3 Reasons to Steer Clear

Energy Recovery Stock: Recent Performance and Investor Outlook

Over the last half-year, Energy Recovery's share price has dropped by 26.3%, now sitting at $10.75 per share. This decline follows weaker-than-expected quarterly earnings, leaving many investors reconsidering their positions.

Should you consider buying Energy Recovery at these levels, or does it pose too much risk for your portfolio?

Why We’re Not Enthusiastic About Energy Recovery

Even though the stock is more affordable now, our confidence in Energy Recovery remains low. Below are three key reasons we’re steering clear of ERII, along with a stock we prefer instead.

1. Weak Long-Term Revenue Growth

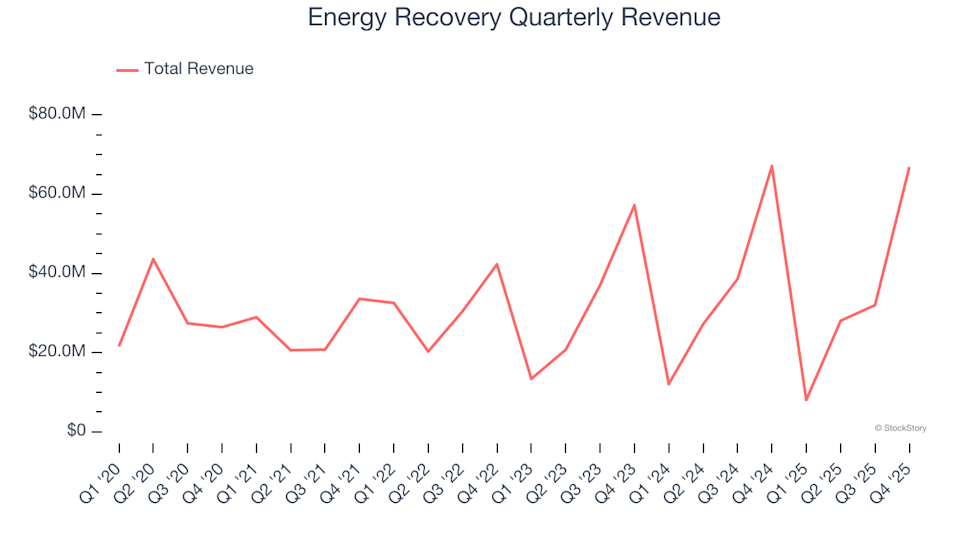

Consistent, long-term expansion is a hallmark of a strong business. While any company can have a good year, the best ones deliver steady growth over time. In the past five years, Energy Recovery’s sales have only increased at a modest 2.6% compound annual rate—falling short of our expectations.

Energy Recovery Quarterly Revenue

2. Unfavorable Revenue Forecasts

Analyst projections offer insight into a company’s future prospects. While forecasts aren’t always perfect, accelerating growth tends to lift valuations and share prices, whereas slowing growth can have the opposite effect.

Looking ahead, analysts anticipate Energy Recovery’s revenue will decline by 10.3% over the next year—a sharp reversal from its previous five-year annualized growth. This outlook suggests the company may face challenges in maintaining demand for its offerings.

3. Declining Returns on New Investments

Return on invested capital (ROIC) measures how efficiently a company generates profit from its capital base. We favor businesses with strong and improving ROIC, as positive trends often drive stock performance.

Unfortunately, Energy Recovery’s ROIC has trended downward in recent years. While management has made solid decisions in the past, the falling returns could indicate a lack of lucrative growth opportunities going forward.

Energy Recovery Trailing 12-Month Return On Invested Capital

Our Verdict

While Energy Recovery is not a poor company, it doesn’t make our list of top picks. After its recent drop, the stock trades at a forward P/E of 17.2 (or $10.75 per share), which is a fair valuation. However, the company’s weakening fundamentals introduce significant downside risk. We believe there are more promising opportunities available right now. For example, consider one of our top digital advertising recommendations.

Alternative Stocks Worth Considering

Don’t Miss: Top 5 Momentum Stocks. The ideal time to invest in a standout stock is when the market starts to recognize its potential. These companies not only have strong fundamentals, but are also experiencing significant momentum right now—making them especially attractive.

Discover which stocks our AI-powered platform is highlighting this week. Check out the latest Strong Momentum stocks—completely free.

Our list features well-known names like Nvidia (up 1,326% from June 2020 to June 2025) as well as lesser-known companies such as Exlservice, which delivered a 354% return over five years. Find your next breakout stock with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

BillionToOne Crumbles as Bearish Signals Dominate

A whale repurchased 1,733 XAUTs for 8.9 million USDC.

3 Discounted AI Infrastructure Stocks

Two-Fold Economic Risks Become Apparent