3 Compelling Arguments to Let Go of NSC and One Alternative Stock Worth Buying

Norfolk Southern’s Recent Performance and Investor Considerations

Over the last half-year, Norfolk Southern has outperformed the S&P 500 by 7.5%, with its stock price climbing to $311.61—a 13.1% increase. This upward momentum has been fueled in part by strong quarterly earnings, prompting investors to consider their next steps.

Is Norfolk Southern currently a smart addition to your portfolio, or could it introduce unnecessary risk?

Reasons for Caution with Norfolk Southern

Despite recent gains, we remain cautious about Norfolk Southern’s future prospects. Below are three key concerns, along with an alternative stock we find more appealing.

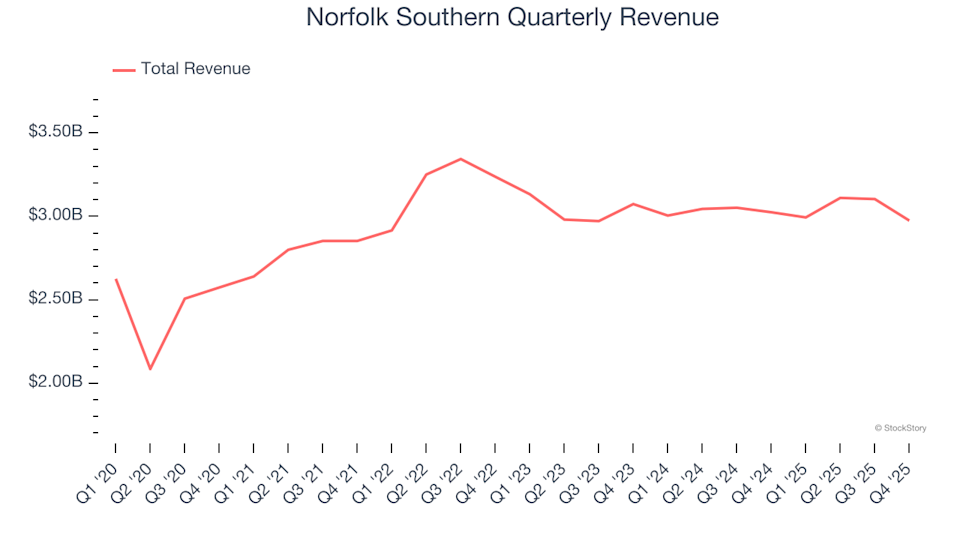

1. Underwhelming Long-Term Revenue Growth

Consistent, long-term sales growth is a hallmark of high-quality companies. While any business can post strong results in the short term, sustained expansion is more telling. Over the past five years, Norfolk Southern’s revenue has grown at a modest 4.5% annual rate, falling short of what we expect from leading industrial firms.

Norfolk Southern Quarterly Revenue

2. Declining Operating Margin

Operating margin reflects how much profit remains after covering core business expenses, excluding interest and taxes. This metric allows for fair profitability comparisons across companies with varying debt and tax structures.

Norfolk Southern’s operating margin has dropped by 4.1 percentage points over the last five years. This decline is concerning, as stronger revenue growth should have improved cost efficiency and profitability. Currently, the company’s operating margin for the past year stands at 35.8%.

Norfolk Southern Trailing 12-Month Operating Margin (GAAP)

3. Falling Free Cash Flow Margin

We place a strong emphasis on free cash flow, as it represents the actual cash available to meet obligations—unlike accounting profits. Over the past five years, Norfolk Southern’s free cash flow margin has decreased by 8.4 percentage points. If this trend persists, it may indicate rising capital requirements and investment needs. For the last twelve months, the free cash flow margin was 18.1%.

Norfolk Southern Trailing 12-Month Free Cash Flow Margin

Our Verdict

While we appreciate companies that strive to improve customer experiences, we’re taking a cautious stance on Norfolk Southern. The stock is currently trading at a forward P/E of 26.3 (or $311.61 per share), suggesting that much optimism is already reflected in the price. We believe there are more attractive opportunities available. Consider exploring as an alternative.

Stocks We Prefer Over Norfolk Southern

One More Thing: Our Top 6 Stock Picks for This Week

The current market is quickly distinguishing high-quality stocks from overpriced ones, with AI-driven shifts impacting entire sectors. In such a dynamic environment, having more than just a list of good companies is essential.

Our AI-powered system identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rally, and Nvidia prior to its 1,178% climb. Each week, it highlights six new stocks that meet these rigorous criteria.

Our recommendations have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Kadant, which delivered a 351% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Solana Price Drop Pushes SOL Below $85

+157 Billion in 24 Hours: Shiba Inu (SHIB) Inflow Wave Ends Rally Expectations

Altcoins Eye 2x–4x Gains as PMI Turns Positive — 4 High-Momentum Trades to Watch

Bitcoin Mining Giants Ramp Up Sales as Prices Drop Sharply