US Treasury Bonds: The Tree Wants to Remain Still, but the Wind Won't Stop

On one hand, oil prices are soaring, while on the other, the job market appears weak. This is the scenario the Federal Reserve least wants to see, and it has arrived.

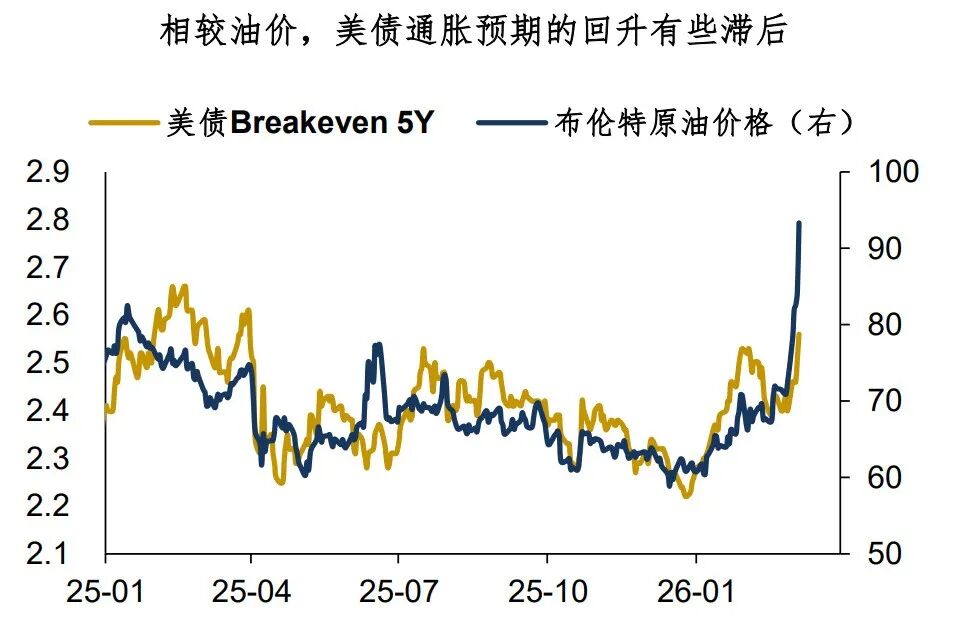

Since early March, the 10Y US Treasury yield has risen by 20 basis points from its low. However, compared with the explosive surge in oil prices, this increase in yields is insignificant. The chart below shows that US Treasury inflation expectations (Breakeven) have been slow to pick up, with their upward movement not matching oil prices.

Why haven’t US Treasuries fully reflected the impact of rising oil prices? In my opinion, there are two main reasons:

