3 Reasons Why RTX Carries Risks and One Alternative Stock Worth Considering

RTX’s Performance Outpaces the Market

Since March 2021, the S&P 500 has returned 79.5%. However, RTX has significantly outperformed, climbing 170% over the past five years to reach $204.06 per share. The stock’s upward trend continues, gaining 32.3% in the last half-year, driven by strong quarterly earnings and surpassing the S&P 500 by 26.7%.

Is RTX a smart addition to your portfolio right now, or should you approach with caution?

Why We’re Not Enthusiastic About RTX

While RTX’s price appreciation has benefited shareholders, we remain cautious. Below are three reasons we’re steering clear of RTX—and a stock we prefer instead.

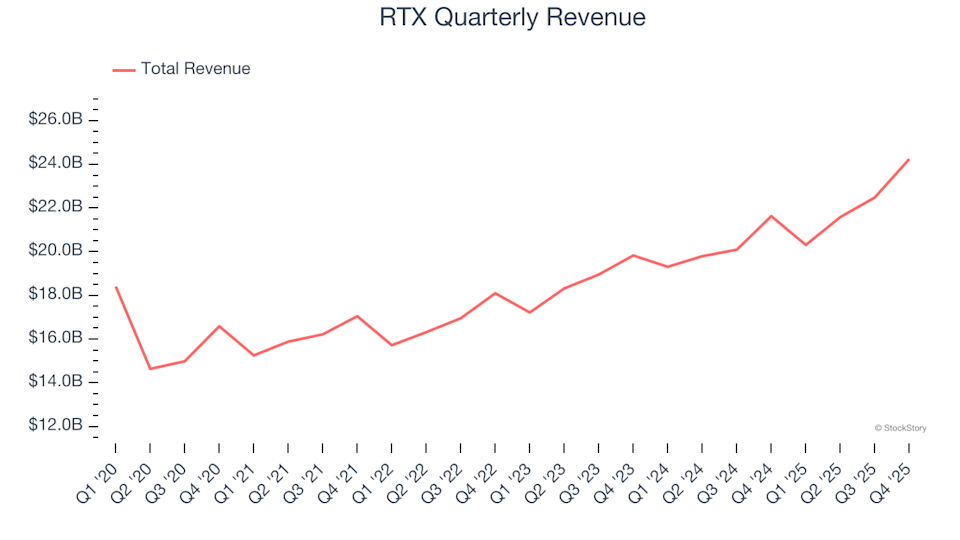

1. Long-Term Revenue Growth Lags

Evaluating a company’s long-term track record reveals its true strength. While any business can post strong results for a quarter or two, sustainable growth over years is what matters. RTX’s annualized revenue growth of 6.5% over the past five years is underwhelming and falls short of our expectations for the industrial sector.

RTX Quarterly Revenue

2. Modest Revenue Growth Outlook

Wall Street’s revenue forecasts offer a glimpse into a company’s future prospects. While predictions aren’t always precise, accelerating growth tends to lift valuations and share prices, whereas slowing growth can have the opposite effect.

Analysts anticipate RTX’s revenue will increase by just 5.6% over the next year—a slowdown compared to its 6.5% annualized growth over the past five years. This tepid outlook suggests RTX may face headwinds in demand for its offerings.

3. Growth Investments Have Underperformed

Growth is important, but how efficiently a company invests for that growth matters even more. Return on Invested Capital (ROIC) measures how much operating profit a business generates relative to the capital it has raised through debt and equity.

RTX’s five-year average ROIC stands at 4.5%, which is below the typical cost of capital for industrial companies. This indicates that RTX’s investments in growth have not delivered strong returns.

RTX Trailing 12-Month Return On Invested Capital

Our Verdict

RTX is not a poor business, but it doesn’t make our list of top picks. Despite its recent market-beating performance, the stock trades at a forward P/E of 30.6 (or $204.06 per share). Investors willing to take on more risk may find RTX appealing, but we believe there are more attractive opportunities available. We suggest considering instead.

Stocks We Prefer Over RTX

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The optimal time to invest in a great company is when the market starts to recognize its potential. These businesses not only have strong fundamentals but are also experiencing significant momentum right now—making them stand out.

Want to know which stocks our AI platform is highlighting this week? Discover this week’s Strong Momentum stocks for free.

Our list features well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Kadant, which delivered a 351% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Canadian Pacific Shares Drop 2.7% After $1.2 Billion Debt Issuance Ranks 503rd in Daily Trading Volume

Gold price to accelerate and hit new record highs after this event – technical analyst

Chevron at $190: Is This an Energy Sector Rotation or a Broader Market Revaluation?