

On paper, Block reported strong growth in the fourth quarter of 2025. The company’s net revenues came in at $6.25 billion, rising 3.6% year over year. Adjusted earnings per share (EPS) were 65 cents, reflecting a 38.3% year-over-year increase. The company has realigned its revenue and related costs of revenues across three categories to reflect its evolution, namely, Commerce Enablement, Financial Solutions and Bitcoin Ecosystem.

In the quarter, gross profit increased 24.3% year over year to $2.87 billion. Cash App, the crown jewel of Block’s ecosystem, posted $1.83 billion in gross profit, up 33.1% year over year, driven by growth across Cash App Borrow, BNPL products and Cash App Card. Square reported a 7.5% gross profit increase to $992.7 million, driven primarily by Financial Solutions, most notably Square Loans. Adjusted operating income surged 46.3% to $587.8 million, delivering 300 basis points of margin expansion to 20% on a year-over-year basis, even as the company invested in initiatives with strong ROIs that it expects to drive future growth.

Block repurchased $790 million of shares in the fourth quarter, bringing its total for 2025 to $2.3 billion. The company exceeded the Rule of 40 in the fourth quarter of 2025 and believes it is on track to sustain it annually moving forward. It continued launching new products and investing in go-to-market efforts across Square and Cash App to sustain strong growth at scale.

What’s Driving Block Stock's Performance?

The biggest driver behind Block’s momentum is Cash App, which has evolved into far more than a peer-to-peer payments platform. It now functions as a multi-service financial hub, particularly for younger, digitally native consumers. With products spanning payments, banking, commerce and Bitcoin transactions, Cash App is broadening its role in users’ financial lives.

In the fourth quarter of 2025, Cash App monthly actives grew to 59 million from 58 million in the prior quarter. While monthly actives may fluctuate from time to time, the company continues to expect low single-digit actives growth in 2026 and over the long term. The company continues to invest in Cash App Green as a cornerstone of its engagement strategy.

Meanwhile, Square, which is Block’s merchant-facing ecosystem, remains solid. Double-digit growth in gross payment volume (GPV) alongside innovations like Square AI, Square Handheld and next-gen Square Point of Sale software highlights the company’s efforts to keep Square competitive in the evolving point-of-sale and software landscape. In addition, the company now partners with 100 independent sales organizations, complementing its direct sales motion and extending its reach to more new sellers.

Block raised its full-year 2026 guidance to reflect the strength across the business. The company now expects to deliver gross profit of $12.20 billion, indicating 18% growth in 2026 compared with 17% growth shared at Investor Day. It expects adjusted operating income to be $3.20 billion, with an operating margin of 26%. At Investor Day, it was expected to be $2.70 billion. In 2026, it expects to deliver adjusted EPS growth of 54% year over year to $3.66 compared with the prior outlook of $3.20.

XYZ’s Challenges: Competition, Volatility and Concentration

Despite its strengths, Block faces material headwinds. Competition in digital payments is intensifying. PayPal Holdings, Inc. PYPL continues to command stronger merchant acceptance globally, while Apple Pay and other wallet providers are expanding their reach. In consumer finance, established banks and emerging fintechs are vying for the same demographics that Block targets. Bitcoin remains a meaningful part of Block’s strategy, but it adds volatility.

Block remains highly concentrated in the U.S. market and heavily reliant on a younger demographic base through Cash App. While this has fueled strong growth to date, geographic and demographic concentration may limit long-term resilience compared with more globally diversified peers.

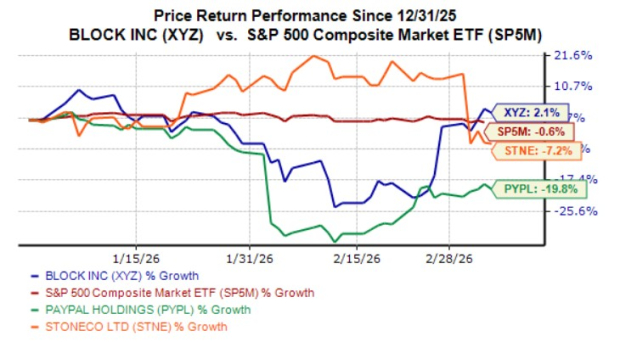

XYZ Stock Price Performance

XYZ stock has not only outpaced its peers, such as PYPL and StoneCo Ltd. STNE, but outperformed the S&P 500 composite in the year-to-date period. PayPal and StoneCo shares have declined 19.8% and 7.2%, respectively, over the same time frame.

Image Source: Zacks Investment Research

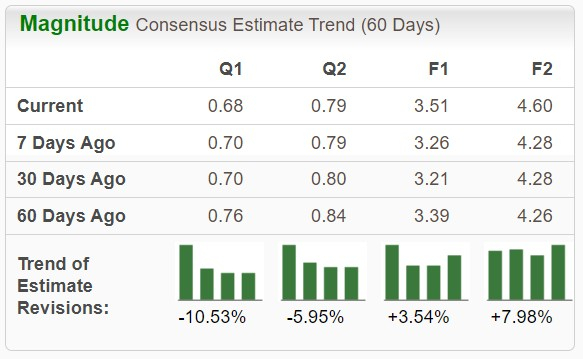

XYZ’s Earnings Estimate Revision Trends Upward

The Zacks Consensus Estimate for Block’s 2026 sales calls for a year-over-year rise of 11%, while that for EPS suggests a 48.1% increase year over year. EPS estimates have been trending upward by 25 cents to $3.51 per share over the past week.

Image Source: Zacks Investment Research

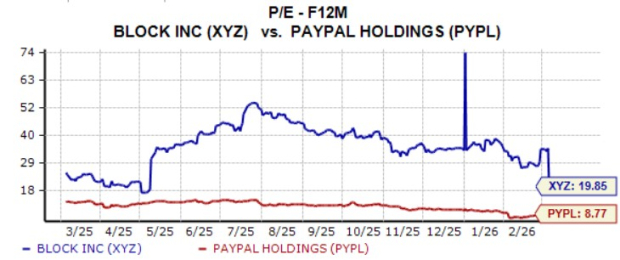

XYZ Shares Trade at a Premium

Block shares are overvalued, as suggested by the Value Score of C. In terms of forward 12-month Price/Earnings (P/E), Block is trading at 19.85X, which is at a premium to PayPal’s 8.77X.

Image Source: Zacks Investment Research

Final Take on Block

Block continues strengthening its position as a leading fintech innovator through its expanding Square and Cash App ecosystems. Innovations across Square and Cash App highlight the company’s strong execution and growing ecosystem.

While competition, demographic concentration and premium valuation raise caution, Block’s diversified revenue base, user growth strategies and continued momentum justify holding the stock. For now, maintaining a position in XYZ seems prudent as it navigates challenges while unlocking new growth avenues.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Groupon (GRPN) Dipped More Than Broader Market Today

Bitcoin Hyper News: Pepeto Stalls as DeepSnitch AI’s March 31 Launch Fuels 1000x Talk

AGNC Investment (AGNC) Falls Further Than the Overall Market: Key Insights for Shareholders