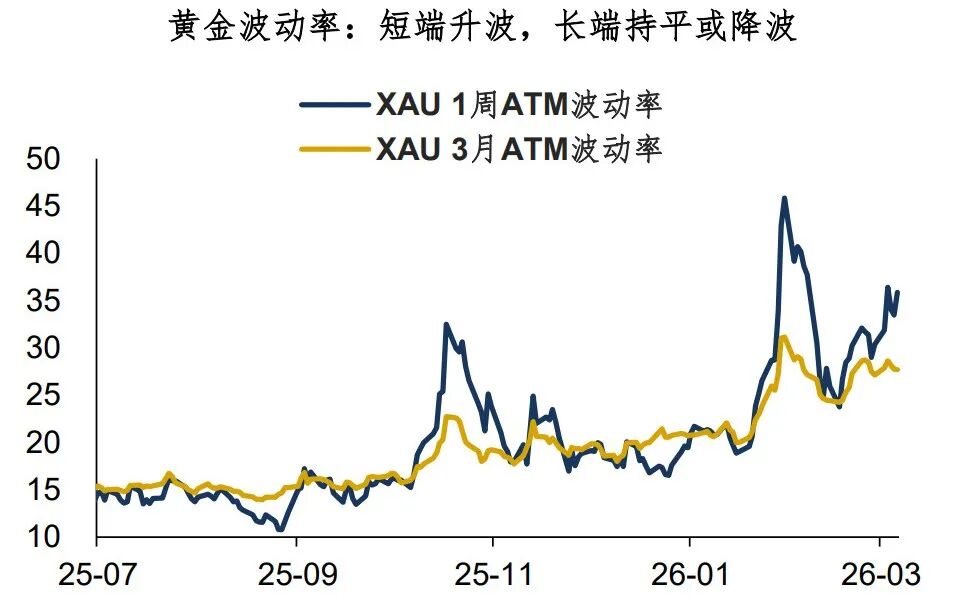

First, the market believes the US-Iran conflict and oil price spike are short-term and will eventually revert.There is evidence for this expectation. Take gold, a typical liquidity-sensitive asset: its entire volatility curve is distorted. Short-term (1W) volatility continues to rise, while medium-to-long term (3M) barely changes or even declines.US Treasury pricing is similar—markets see the US-Iran conflict as temporary.

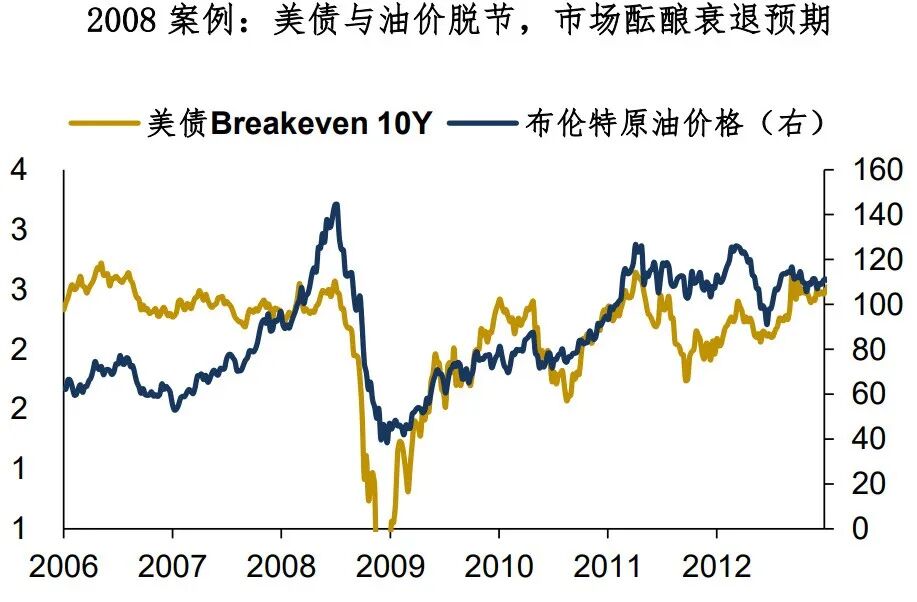

Second, the US Treasury market is starting to price in longer-term recession expectations.A similar situation occurred in 2008 when crude oil peaked at $140, but Treasury yields stopped following after 4.0%, with the market starting to position for a recession.In this cycle, high oil prices will also catalyze recession expectations— foreign bank research shows that for every 1% rise in oil prices, US household consumption is dragged down by about 0.06%. Coupled with the divergence in US stocks and negative news in Private Credit, recession expectations are not unfounded.

