The path to recovery seemed close, but increasing fuel expenses might have set it back once again

Trucking Industry Hopes Dashed by Rising Fuel Costs

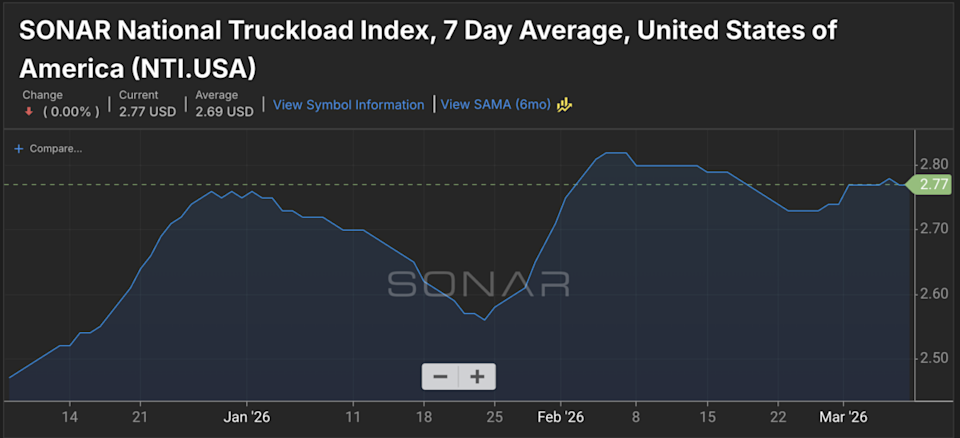

After three challenging years, the trucking sector was beginning to regain confidence. While not celebrating, industry professionals were cautiously optimistic as key indicators improved: spot rates were on the rise, excess capacity had diminished due to carrier closures and stricter regulations, and investment in new fleets remained low. Sentiment surveys reflected this renewed hope, and analysts who had previously delivered bleak forecasts started mentioning terms like “turning point” and “market rebalance.” The freight downturn that began in April 2022 finally seemed to be loosening its hold.

That optimism, however, was short-lived—just two weeks ago, the outlook changed dramatically.

Chart: SONAR (NTI.USA). Spot rates over the past 3 months have looked more like a roller coaster than a gradual climb out.

Currently, crude oil prices have surged to between $100 and $111 per barrel, and diesel has reached a national average of $4.60 per gallon, with $5 on the horizon. The ongoing conflict involving U.S.-Israeli forces and Iran has threatened to close the Strait of Hormuz, a critical passage for about a third of the world’s seaborne crude oil. The Federal Reserve, which had been preparing to lower interest rates to support the economy, now faces renewed inflation concerns driven by soaring oil prices, making rate cuts unlikely. The fragile optimism among small carriers has been thrown into doubt once again.

This is fundamentally a story about cash flow and capital. If you operate a small trucking business, it’s crucial to approach the situation with this perspective.

How the Recovery Was Built

To understand what’s at stake, it’s important to recognize how precarious the recovery actually was. The trucking industry didn’t truly bounce back in 2025—it endured. There’s a significant distinction between survival and recovery.

The real change came from the supply side. Throughout 2023 and 2024, more carriers exited the market, with the FMCSA recording over 6,400 authority revocations in December 2025 alone, after accounting for reinstatements. Low profitability, rising insurance and financing costs, and years of rates below operating expenses forced undercapitalized operators out. Class 8 truck sales dropped to their lowest January levels since 2011. Fleet investments were focused on replacing old equipment rather than expansion. The industry was contracting to match demand, not growing with it.

On the demand side, there was little improvement. Consumer spending shifted toward services after the pandemic and never fully returned to the goods sector that drives trucking. Manufacturing remained weak, and ISM New Orders—a key indicator for trucking growth—never consistently surpassed the 55 mark that typically signals expansion. FTR Transportation Intelligence described the environment as the “most favorable for carriers since February 2022” heading into 2026, but notably avoided calling it a demand surge.

Industry Sentiment and the Need for Demand

A survey of over 600 carriers in February 2026 showed growing optimism, yet 68% had no plans to buy new equipment in the first half of the year. Over a third were unsure about their professional future in six months. The optimism was cautious, shaped by years of hardship.

What the industry truly needed was a boost in demand—a spark to match the tightened capacity and finally create the rate environment necessary for carriers to rebuild margins and cash reserves. FTR even suggested that a market resembling 2021 was possible if demand picked up—a rare note of optimism from a typically cautious firm.

But then, oil prices broke the $100 barrier.

How Sustained High Oil Prices Impact the Economy and Freight

While the relationship between fuel costs and freight demand isn’t always immediate, it is significant and tends to intensify over time—often affecting small carriers before larger shippers feel the impact.

