Goldman Sachs "tears up report": If the Strait of Hormuz does not "resume as scheduled" in the next few days, oil prices face rapidly expanding "significant upside risk"

On March 7, according to news from Chasing Wind Trading Desk, the Goldman Sachs Commodities Research team quietly "overturned" its previous optimistic expectations in its latest oil report on March 6 — the bank’s previous baseline scenario was based on the assumption that the Hormuz Strait flow would "gradually begin to normalize in the coming days."

As previously referenced byWallstreet Insights, Goldman Sachs Chief Oil Strategist Daan Struyven expected in his March 4 report that the blocked crude transportation via the Hormuz Strait would remain at the currently suppressed level for the next five days, recover to 70% of normal within the following two weeks, and reach 100% full normalization in four weeks. However, the latest data shows that reality is much more severe than expected.

Goldman Sachs makes it clear in the latest research report:If there is no sign of strait flow normalization in the coming days, oil price forecasts will be immediately revised. More importantly, the report points out thatupside risks are "rapidly widening", and gives a direct price judgment in extreme scenarios:

If there is no sign of resolution this week, oil prices are very likely to break through $100 next week; if flows stay depressed through March, oil prices (especially refined products) will surpass the historical highs of 2008 and 2022.

The research points out that upside risks for energy assets are accumulating at an unprecedented speed, and the four major reasons provided by Goldman Sachs are successively undermining the logic behind the "quick recovery" hypothesis.

Reason 1: Drop in strait flow far exceeds expectations, reality is worse than assumptions

Goldman Sachs estimates normal oil flow through the Hormuz Strait at approximately20 million barrels per day (20mb/d), including about 14mb/d of crude oil and condensates, 4mb/d of refined products, and 2mb/d of liquefied natural gas (NGL).

The current actual data is striking:Average daily strait flow has already dropped about 90% below normal, which is a reduction of roughly 18mb/d..

This figure is even below the "85% drop (about 15% of normal flow)" baseline in this week's Goldman Sachs assumptions. In other words, the reality is even worse than Goldman Sachs' pessimistic estimate. This means that the risk around the baseline scenario is now skewed towards "lower flows, for a longer duration."

Reason 2: Alternative pipeline rerouting capacity is severely insufficient, actual rerouting only 0.9mb/d

In the face of the strait closure, the market had hopes that pipelines and alternative ports would fill the gap. Theoretically, Saudi Arabia’s east-west pipeline (to Red Sea Yanbu Port) and the UAE's Habshan–Fujairah pipeline (to the Gulf of Oman) have a combined estimated spare capacity of less than4mb/d (3.6mb/d).

However, real-time Goldman Sachs tracking shows that in the past four days, net rerouted flows via pipelines and Yanbu (Red Sea, Saudi Arabia) and Fujairah (Gulf of Oman, UAE) haveonly increased by about 0.9mb/d, far less than the theoretical limit.

The reasons for this significant gap are multiple:

This week's attack on Fujairah port and oil storage facilities directly undermined alternative export capacity;

Local shortage of marine fuel (generally imported from the Persian Gulf via Hormuz Strait), causing tankers to be unable to operate normally;

Previous attacks on pipelines further constrained rerouting potential.

This means that market expectations of "pipelines as backstop" were gravely overestimated and the actual buffer capacity is extremely limited.

Reason 3: A rapid resolution is not necessarily imminent, shippers remain on the sidelines

Through communication with market participants, Goldman Sachs found thatmost shipowners are currently in "wait and see" mode, with the fundamental reason being extremely high physical risk in the strait.

Notably, Goldman Sachs’ analysis rules out "insurance costs" as the main cause of the sharp flow drop. Data shows there is still some insurance available, and purely economically, transiting the strait remains profitable for shippers under surging freight rates — even though war risk premiums have surged (currently about 3%, with the historical high being 7.5% during the Iran-Iraq war in the 1980s).

This points to a more worrying conclusion:the core factor stopping ship passage is physical security risk, not economic cost. As long as the physical risks persist, economic incentives alone are not enough to restore flows.

Goldman Sachs lists three possible paths to strait flow recovery:

- Overall de-escalation of conflict

(comprehensive ceasefire or diplomatic resolution);- The US provides powerful escort protection for tankers

;- Iran allows safe passage for tankers of certain origins/destinations (including China)

.