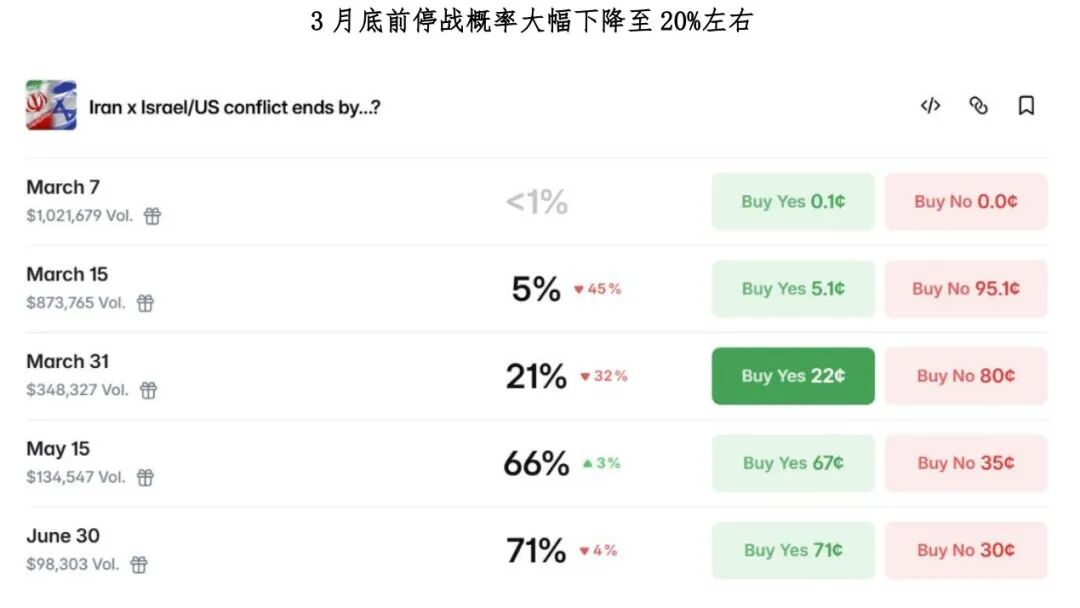

The above discussion focuses on the present, but what about the future?It is noteworthy that the Middle East situation is highly volatile, and market expectations are constantly changing. Based on current Polymarket and other betting site odds, the market now increasingly believes the US-Iran conflict is turning into a protracted war—bets show that the probability of a ceasefire before March 31 has fallen to 20%, and even the probability for a ceasefire by mid-May is only about 60%.

Overall, the US military’s early objectives (a 3-4 week quick victory) are out of reach, and the current situation cannot be solved simply…High oil prices might not form a sharp peak, but rather a sticky, rounded top.

What are the asset allocation opportunities? I believe there are several points to consider:

1. For US Treasuries, a curve flattening strategy should be prioritized.Because short-term rate cut expectations may converge further, or even be priced out, while the long end remains volatile;

2. In foreign exchange, go long the Canadian dollar and US dollar.Both are typical beneficiaries of high oil prices. The dollar’s own fundamentals are actually quite weak, but high oil prices impact the euro and yen even more;

3. In precious metals, seize the opportunity to buy on corrections.True, liquidity tightening is the main risk facing gold investments at this stage, especially apparent during US trading hours. However, there is still plenty of new capital in this market, and the long-term thesis remains strong—pullbacks are good opportunities to build positions.

To summarize today’s discussion:

1. Recently, although US Treasury yields have risen, the pricing is still insufficient compared to the skyrocketing oil prices. Two reasons: first, the market largely sees the US-Iran war and oil price surge as a short-term event; second, US Treasuries are beginning to price in longer-term recession risks;

2. It’s important to note that the Middle East situation is highly uncertain, and market expectations are constantly changing. Polymarket pricing suggests the market is increasingly betting on a protracted US-Iran conflict. The current situation cannot be quickly resolved…

3. What are the implications for assets?I believe high oil prices are unlikely to be a sharp peak, but instead will form a sticky, rounded top.US Treasury curve may flatten, go long on CAD and USD in forex, and take seriously any dip-buying opportunities in precious metals.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Lucrative Stocks That Still Raise Some Questions

Bitway (BTW) 24-Hour Amplitude Reaches 88.0%: Speculative Rally Driven by Over $170 Million Surge in Trading Volume

Rocket Lab Surges 21.9% Over the Last Three Months: Is Now the Time to Invest?