- Consumer Impact: When oil prices spike, consumers feel it first. Higher fuel costs act as a “stealth tax,” reducing discretionary spending and shifting purchases away from goods—the very sector that fuels trucking demand. Economists estimate that every $10 increase in crude adds about 25 cents per gallon at the pump. With crude jumping from $63 to $111 in a month, the effect is substantial.

- Business and Manufacturing: Next, higher oil prices drive up costs for producers—fuel, lubricants, plastics, fertilizers, and more become more expensive. Businesses, already cautious, slow down inventory building and capital spending. Orders and production decrease, leading to less freight.

- Monetary Policy: The Federal Reserve had been preparing to lower rates in 2026, which would have eased financing for equipment and reduced credit costs for small carriers. Now, with inflation concerns rising, that relief is on hold. Analysts warn that the oil surge has brought stagflation—rising prices alongside slowing growth—back into focus. The Fed is pausing rate cuts, and markets expect higher rates to persist through 2026. Carriers hoping for lower rates to refinance or expand credit will have to wait much longer.

Economic analysts estimate that a sustained $90 per barrel oil price would add at least 0.6 percentage points to U.S. inflation. With prices well above that, and consumer demand growing at just 1.5% annually in early 2026, the freight market now faces headwinds instead of the demand boost it needed.

Cash Flow Challenges Facing Small Carriers

It’s important to address the financial realities facing small carriers, as industry coverage often overlooks the day-to-day struggles of operators running just a few trucks or relying on load boards.

Many small carriers entered this period already burdened by years of razor-thin margins. Those who survived 2023–2025 did so by slashing costs, delaying equipment upgrades, operating older vehicles, and accepting rates that left little room for savings.

Fuel is the largest variable expense in trucking. At $4.60 per gallon, a truck averaging 6 miles per gallon spends $0.77 per mile on fuel. At $5.00, that rises to $0.83 per mile. According to ATRI, the total cost of operating a truck was about $2.27 per mile in 2024 and 2025. Increases of just six to eight cents per mile in fuel costs can wipe out already slim profits, and in some cases, turn every mile into a loss.

Cash flow timing makes matters worse. Fuel must be paid for immediately, while freight payments can take 30 to 45 days—or three to five days with factoring, minus fees. When fuel costs spike, the gap between expenses and revenue widens. A carrier running five loads in a week might spend $1,500 to $2,000 more on fuel than planned, depleting cash reserves long before revenue arrives. For those already living week to week, this gap can threaten their very survival.

Steps to Protect Your Capital Now

- Update Your Fuel Surcharge Policy: Make sure your fuel surcharge is clearly documented, communicated, and enforced immediately. Use the EIA national average diesel price as your benchmark. If your cost model was based on $3.50 diesel and you’re now paying $4.60, that’s a 110-cent difference. At the standard formula of one cent per mile for every six-cent increase, you’re looking at about 18 cents per mile in additional costs. For a carrier running 8,000 miles a week, that’s $1,440 lost each week if you don’t adjust your surcharge.

- Assess Your Cash and Credit: Review your available cash and credit lines. Know exactly what resources you have and what they cost. This isn’t about using credit recklessly, but about being prepared. Understanding your liquidity options allows you to make strategic decisions rather than desperate ones.

- Reevaluate Load Selection: Base your load decisions on current fuel prices, not outdated figures. Calculate your break-even rate per mile with diesel at $4.60, and refuse loads that don’t cover your costs. Accepting loads below your break-even isn’t revenue—it’s essentially providing a loan to shippers at your own expense.

- Consider Factoring: If cash flow is a concern and you don’t already use factoring, now is the time to seriously consider it. While factoring fees are real, they’re often less costly than the disruptions caused by cash shortages—such as missed loads, deferred maintenance, or lost opportunities.

Looking Ahead: Recovery Postponed, Not Lost

The recovery that seemed within reach for the trucking industry as recently as February 2026 hasn’t disappeared. The supply-side improvements remain: carriers who left the market aren’t returning, and the Class 8 fleet continues to shrink. The structural factors favoring carriers are still present.

What the oil shock has done is delay the demand catalyst needed to turn these supply-side gains into real rate recovery and improved margins. If oil prices stabilize or fall as tensions in Iran ease—there are early signs of diplomatic progress—the impact on consumer spending and freight demand could be contained. The best-case scenario is a sharp spike followed by partial stabilization, similar to the pattern seen after the Ukraine conflict in 2022.

However, carriers must also prepare for a less favorable outcome: if disruptions in the Strait of Hormuz persist and high oil prices continue through mid-2026, demand could weaken just as the market was ready for growth. In that case, recovery could be pushed back to late 2026 or even 2027. The carriers that make it through will be those who rigorously protect their cash, enforce fuel surcharges, and refuse to accept rates that undermine their business.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin could face deeper downside as odds of U.S. market meltdown rise to 35%

WTI Price Forecast: Multi-year high above $126 looks possible

Japan’s Takaichi: Difficult to say now how Middle East conflict might affect Japan's economy