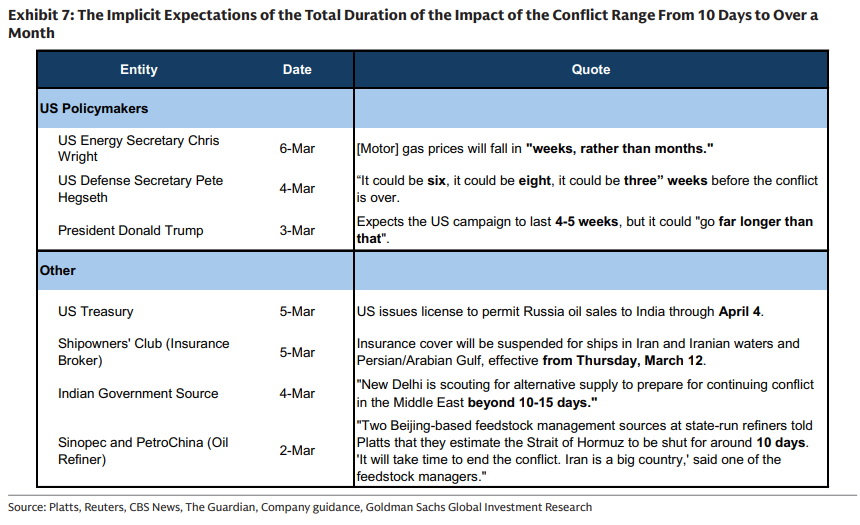

Judging from various statements (see table below), expectations for the conflict’s duration range from 10 days to over a month, with large divergences, further increasing market uncertainty:

Reason 4: Supply shock is unprecedented, demand destruction pricing will come sooner than ever

Goldman Sachs emphasizes that the scale of this supply shock has no precedent in history.

The total shock to Persian Gulf oil supply has reached 17.1mb/d — a figure17 times the peak drop in Russian output in April 2022. At the same time, total Persian Gulf oil exports aredown 74% from normal, leaving only about 6mb/d.

Goldman Sachs notes that, due to the unprecedented scale, the market will start to price in "demand destruction" faster than historic experience and simple models suggest, for two main reasons:

- Stock drawdown is happening extremely fast

: the larger the shock, the sooner the market will start to price in demand destruction, even while inventory is relatively high, rather than wait for inventory to be truly depleted;- Accelerating factors add up

: consumer hoarding behavior, as well as non-OECD countries cutting refined product exports (such as China reducing exports to ensure domestic supply), will further accelerate OECD inventory drawdown.

The essence of Goldman Sachs’ "tearing up the report": The baseline assumption is being shredded by reality

The key to understanding this report is to compare it with Goldman Sachs’ earlier optimistic expectations.

As referenced byWallstreet Insights, previously, the Goldman Sachs strategy team turned bullish against the backdrop of market turbulence, regarding the downturn as a buying opportunity, with one key supporting logic being the optimistic assumption that Hormuz Strait flows would "normalize within four weeks." Chief Oil Strategist Daan Struyven previously set the path as:strait flow maintains about 15% of normal for another five days, recovers to 70% in two weeks, and normalizes to 100% after another two weeks.

Based on this, Goldman's forecast for Brent crude average price in Q2 was raised to $76/barrel, WTI to $71/barrel, and Brent's Q4 2026 forecast from $60 to $66.

However, this March 6 report is actually Goldman Sachs openly questioning its own assumptions with the latest data:

Goldman Sachs clearly states,if there is no evidence of gradual normalization of strait flows in the coming days, oil price forecasts will soon be revised. This is in fact a warning to the market: a more aggressive upward revision may come at any moment.

However, Goldman Sachs also indicated in previous reports that if the US escort plan or diplomatic efforts succeed and strait flows recover rapidly, the current risk premium could quickly evaporate, and Brent oil prices may face asharp drop of $12–15 per barrel.

According to the research, so far, 12 tankers have been attacked in and near the Hormuz Strait (from March 1 to 6), and thus far, there have been no confirmed attacks on Asia-flagged tankers—this detail could be an important variable influencing future developments.

~~~~~~~~~~~~~~~~~~~~~~~~

For more detailed interpretations, including live interpretations and frontline research, please join the [Chasing Wind Trading Desk ▪ Annual Membership]

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Pundit Describes How $10,000 In XRP Could Become $1,000,000

Nvidia Releases Financial Results. Investors on Wall Street Respond, "Is That All?"

Patrick Bet-David’s Bombshell XRP Price Forecast if XRP Captures 5% of SWIFT Volume

The new American AI restrictions cause Nvidia stock to plunge