First Bancorp (FBNC): Should You Buy, Sell, or Hold After Q3 Results?

First Bancorp: Limited Growth and Lukewarm Performance

Currently, First Bancorp is trading at $57.53 per share and has delivered a modest 3.9% return over the past half-year, showing little momentum.

Should you consider adding First Bancorp to your portfolio, or is caution warranted?

Why We’re Not Enthusiastic About First Bancorp

At this time, we’re not recommending First Bancorp. Below are three reasons why we believe there are more attractive investment options than FBNC, along with a stock we prefer.

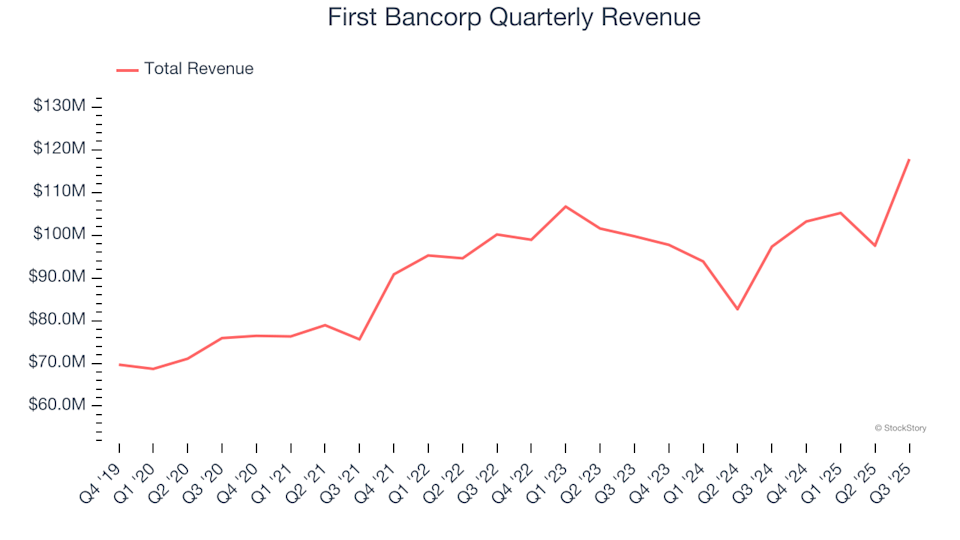

1. Underwhelming Revenue Expansion

For banks, net interest income and fee-based revenue are the main drivers of earnings. Net interest income reflects the profit from the difference between lending rates and deposit costs, while fee-based revenue includes charges for banking services, credit products, wealth management, and trading.

First Bancorp’s revenue has grown at an average annual rate of just 8.2% over the past five years, which falls short of our expectations for the sector.

First Bancorp Quarterly Revenue

2. Weak Net Interest Margin Signals Low Profitability

The net interest margin (NIM) is a key indicator of a bank’s profitability, measuring the difference between interest earned and interest paid. It reveals how effectively a bank generates returns from its lending activities.

Over the last two years, First Bancorp’s average NIM was a lackluster 3.1%, suggesting high servicing and capital costs are weighing on profitability.

First Bancorp Trailing 12-Month Net Interest Margin

3. Earnings Per Share Growth Remains Tepid

We monitor long-term changes in earnings per share (EPS) to assess whether a company’s growth is translating into real profits.

First Bancorp’s EPS has increased at an annual rate of just 6.5% over the past five years, mirroring its slow revenue growth. This indicates the company has maintained, but not meaningfully improved, its profitability per share as it has grown.

First Bancorp Trailing 12-Month EPS (Non-GAAP)

Our Verdict

While First Bancorp is not a poor-quality company, it does not meet our standards for excellence. The stock is currently valued at 1.5 times forward price-to-book (or $57.53 per share). Investors willing to take on more risk may find it appealing, but we believe the downside outweighs the potential rewards. There are more compelling opportunities in the market right now. For example, consider one of our top digital advertising picks.

Top Stocks for Any Market Environment

Don’t Miss: Our Top 5 Growth Stocks. The biggest winners in the stock market often share one trait: explosive revenue growth. Companies like Meta, CrowdStrike, and Broadcom were all identified early by our AI, delivering returns of 315%, 314%, and 455%, respectively.

Discover which five stocks our system is highlighting this month—absolutely free.

Our list features well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Exlservice, which delivered a 354% five-year return. Find your next potential winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

BillionToOne Crumbles as Bearish Signals Dominate

A whale repurchased 1,733 XAUTs for 8.9 million USDC.

3 Discounted AI Infrastructure Stocks

Two-Fold Economic Risks Become Apparent